NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US-China trade talks have been called off for the foreseeable future with little market impact.

Who’ll be the next in line?

Who’ll be the next in line for heartache?

Who’ll make the same mistakes I made over you? – The Kinks

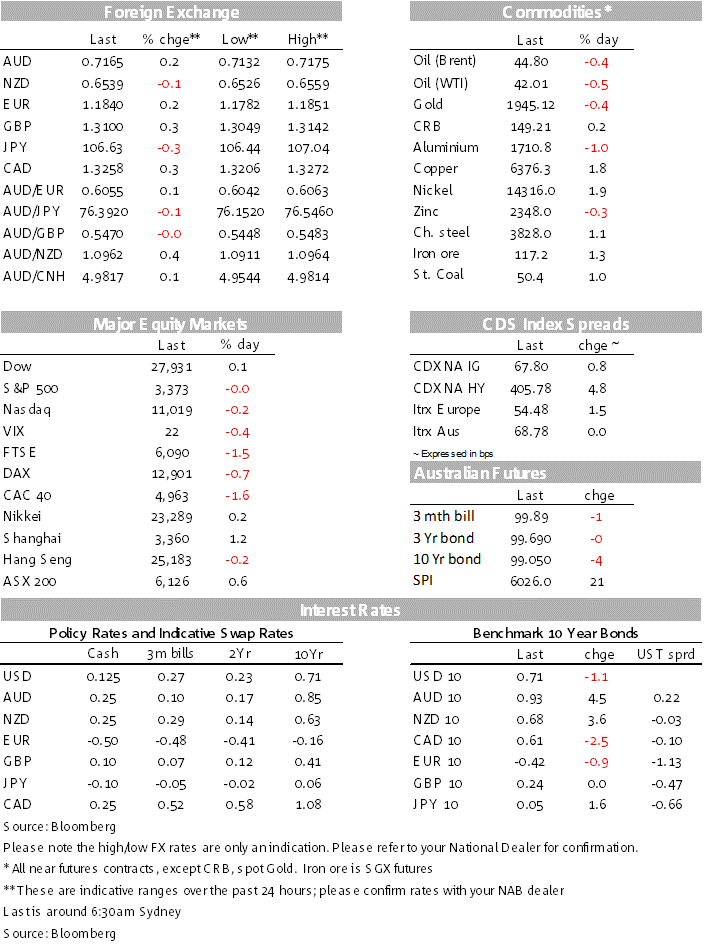

Friday was a tame and mixed day for the US equity market while the increase in COVID-19 infections weighed on Europe. News that US-China Phase-One trade deal has been postponed indefinitely didn’t elicit much of a reaction. 10y UST yields consolidated close to their weekly highs and the USD edged a little bit lower. NZD was the G10 weekly underperformer while the AUD was little changed. Over the weekend President Trump hinted at more action against Chinese companies operating in the US with Alibaba potentially next.

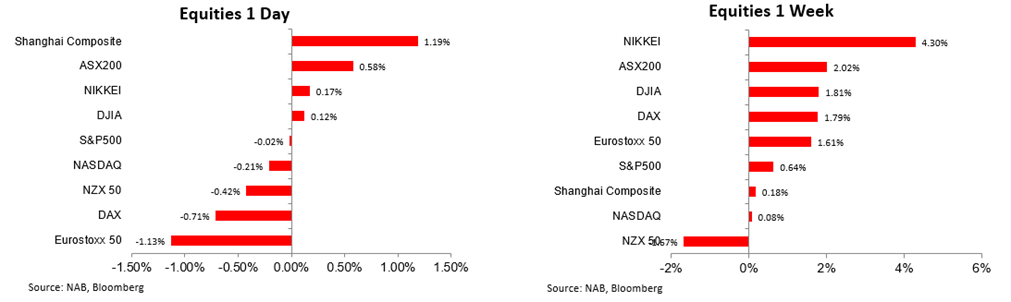

The S&P 500 closed -0.10% lower on Friday while the NASDAQ ended down 0.21%. For the week the S&P 500 gained 0.64%, its third consecutive weekly gain, although it was its smallest weekly gain since the COVID-19 crises began in March.

The NASDAQ was 0.08% higher for the week. News that a scheduled review of the US-China Phase-One trade deal has been postponed indefinitely due to scheduling issue didn’t elicit much of a reaction by markets. For now there is no signs the trade deal is in jeopardy with the review’s postponement seen as an allowance for China to increase its purchase of US agricultural goods, which are way behind schedule.

The US administration has continued to increase tensions with China. Over the weekend, President Trump ordered that Chinese-owned ByteDance sell its video-sharing app Tik Tok within 90 days, effectively putting a deadline for those US firms lining up to buy it. Separately, the Commerce Department said it was ending a temporary waiver for US firms to do business with Huawei, requiring those firms to apply for licences. Trump also hinted that he is looking at taking action against other Chinese tech giants, such as Alibaba, and the risk for the market is he ratchets up tensions further into November’s election.

All major regional indices ended the day down between -0.71% to -1.82% while the Stoxx 600 fell 1.2%, with all sectors in the red. Declines led by travel & leisure sector not helped by concern over a spike in COVID-19 infections around Europe plus news that the UK had introduces self-quarantine for 14 days from Saturday on travellers from France and Holland, as well as certain other countries.

Over the weekend we learned that German virus cases rose to their highest since the end of April on Saturday (1505 but 704 on Sunday) and a big European tour operator, TUI AG cancelled all tours to Spain after the German government advised against non-essential travel to the country because of a resurgence of outbreaks. It seems fair to suggest Europe’s travel and leisure equity sector will remain under pressure at the start of the new week.

Retail sales were +1.2% m/m in July, below the consensus +2.1%, but the core and control reading beat expectations. Core Sales, Ex-auto were +1.9% in July, stronger than the 1% by consensus while the key control series — ex autos, gas, building materials & food services — was +1.4% in July, versus consensus +0.8%. The good news is that core retail sales in the US are now back to pre-COVID levels.

Is that the US Consumer remains very cautious with the Michigan sentiment index printing essentially unchanged at 72.8 in early August, from 72.5 in July. This is a subdued level and just like retail sales the outlook does not look promising given that we know the enhanced unemployment benefits that have been supported the consumer have expired. US politician are still debating the next stimulus and without another a new round of support it seems likely that job uncertainty and limited income prospects will weigh on consumer confidence and spending.

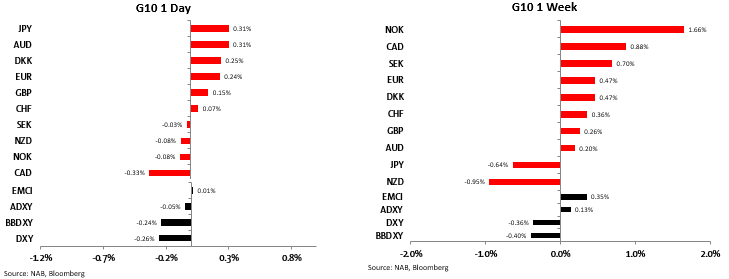

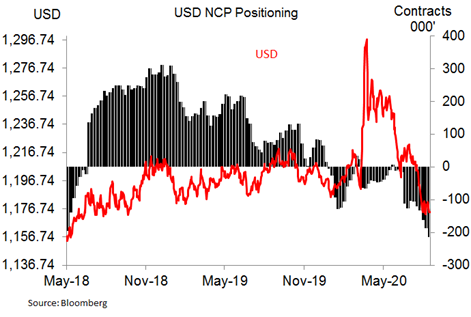

Like equities, Friday’s moves were also very subdued. The USD was weaker in index terms (BBDXY – 0.16%) with its weekly return also negative ( BBDXY -0.40% while DXY was -0.36%). Speculative investors increased their short positions in the USD last week according to the CFTC; the net short USD position in futures held by speculators is now its biggest since mid-2018 ( see chart of the day below).

The euro managed to edge a 0.24% gain on Friday notwithstanding the underperformance in European equity market amid COVID-19 concerns, the euro opens the new week at 1.1841 and it will be interesting to see if it can maintain its buoyancy against the USD ( euro up 0.47% for the week) or if COVID-19 news ebgin to weigh. The AUD/USD also managed to eke out a small gain 0.31% on Friday ending the week at 0.7171. The AUD/USD remains in consolidation mode with a sustained move above 72c still elusive. This seems to be consistent with its high degree of correlation to the US equity with the latter also showing signs of altitude sickness.

The NZD was also the weakest of the G10 currencies last week (-1%), in part due to the dovish RBNZ MPS which reignited market expectations for a negative OCR next year. The AUDNZD cross has also continued to edge higher , the cross now trades at 1.0955, its highest level since October 2018. The contrast between the RBNZ and RBA is stark, with Governor Lowe on Friday reiterating that the negative interest rates are “extraordinarily unlikely” for Australia, although he didn’t rule out a quantity-based QE bond buying programme in the future.

Victoria extended a state of emergency by four more weeks through September 13 and this morning NZ PM Arden will announce whether the election will go ahead as originally scheduled, on September 19th or is delayed.

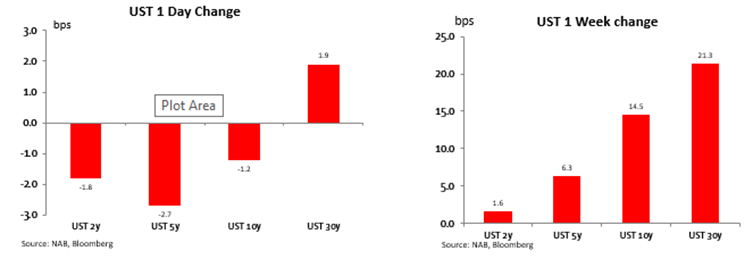

Movement in UST yields were also mixed on Friday. The 10y UST note closed the day 1bps lower at 0.71%, but the 30y Bond climbed another 1.9 to 1.44%. A bear steeping of the curve was the theme for the week with the 30y bond up 21.3 bps

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.