Online retail sales growth slowed in May following a fairly strong April

Insight

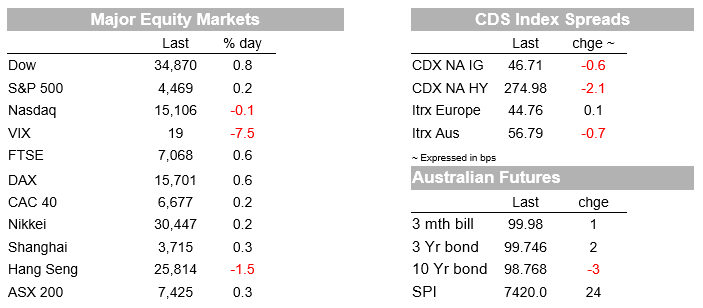

It has been a slow start to the week with little in the way of market moves outside of commodities. Markets overall appear to be in a holding pattern ahead of US CPI figures tonight and the FOMC next week . The S&P500 swung between small gains and losses to finish up 0.2% after five consecutive days of losses, helped along by energy stocks.

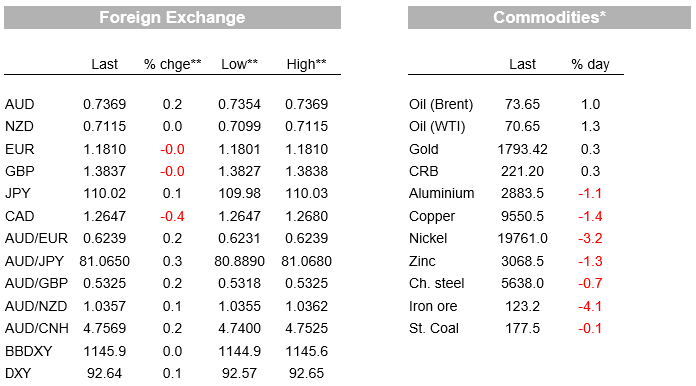

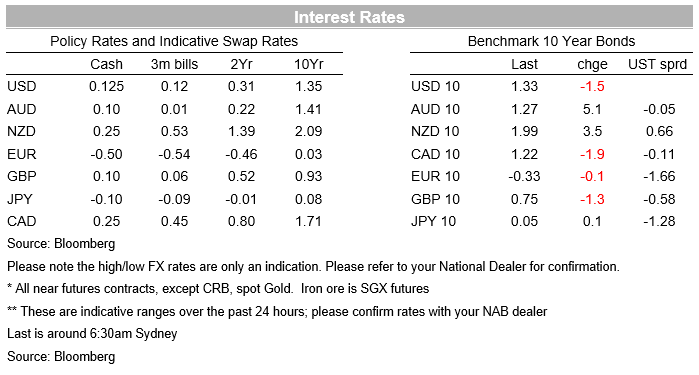

It has been a slow start to the week with little in the way of market moves outside of commodities. Markets overall appear to be in a holding pattern ahead of US CPI figures tonight and the FOMC next week . The S&P500 swung between small gains and losses to finish up 0.2% after five consecutive days of losses, helped along by energy stocks (energy sub-index +2.9%). Today’s gains see the S&P500 now just 1.5% away from its early September peak. Brent oil rose 1.0% to 73.65 on a combination of a better demand outlook and ongoing supply disruptions in the Gulf of Mexico due to recent storm activity. As for rates, it was very quiet with the US 10yr yield ticking down -1.5bps to 1.33%, only partly reversing the 4.8bp rise on Friday. Interestingly the move was driven by the implied inflation breakeven which fell -2.4bps to 2.37%, and thus not following the movement in energy prices. Commodity linked currencies though did take their que from energy with the AUD +0.2% to 0.7369, USD/CAD -0.4% to 1.2647 and USD/NOK -0.3% to 8.6426. The broader USD (BBDXY +0.0%) was little changed with EUR -0.0%, GBP -0.0% and USD/Yen +0.1%.

There was little in the way of data, while news flows continued to play to the view of doubt around the magnitude of further US stimulus. Proposed legislation released on Monday showed that the House Democrats’ tax reform plan to help fund President Biden’s proposed $3.5 trillion budget plan is smaller in scale than the original proposal. Reports show that the plan is to increase the top rate on capital gains to 25%, from 20%. Including the 3.8% Medicare surtax on high income earners this would take the top capital gains rate to 28.8%, still well below Biden’s proposal of a 39.6% rate (43.4% if include surtax) for incomes of $1 million or higher. For the corporate tax rate, the proposal is to increase this from 21% to 26.5% versus Biden’s proposal of 28% (see WSJ: Democrats Release Details of Proposed Tax Increase). Senator Manchin who’s vote is crucial to pass legislation in the Senate continues to object to a $3.5 trillion stimulus, stating on Sunday “It’s going to be $1, $1.5 [trillion]. We don’t know where it’s going to be. It’s not going to be at $3.5 [trillion], I can assure you.” (see Politico: Manchin suggests he may support a $1T-$1.5T spending agenda).

Elsewhere China is battling another delta outbreak that involves at least 75 positive cases. The latest modelling by health officials suggest that the outbreak might peak later in September. Another round of lockdown restrictions due to China’s elimination strategy threatens to further weaken momentum after surprising softness in the recent PMIs. S&P Ratings overnight also warned China needs to start to transition to living with the virus, noting that while restrictions are effective, “ the need to manage recurring episodes of outbreaks and lockdowns under the zero-COVID approach adds additional burdens to corporates in the country, which have yet to fully recover and are seeing weakening credit trends” and that going forward ratings could be pushed “further into the negative” if outbreaks continue to disrupt the country.

In more optimistic virus/vaccine news, latest research continues to show vaccines provide a high degree of protection and that the surge in virus cases due to delta is from the unvaccinated. An analysis of more than 50,000 Covid-19 deaths in England this year shows only 256 deaths occurred amongst fully vaccinated people, equivalent to just 0.5% of all COVID-19 deaths (see UK ONS for details ). Similar statistics are being seen across the pond with the WSJ noting at a Tampa General Hospital, about 90% of recent Covid-19 patients were unvaccinated (see WSJ: Unvaccinated People 11 Times as Likely to Die From Covid-19).

As for commodities, oil prices pushed up nearly 1% taking Brent Crude just shy of $74 overnight. A monthly report from OPEC showed global consumption of oil expected to rise by 4.2m barrels a day for 2022, about a million barrels a day higher than last month’s estimate on the back of the global economic recovery. In addition supply disruptions out of the Gulf of Mexico continue with Tropical Storm Nicholas set to make landfall in Texas, while the mess after Hurricane Ida still sees nearly 50% of oil supply down in the Gulf. Aluminium prices also continued their strong rally, breaking up through $3000 per ton for the first time since 2008 on the back of supply disruptions across many regions.

Finally across the ditch, NZ extended level 4 lockdown in Auckland for another week, though Cabinet had agreed to an “in-principle” move to Level 3 thereafter. Interestingly lockdown restrictions do not appear to be hampering NZ business confidence with the preliminary ANZ business survey for September largely retaining the poise that was evident in the post-lockdown portion of the survey responses for August. While activity expectations have been bruised, and profit expectations undermined, the survey’s inflation gauges remained relatively strong. My BNZ colleagues note these results are in stark contrast to what we saw during previous lockdowns. This suggests the majority of businesses are not only better able to see their way out of the present predicament, but that a capacity constrained economy will accompany them out the other side.

A busy day for Australia with RBA Governor Lowe speaking along with the NAB Business Survey. Offshore the most interesting piece is the US CPI with signs that some of the transitory price components have peaked. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.