Robust growth for online retail sales observed in June

Insight

The rush to bonds continued on Friday, hitting new lows for Treasury yields, even as equities in the US saw a last-minute push and actually finished the week up a little.

https://soundcloud.com/user-291029717/oil-price-battle-will-add-to-volatility?in=user-291029717/sets/the-morning-call

Another wild Friday across financial asset and commodity markets, completed disconnected from incoming hard economic news since the latter continues to predate the dramatic downforce on all manner of service sector activity outside China from the various voluntary or policy-mandated ‘social distancing’ responses to the COVID-19 crisis. The number of confirmed COVID-19 cases is now just under 110k and the number of deaths is approaching 4,000. Over the weekend Italy’s government imposed travel restrictions in Lombardy and surrounding provinces that will affect a quarter of its population. France has just announced a ban on gatherings of more than 1,000 in an effort to contain the coronavirus.

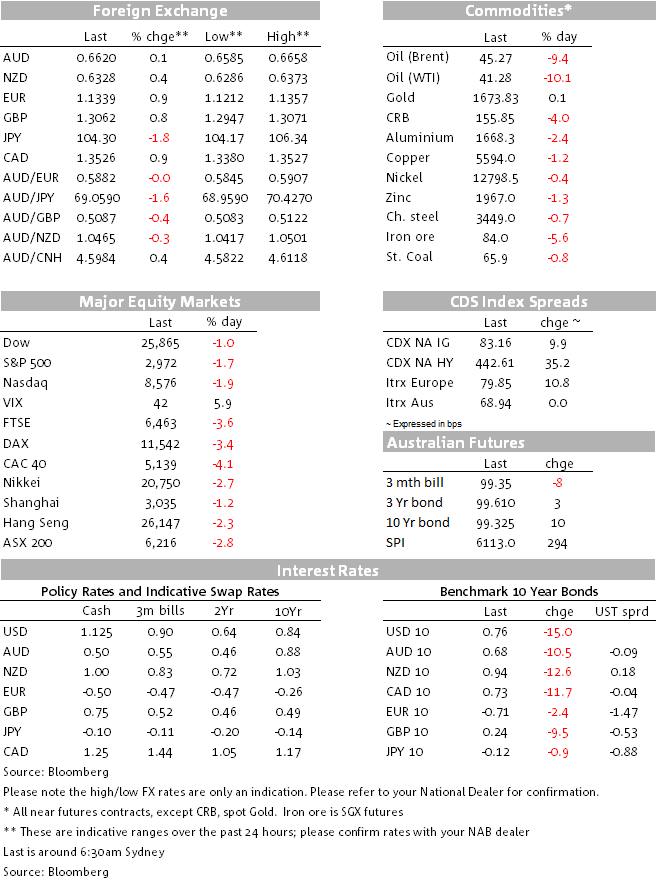

The now all-too regular last ‘hour of power’ in US equity markets saw the S&P 500 lift by more than 2.5% off its intra-day lows, and while the index still ended 1.7% down on the day it is actually up on the week (by 0.6%).The NASDAQ closed1.9% down for a 0.1% weekly gain and the Dow 1% lower for a 1.8% rise on the week. Even the structurally bullish 24-hour business news channels were raising eyebrows about the late day performance, hinting at some sort of invisible hand but without pointing the finger at any particular place (remember the ‘pension funds buying’ shout that went up during the previous Friday’s last hour of trading when the S&P similarly jumped by 2.5%?). Prior to the late-day turnaround, the VIX index hit 54.4, its highest since January 2009, before settling just above 40.

Expectations of plenty more policy support for the economy and financial markets from where last week’s 50-point Fed rate cut came from figured in some stock market narratives, in which respect US money markets now have a full 75bp of additional rate cuts fully priced to occur by no later than the June FOMC meeting. Down here, a follow-up 0.25% Cash Rate cut is 98% priced for the 7 April RBA meeting. Before then, the details and initial magnitude of the Morrison government’s fiscal support plans are keenly awaited (likely later this week). On the US fiscal front, President Trump on Friday signed into law an $8.3bn bill for fighting the coronavirus.

The biggest price movement on Friday was not in stocks, bonds or currencies but rather oil, where WTI crude plunged by 10% and Brent crude by 9.4% after the OPEC+ meeting ended in a dramatic failure, Russia refusing to bow to the will of Saudi Arabia who wants to slash production in an effort to offset the hit to demand from the coronavirus outbreak. The relative resilience of Russia’s public finances to lower oil prices and, strategically, a view that cheap crude prices will knock out competition from US shale oil, reportedly motivate Russia’s new-found refusal to play ball with OPEC. The energy sector was the single biggest contributor to Friday’s US equity weakness, off 5.6% within the S&P 500..

Bloomberg reported Saudi Arabia plans to increase oil output next month, going well above 10 million barrels a day, as the kingdom responds aggressively to the collapse of its OPEC+ alliance with Russia. Bloomberg reports the world’s largest oil exporter started a price war on Saturday by slashing the prices it sells crude into foreign markets by the most in at least 20 years, offering unprecedented discounts in Europe, the Far East and the U.S. to entice refiners to purchase Saudi crude at the expense of other suppliers. It adds that ‘At the same time, Saudi Arabia has privately told some market participants it could raise production much higher if needed, even going to a record of 12 million barrels a day, according to people familiar with the conversations’. This might all just be aimed at getting Russia back to the negotiating table, but in the meantime further oil price falls look likely, with inevitable spill-overs to the high yield credit markets, in the energy sector in particular.

Industrial metals were all lower again Friday bar a small rise for lead, led by a 2% fall in aluminium. The LMEX index of base metals was down 1.25%. Gold added another $1.60 to $1,674 – a new post-January 2013 high.

The nose dive in US Treasury yields proceeded apace, the 2-year ending the day 9bps lower at 0.51% after having been as low as 0.39% while the 10-year finished off 15bps to 0.76% having traded to a new historic low of 0.66% intra-day. Remember it was only last Tuesday that 10s broke below 1% for the first time in history.

It was another down day for the US dollar, the DXY index losing another 0.5% to close below 96 for the first time since 20 March 2019. Gains of 0.7-0.8% were witnessed for the CHF, JPY, GBP and (curiously) NZD. EUR/USD ended 0.4% higher and spent time above 1.13 for the first time since 1 July 2019. It’s already traded back up above 1.1350 in early APAC trade.

It was tempting on to attribute at least part of Friday’s EUR gains to the surprise 5.5% jump in German factory orders, but the more plausible explanation remains the unwinding of EUR-funded long USD and other global cross-asset positions. Friday’s CFTC/IMM positioning data, for the week ended last Tuesday, shows that while speculative short positioning was pared in the week ended last Tuesday, it remained large at 87k contracts. Overall USD net speculative positioning against G10 currencies was a still-large 155k contracts (though is likely to have fallen a fair bit since then). AUD was more of a by-stander on Friday, but added a third of a percent to 0.6636, but has opened the week lower, as have the CAD and NOK, on the aforementioned oil market developments.

Labour market data from both the US and Canada was better than expected in February, US non-farm payrolls rising by 273k against an expected 175k and with the prior two months revised up by 85k. The unemployment rate fell back to match its cycle low of 3.5%, from 3.6% in January while average hourly earnings rose by 0.3% on the month as expected for a 3.0% annual gain – down from 3.1% in January due to unfavourable base effects. In Canada employment rose by 30.3k (11k expected), the unemployment rate rose to 5.6% from 5.5% as expected while hourly wages growth exceeded expectations at 4.3% y/y, down from 4.4% in January but well above the 3.6% expected.

The more significant economic news since Australia went home on Friday was China’s combined January-February trade data published on Saturday. These showed exports in USD terms slumped by 17.6% in yr/yr terms (consensus -16.2%) having been +7.6% in December, while imports held up by more than expected, just -4.0% y/y (-16.1% consensus) having been +16.3% in December. The overall trade balance was in deficit by $7.1bn against expectations for a $38.85bn surplus.

We also had China February FX reserves on Saturday, which at $3.107tn from $3.116tn in January suggests little FX intervention last month, the fall broadly consistent with negative valuation effects from the slightly stronger USD.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.