On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Market sentiment has switched in the last 24 hours, with concerns that the economic recovery from COVID-19 might be slower than anticipated.

https://soundcloud.com/user-291029717/oil-price-spills-over-covid-recovery-concerns?in=user-291029717/sets/the-morning-call

Reaching out for something you’ve got to feel, While clutching to what you had thought was real

Struggle within.. – Metallica

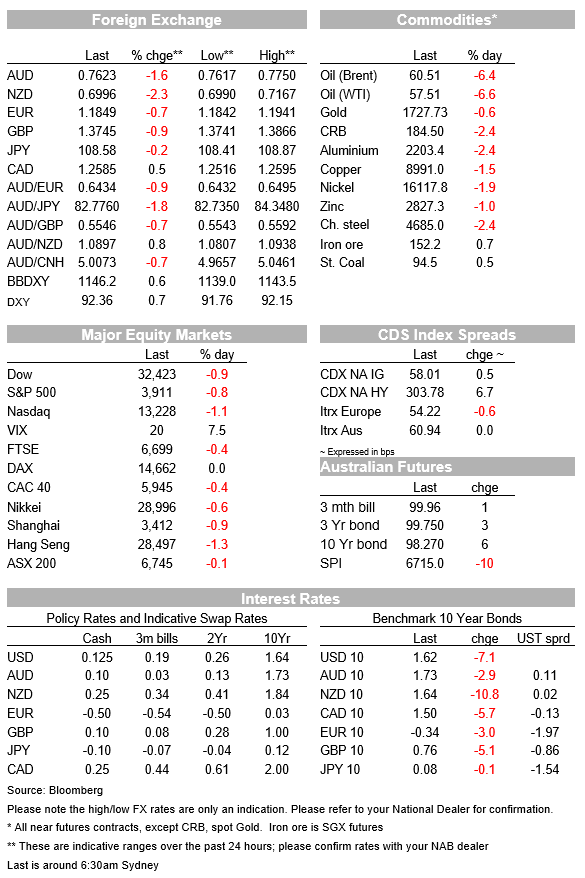

After a negative lead from China, equity markets have remained on retreat mode overnight as investors struggle with the implications of fresh or extended lockdowns in Europe. UST yields extended yesterday’s APAC decline while the USD and JPY are broadly stronger, benefiting from a safety bid. NZD is the big G10 underperformer, down over 2% amid uncertainty from the Government new Housing Policy while risk aversion in the air plus an oil led softer commodity backdrop have not helped the AUD, down 1% to 0.7652.

The decline in China’s equity market during our session yesterday was already pointing to a difficult start to the overnight session . The CSI index ended the day 0.95% lower, extending its loses to over 15% since it peaked at 5930.91 on February 18. Concerns over underwhelming earnings growth plus PBoC tight liquidity are keeping investors wary while many are looking at the test of key support at 5000 as an additional worry, the index closed at 5009.25, after trading to an intraday low of 4966.53.

European equities opened sharply lower with investors reassessing the implication of fresh or extended lockdowns within the Union . Extended lockdowns in Europe are being driven by the threat of a third wave, with a new variant of the coronavirus on the continent. Yesterday we noted that German leaders imposed another four-week lockdown, while in addition to that a five day lockdown over Easter will be particularly harsh. Most regional equity indices ended the day down between 0.18% and 0.61% while the Stoxx Europe 600 Index declined by 0.2%, after falling over 0.8% earlier in the session. A shift in sector preference was clearly evident with pro cyclical sectors dumped (Auto -2.7% and Energy -1.5%) while defensive sectors outperformed ( Utilities +1.5 and Real Estate +1.25%).

US equities are also trading in the red with the Dow -0.94%, S&P500 -0.76% and NASDAQ -1.12%. A look at the S&P 500 sector performance reveals a similar narrative with Utilities at the top of the leader board (+1.24%) while industrials and materials are the laggards, down 2.05% and 2.41% respectively.

UST have led the decline in core global yields overnight extending the decline recorded during our APAC session yesterday. Relative to yesterday’s close the 10y UST Note is down 7.5bps to 1.6224% while the 30y bonds is -6.5bps to 2.335%. Earlier in the session 10y Bunds close -3bps to -0.341% while 10y UK gilts fell 5bps to 0.7630%.

The USD and JPY have benefited from a safe-haven bid with JPY the only pair managing to outperform the greenback, USD/JPY is +0.12% and trading at ¥108.61 while BBDXY (@1146.1) and DXY (@92.35) are up just over 0.6%.

NZD is the big G10 underperformer, extending yesterday’s decline following the Government’s new Housing policy which encompasses a range of supply and demand side measures designed to attack excess house price inflation and tilt the playing field away from investors and to first home buyers. The kiwi now trades at 0.6997, down over 2.3% in the past 24 hours.

The Government’s demand side, include an extension of the effective capital gains tax for investors (to capture investment properties held for less than 10 rather than the 5 years currently legislated) and, more significantly, the removal of interest rate deductibility on investment properties, immediately for future purchases but phased in over the next four years for existing owners. Supply side measures include a $3.8b contestable fund for councils to fund infrastructure around new developments and easing the path for the state housing agency to acquire land.

Jason Wong, my BNZ colleague, notes that the policy mix makes the RBNZ’s job of driving inflation up more difficult. With lots of moving parts it’s hard to get specific with numbers, but the direction of influence from here seems clear – lower house prices, higher rents, less future monetary policy tightening required and less growth in housing debt going forward.

The market reaction was consistent with the view that measures will be negative for the economic outlook and the pricing of rate hikes through next year was reduced – now just one hike priced in for the whole of next year – driving a chunky 8bps fall in the 2-year swap rate to 0.42%. An even larger fall was evident in the 5-year rate – down 11bps to 1.05% – suggesting that the market sees the economy being more sensitive to interest rates and less upside risk for the OCR from a medium-term perspective.

While not to the same degree, the AUD is also on struggle street, down 1.5% to 0.7625, buffeted by broad risk aversion and an oil slide leading the declines in commodities . Oil prices are down by over 6% on concerns about the demand outlook over coming months in light of the likely delayed recovery in Europe due to extended lockdowns.. Brent crude is trading at $60.5 as I type, Aluminium is down 2.5% (as China mulls selling aluminium from State Reserves to cool prices) and Copper is -1.5%.

In overnight news, Fed Chair Powell and Treasury Secretary Yellen began a two-day hearing in front of lawmakers and are still being grilled as we go to press. Powell reiterated the message from last week’s FOMC statement, indicating that the Fed would provide support to the economy for as long as it takes and played down the risk of inflation getting out of hand, seeing an expected lift in inflation as temporary in nature. Yellen repeated a previous comment she has made suggesting that the US could return to full employment in 2022. So far, there has been no comments of a market-moving nature.

There was little to be gleaned from UK labour market data released late yesterday. The ILO unemployment rate for the 3M to January stood at 5% vs a 5.2% consensus and vs December’s 5.1%. UK weekly jobless claims for February however rose 86k and the claims count percentage to 7.5% from 7.2%. Average weekly earnings for 3M y/y in January were +4.8% vs 4.9% f/c and 4.2% ex-bonus, vs 4.4% expected. The furlough scheme continues to support the labour market and unemployment is unlikely to materially rise until this ends in September.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.