Online retail sales growth slowed in May following a fairly strong April

Insight

Oil prices fell sharply on news Saudi oil production will be back in full by the end of the month.

https://soundcloud.com/user-291029717/oil-slides-as-production-returns?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s Market Research support please let your company’s representative know.

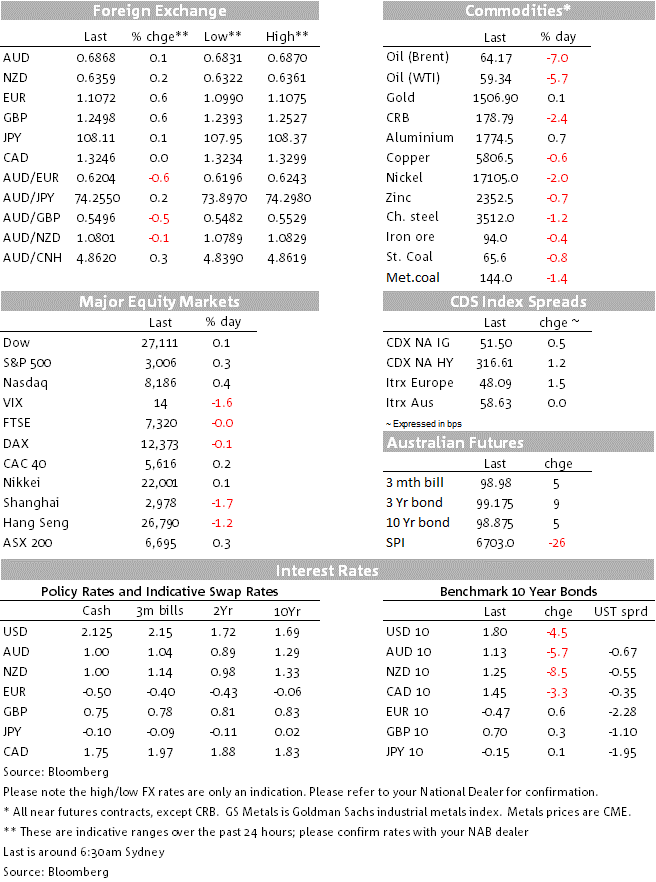

The oil price was the biggest mover this morning with Brent sliding some -7.1% to $64.11 on news that Saudi oil production will be fully back online in 2-3 weeks. In the words of the Bee Gee’s 1977 hit, oil production is Stayin’ Alive. The other significant event overnight has been in the repo market where rates spiked, forcing the Fed to inject some $53.2bn via overnight system repo for the first time in a decade. The move is being seen as more of a plumbing issue and it is likely there will be further Fed intervention in the market – another operation is scheduled for tomorrow (see below for details). In FX it has been a story of USD weakness with DXY -0.4%, partly driving is the lower oil price with oil-importers less likely to come under stress – particularly EM. Gains were seen in EUR (+0.6% to 1.1073) and GBP (+0.6% to 1.2499), while USD weakness reversed the decline in the AUD seen yesterday following the Yuan fix and the dovish RBA Minutes. Equities have largely drifted with the S&P500 +0.3% in a late surge, while US Treasury yields are lower ahead of the FOMC later tonight. Markets are around 86% priced for a cut, with initial focus on the dot plot and then to the press conference to determine whether the Fed is still seeing this as a mid-cycle adjustment or more of a protracted easing cycle.

First to oil. Saudi oil production is set to come back online quicker than expected. Reuters initially reported that normal oil production would be resumed within 2-3 weeks with around 70% of lost production having been restored already. Those sentiments were later confirmed by Saudi Energy Minister Salman who said production will reach 11m barrels per day by the end of September and full capacity of 12m barrels will be restored by the end of October – note that the drone strike initially took some 5.7m barrels out of circulation. Oil has consequently fallen sharply with Brent -7.1% to $64.11 and WTI -6.2% to $59.02. There was little sustained reaction to reports that the US had identified exact locations in Iran from which a combination of drones and missiles were allegedly launched. Given the heightened geopolitical tensions though, we would still expect oil to trade with a higher risk premium then previously even as Saudi production comes back online.

US repo markets were under the spotlight last night with extreme spikes in repo rates (opening at 3.8% but getting as high as 10%) spilling over to the Effective Fed Funds Rate which the Fed uses to implement policy (effective fed funds went from 2.14% on Friday to 2.25% on Monday and likely much higher today – note the Fed publishes transacted rates the next day). To stem the rise the Fed undertook its first overnight system repo in a decade with $53.2bn injected and the Fed has flagged another repo operation for tomorrow capped at $75bn. As for the drivers of higher repo, markets are citing a number of factors including a shortage of FICC sponsored cash (companies pulling cash out in order to pay tax bills), corporate bond issuance and a step up in Treasury issuance, low reserve levels in the banking system, and reports of Saudi cash being pulled out of US markets to support their economy following the drone strike. With the Effective Fed Funds Rate likely outside of the current 2.00-2.25% target range, it is also possible that the FOMC also cuts the IOER rate by more than 25bps today.

Data overnight was mostly second tier. US Industrial Production was stronger than expected in August at +0.6% m/m against 0.2% expected and -0.1% previously. However there were some one-off factors with oil production up +2.6% m/m and the ISM Manufacturing Survey continues to point to dire conditions in the manufacturing sector. Highlighting that overnight was earnings by FedEx whose first quarter results missed expectations as well as lowering guidance for 2020. Fed Ex CEO stated “our performance continues to be negatively impacted by a weakening global macro environment driven by increasing trade tensions and policy uncertainty”. In Germany the ZEW survey of analysts was a little better than expected with the expectations component at -22.5 against -38.0 expected, though it continues to remain firmly negative.

The RBA Minutes yesterday were more dovish than expected and paved the way for a near-term rate cut. A hat tip to my colleagues who were tipping a dovish framing and noting that the Minutes were now being used to convey the RBA’s key messaging as opposed to the post-meeting Statement. While NAB continues to expect the next 25bps cut in November, the Minutes raise the risk of an earlier October move if there is a material deterioration in Thursday’s labour market data – consensus there looks for an unchanged unemployment rate at 5.2%. Markets are pretty much 50/50 on Oct v Nov with October 40% priced and November 95% priced. As for the dovish leanings in the Minutes, the key policy paragraph dropped the reference to waiting for an “accumulation” of evidence in deciding to cut again, the RBA seemed more focused on downside risks to the global outlook and no longer cites a “reasonable” global outlook, while domestically the RBA’s liaison with retailers suggests tax refunds have not boosted spending.

The AUD fell as much as -0.6% in the wake of a weaker CNH (USD/CNH +0.3%) and the dovish RBA Minutes, but a lower oil price and USD weakness saw the losses fully reverse with the AUD unchanged at 0.6866 this morning. The USD was weaker across the board with DXY -0.4% 98.22, with the fall in the oil price alleviating some of the pressure on oil imports – particularly for emerging markets. EUR and GBP were both 0.6% higher, while USD/Yen was little moved at 108.13.

US yields were lower with 10yr Treasury yields -4.2bps to 1.80%. Yields though were higher in Europe, with Italian 10y BTP yields +7.9bps to 0.917% on news at former PM Matteo Renzi has split from the centre-left Democratic party (who has only just formed a coalition to govern) to create a new political party. The bigger driver for yields globally will be the FOMC meeting later tonight where focus will be on the framing of a likely rate cuts. Given divisions in the FOMC it is possible Powell is not as dovish as the markets would like (see coming up for details).

Domestic focus will be on the NAB Business Survey and then to the Chinese CPI/PPI. It is relatively quiet otherwise with little data of note out of the US.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.