Total spending grew 0.9% in June.

Oil shot up in price overnight.

https://soundcloud.com/user-291029717/oil-talk-and-jobless-surge?in=user-291029717/sets/the-morning-call

“Turning my direction; Quench my thirst with gasoline; So gimme fuel, gimme fire, gimme that which I desire”, Metallica 1996

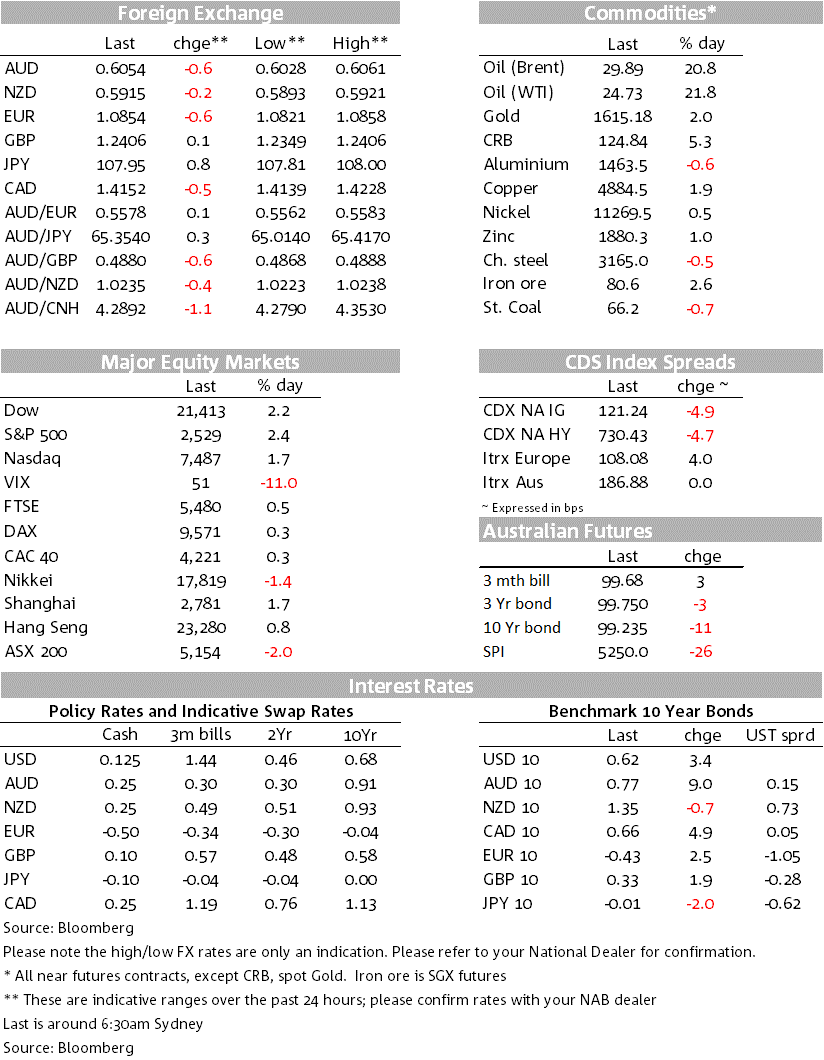

Its all about the oil market today with production cuts looking more likely, while China yesterday also said it was looking to increase its own strategic oil reserves. Brent rocketed, up 20.8% to $29.89 and at one point was up a staggering 47%. The boost in oil prices buoyed energy stocks, pushing equities into the green with the S&P500 +2.4% with the energy sub-index +9.1%. G10 FX saw CAD and NOK outperform (USD/CAD -0.5%; USD/NOK -0.6%), but it was again a story of USD strength with the DXY +0.8%. Broad-based USD gains accelerated after record US jobless claims (emphasising the dollar simile). Initial jobless claims rose 6.6m, and over the past 2wks are up 10m, equivalent to 6% of the entire workforce. The oil price though did flow through to implied inflation breakevens, with US 10yr breakevens +11.9bps to 1.03% (nominal 10yr yields were +3.4bps to 0.62% with real yields falling further into the negative territory). As we open domestically the AUD is down -0.6% to 0.6047, though in the last few minutes has rallied to 0.6069.

Overnight Trump tweeted: “Just spoke to my friend MBS (Crown Prince) of Saudi Arabia, who spoke with President Putin of Russia, & I expect & hope that they will be cutting back approximately 10 Million Barrels, and maybe substantially more which, if it happens, will be GREAT for the oil & gas industry!…..Could be as high as 15 Million Barrels. Good (GREAT) news for everyone!”. Saudi Arabia has called for an emergency OPEC deal and has also invited other nations. The Texas regulator for shale said he had discussed with Russia a global 10m barrel a day cut, and is set to discuss further with Saudi Arabia. Russia though appears a little more cautious, and Saudi Arabia has said they will cut only if other countries join in. Nevertheless, it appears there is sufficient momentum that a global oil production cut is looking more likely than before. Brent and WTI soared, initially by up to 47% and have ended up around 20% (WTI +21.8% and Brent +20.9%).

China also indicated it was looking to build its strategic oil reserves. It is thought China wants to build 90-days of reserves, which would be equivalent to around 900m barrels according to Bloomberg. The current size of China’s reserves in unknown, but some analysts suggest the could see China buying an additional 80-100m barrels over the course of the year.

The rise in US Jobless Claims was the other significant event overnight. Initial claims rose 6.6m, up from 3.3m last week. Over the past two weeks, claims have risen 10m which is equivalent to 6% of the entire US workforce seeking unemployment insurance and is suggestive of a sharp rise in unemployment into the high teens. Jobless claims are likely to remain high over the next few weeks given a widening in states implementing shutdowns, while anecdotally the surge in claims have meant many have been unable to apply for unemployment insurance due to overwhelmed websites and phone lines. We are though unlikely to see a large impact on Payrolls tonight given the payroll pay period is the period including March 12, which pre-dates the rise in jobless claims. The survey period for the unemployment rate also pre-dates the rise, with the household survey referencing the week of March 8-14 (see coming up for details below).

Fed officials continue to warn that unemployment is set to spike – Kaplan the latest saying unemployment could rise to 15% and be back to 8% by year end (see CNBC interview for details). Kaplan also suggested the recovery is more likely to be a U shape (rather than a V) with a likely severe contraction the Q2 spilling into Q3 before a recovery begins. The major determinant of the timing of any recovery will be when containment measures can be lifted, and that depends on the path of the virus. White House advisor Dr Fauci today implied social distancing could be relaxed once there are no new cases (“If we get to the part of the curve where it goes down to essentially no new cases, no deaths for a period of time, I think it makes sense that you have to relax social distancing”). The risk of a second wave of infections though likely means the lifting will be done in a very measured way. In recent days in some places in China, there has been a re-implementation of social distancing out of fears of a second wave of infections and one county with a population of 600k has also re-imposed a full lockdown (see SCMP for details). Dr Fauci also warned COVID-19 might become part of the usual flora of viruses.

G10 FX saw a continuation of USD strength with the DXY +0.8% with broad-based gains except for the oil-linked currencies of NOK and CAD. The EUR fell -0.6% to 1.0854, USD/YEN rose 0.8% and suggestive of some easing in risk aversion to 107.95, while GBP outperformed +0.1% to 1.2406.

The AUD largely reflected moves in the USD with the AUD -0.6% to 0.6054. Australian data yesterday had minimal impact on the Aussie – the NAB Q1 business survey fell to -11 for conditions, while job vacancies declined in Feb though pre-dated the latest COVID-19 developments.

Moody’s reaffirmed the NZ Government’s credit rating at Aaa, while the RBNZ introduced a new lending facility yesterday, called the Term Lending Facility (TLF). As my BNZ colleagues note, details of the scheme are still light, but the RBNZ said it would provide funding to banks for up to three years at low interest rates to support the Government’s recently announced Business Finance Guarantee Scheme. Also in NZ, the RBNZ said it had agreed with NZ banks that there would be no dividend payments “during this period of economic uncertainty” and that there should not be redemption of other (non-CET1) capital instruments. Share prices for the Big 4 Australian banks were down 4-6% yesterday, underperforming the 2% fall in the benchmark index. The RBNZ’s announcement follows a similar move in the UK, where banks agreed to suspend dividend payments at the request of the Bank of England. Australia’s APRA in contrast confirmed yesterday that dividend payments for Australian banks would remain a matter for the respective banks’ boards.

There have been further signs of life in the credit market. US telco T mobile launched a huge $19bn multi-tranche bond offering, attracting more than $43bn in orders. The deal will be the second biggest this year. In Europe, issuance of investment-grade bonds totalled more than €25bn.

Data is likely to continue to take a backseat to COVID-19 news and developments in the oil market. US Payrolls would normally take top billing, but are likely to be interpreted as dated given the reference week is early in the month and largely predates the sudden surge in Jobless Claims. The US Non-manufacturing ISM is likely to decline sharply, but has been foreshadowed by the flash Markit Services PMI. In Australia, data is mostly second-tier with Retail Sales for February being seen as both dated, and already well flagged given the ABS published preliminary numbers not that long ago.

Key prints today:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.