Total spending grew 0.9% in June.

Friday was certainly a gamechanger. The US President went into hospital without a clear picture of his condition. Now, it seems he could be returning to the White House as soon as today. So, do the markets take back some of their risk concerns, and focus on the positives of the situation?

https://soundcloud.com/user-291029717/one-big-october-surprise?in=user-291029717/sets/the-morning-call

Donald Trump – from the late Max Miller (recorded in 2011, at the height of Trump’s ‘Apprentice’ Fame – lyrics unprintable – and originally acclaimed by Trump himself after 20 million YouTube hits)

The much vaunted ‘October Surprise’ was certainly that on Friday with news of President Trump’s positive COVID-19 diagnosis followed by news, post Friday’s market close, of his impending hospitalization.

Latest news is that the President could be released from hospital as early as Monday. The considered take in Friday’s offshore session was linked to both a lift in optimism that a pre-election fiscal aid bill would now get done and that the chances of a Biden election victory – already improved following last Tuesday’s TV-debate – had just risen further.

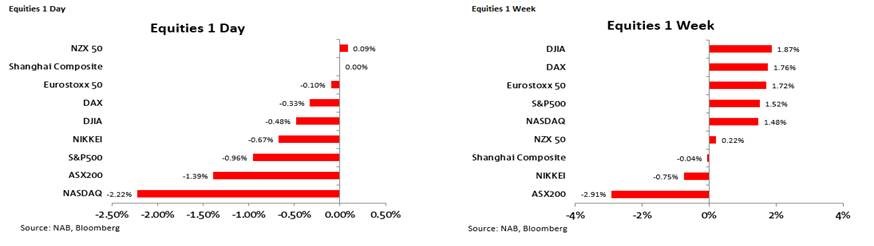

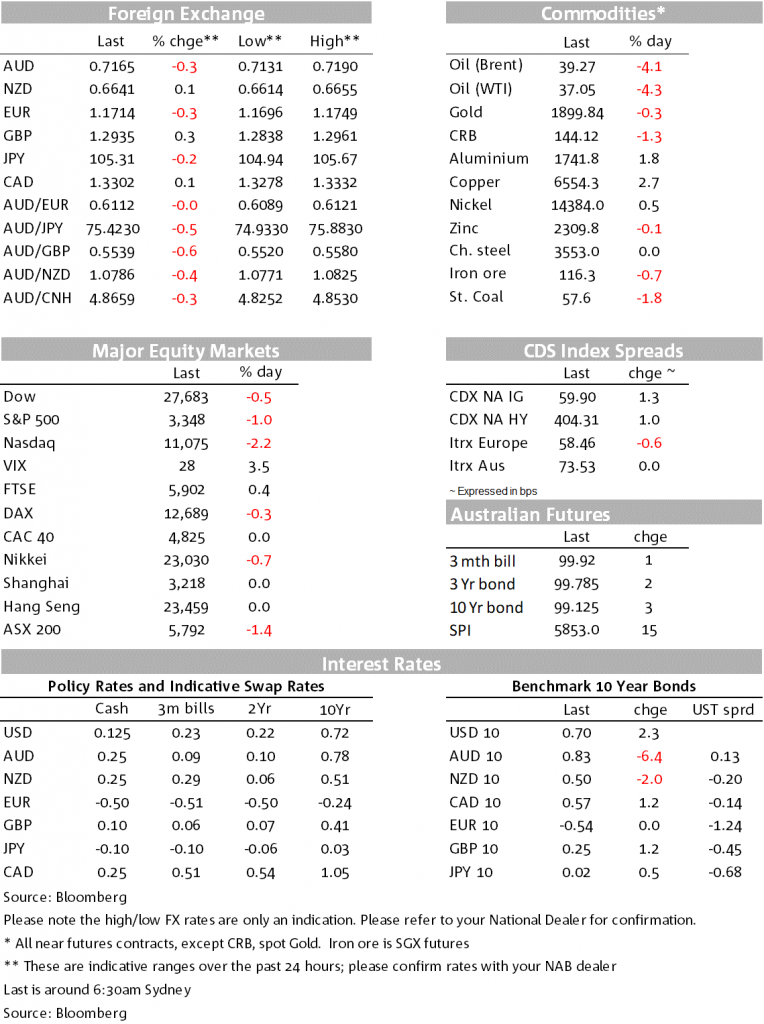

US equity markets ended on Friday for the most part well back from the lows that were seen in futures markets during our afternoon soon after the news of President Trump’s positive COVID-19 test, the S&P finishing in New York just shy of 1% lower having earlier been own closer to 2%. However, there was a real contrast between the NASDAQ, which closed down more than 2% and still near the lows of the day and the likes of the smaller cap Russell 2000, which having also been down by more than 2% at the open, ended the day 0.5% higher:

It is hard to escape the conclusion here that the underperformance of the NASDAQ – and to a lesser extent the S&P relative to smaller cap stocks – reflects markets more confidently pricing in a Biden win on 3 November (or however long thereafter it takes to produce a result) and what that means in terms of key Biden policy proposals with respect to corporate taxes and regulation. In this respect we have also seen the (betting market) odds of a clean sweep or ‘blue wave’ following the election – necessary if passage of much of Biden’s policy agenda is to stand a chance of being passed by Congress – improve from below 60% prior to the TV debate to 64% as of Friday (according to PredictIt).

A just-published NBC/Wall Street Journal poll has Biden’s lead over Trump extending to 14 percentage points from 6 in its previous poll, with Biden now polling ahead of Trump in every state considered ‘swing’ or ‘battleground’.

On improved prospects for a new fiscal support plan being agreed shortly, we have heard optimistic soundings from House speaker Nancy Pelosi, arguing Trumps diagnosis changes the dynamics of the negotiations, but more significantly from Senate leader Mitch McConnell and the President himself, where POTUS tweeted on Saturday ‘OUR GREAT USA WANTS AND NEEDS A STIMULUS. WORK TOGETHER AND GET IT DONE! Thank You!’

The last before the election and on any other day of keen interest for market, was almost completely overshadowed by the Trump news, save that weaker than expected headline employment rise of 661k against an expected 859k confirmed a significant slowdown in the pace of labour market improvement and so further highlighted the imperative of news fiscal support mechanisms falling into place sooner rather than later.

There were 145k worth of upward revisions to July and August data, and private payrolls were up 877k (government jobs down ~200k) plus the unemployment rate dropped by 0.5% to 7.9% (consensus was for a fall from 8.4% to 8.2%). However, the latter was flattered by a 0.3% drop in the labour participation rate, while long term unemployment (i.e. those looking but without work for 6-months or more) rose by 345k to now 3.8 million.

To date, just over half (11.4 million) nd the 22.2 million jobs lost since the pandemic first hit the US, have been recovered.

The final University of Michigan consumer sentiment index lifted to 80.0 from the preliminary 78.9 and 79.0 expected, while in Eurozone September CPI showed headline deflation deepening, to -0.3% from -0.2% and -0.2% expected, with the core measure showing inflation dipping to 0.2% from 0.4% and below the 0.4% expected. These numbers surely add to the ECB shortly announcing a new QE programme to replace the one expiring at the end of the year.

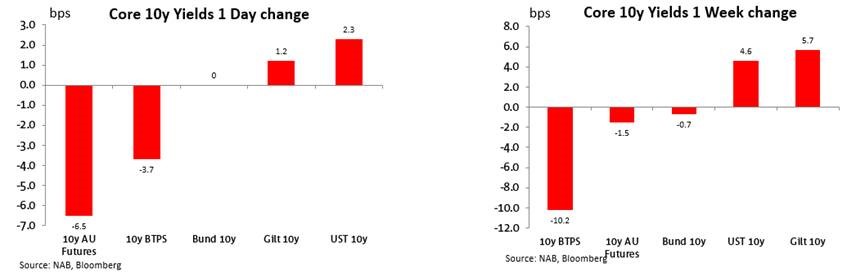

It was the perceived improved chances of a new fiscal support plan that carried the day, 10 year Treasury yields rising from a low of 65bp when the equity sell-off was at its most extreme, to nose back above 70bp by the NY close for a rise of 2bp on the day:

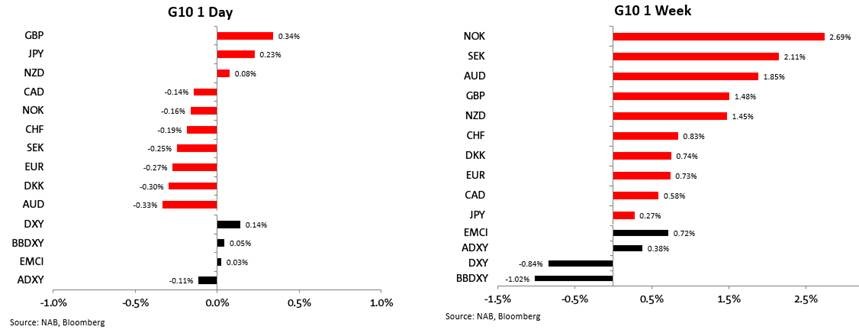

The USD was overall a touch stronger consist with it being a mostly ‘risk-of’ day, the rise in USD indices was blunted somewhat by GBP/USD rising by a third of a cent on ongoing optimism regarding progress toward a UK-EU post Brexit trade deal. Development on Friday and Saturday shows that while insufficient progress has yet been made on the key stocking points such as fishing rights and state aid (as well as the contentious amendments to the Withdrawal Bill) such that negotiators can now enter the ‘tunnel’ or cone of silence to thrash out final details, UK PM Boris Johnson and EU’s Commission chief Ursula von der Leyen agreed Saturday to ‘intensified’ trade talks

The high beta AUD/JPY lost just over 0.5%, consistent with it being a generally risk-off Friday, AUD/USD itself finishing the day down 0.3% but still up 1.9% on the week, one of the best performing major currencies and following the 3.5% decline witnessed in the first four weeks of September:

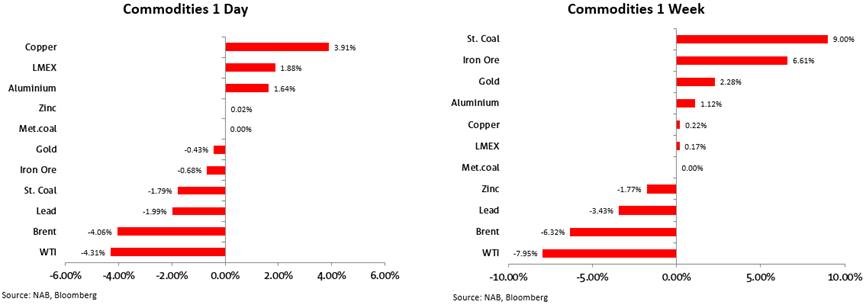

Copper recouping a fair chunk of its mid-week losses and industrial metals (ex-iron ore) mostly firmer, but oil off another 4% with the weekly fall in WTI crude extending to 8%:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.