Online retail sales growth slowed in May following a fairly strong April

Insight

The Bank of England and UK government launched a coordinated approach on tackling COVID-19 headwinds, with an emergency rate cut and fresh fiscal stimulus.

https://soundcloud.com/user-291029717/a-pandemic-and-an-emergency-cut-with-more-help-needed?in=user-291029717/sets/the-morning-call

“You’d better push the button and let me know; Before I get the wrong idea and go”, Sugababes 2005

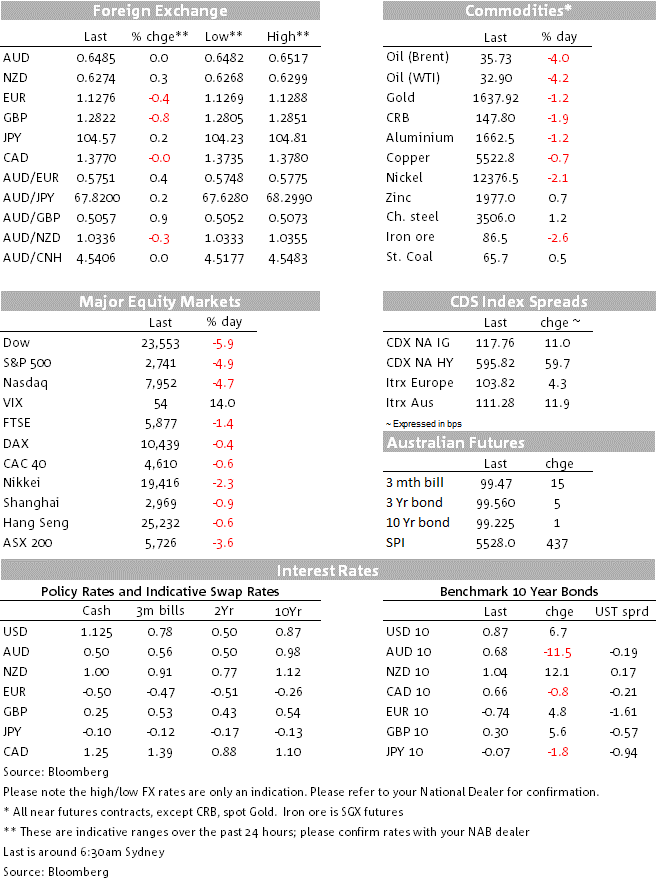

Markets were rattled overnight with the S&P500 -4.9% (reversing Tuesday’s 4.9% gain). As we noted yesterday, markets are crying out for a co-ordinated response to COVID-19 headwinds and a lack of concrete US policy action is rattling markets. The virus itself continues to spread in Europe and the US, meaning more extensive containment measures are likely which will weigh further on global growth. A recent US ISM Institute survey finds more than 80% of firms expect COVID-19 to impact their business, and 16% have adjusted revenue targets down by an average of 5.6% (see link).

Bond markets were a little more steady with US10yr yields +5.7bps to 0.86%. There doesn’t appear to be any specific driver, apart from perhaps notions of expanded fiscal deficits to combat growth headwinds. Currency markets have also been more contained with the USD (DXY) broadly flat with weakness in EUR (-0.3% to 1.1280), largely offset by USD/Yen (+0.3% to 104.67). The biggest G10 mover was GBP which whipsawed on stimulus headlines to finish -0.9% at 1.2812.

The BoE cut rates by 50bps, launched a new 4yr term funding scheme for banks and reduced the countercyclical capital buffer, while the UK Chancellor unveiled a budget which delivers £30bn in fiscal stimulus and a pledge to spend £600bn on infrastructure. The ECB also sets policy tonight and according to sources President Lagarde told EU leaders that a co-ordinated policy response was needed and that the ECB was looking at all their tools, particularly measures to provide super-cheap funding and ensure liquidity and credit don’t dry up. Consensus looks for the ECB to cut its deposit rate by at least 10bps, with an increase in the monthly rate of QE and targeted LTRO being also seen as likely.

The AUD was broadly steady, +01.% to 0.6487. The AUD will largely be at the mercy of headlines with little in the way of data today. The government is scheduled to unveil a fiscal stimulus package, though this has been well flagged in the press. According to the AFR a $17bn package is set to be unveiled (see AFR for details). The measures will include $a 6.7bn to boost cash flows for SME (under the scheme eligible tax-free payments of up to $25,000 will be available to businesses), $1.3bn for wage subsidies for apprentices (package will offer up to $7,000 each quarter in wage assistance for each apprentice), a $700m expansion to the investment asset write-off scheme (by increasing the turnover threshold for eligible business to $500m from $50m, as well as a one-off cash payment worth several hundred each for pensioners and Newstart recipients.

The World Health Organisation (WHO) has declared a pandemic, while the virus itself continues to spread rapidly in Europe (Italian cases surged by over 2,000 yesterday to nearly 12,500) and the US. Governments are becoming more consigned to the notion of the virus being likely to infect a large proportion of the population. German Chancellor Merkel has noted productions that COVID-19 could infect 60-70% of the population, while in the US the Congress’ in house doctor briefed Capital Hill that he expects 70-150m people in the US to be infected (see AXIOS for details). Note while those predictions seem dire, Dr Monahan the in-house doctor noted around 80% of people who get the virus will only have minor symptoms. The concern is for those who are older and have underlying health conditions, making slowing the spread of the virus a priority in order to not overwhelm health systems. The underlying message thus seems to be to expect more containment measures to be implemented, which will continue to weigh on global growth.

US Core-CPI for February came in line with expectations at 0.2% m/m, though the y/y rate was one-tenth higher than expected at 2.4% y/y against 2.3%. While the core-rate at 2.4% is the highest since the GFC, inflation is likely to moderate given COVID-19 headwinds.

All eyes on the government’s fiscal stimulus response, which is likely to be around $17bn according to the press. Internationally the ECB meets where markets expect them to cut the deposit rate by at least 10bps and source stories suggest a targeted loan scheme is also likely to be unveiled.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.