Online retail sales growth slowed in May following a fairly strong April

Insight

There’s a risk-off mood today.

https://soundcloud.com/user-291029717/phase-2-deal-unlikely-trumps-impeachment-proceedings-the-fed-and-the-aussie-dollar?in=user-291029717/sets/the-morning-call

Well we’re scared but we ain’t shakin’, kInda bent, but we ain’t breakin’, in the long run – The Eagles

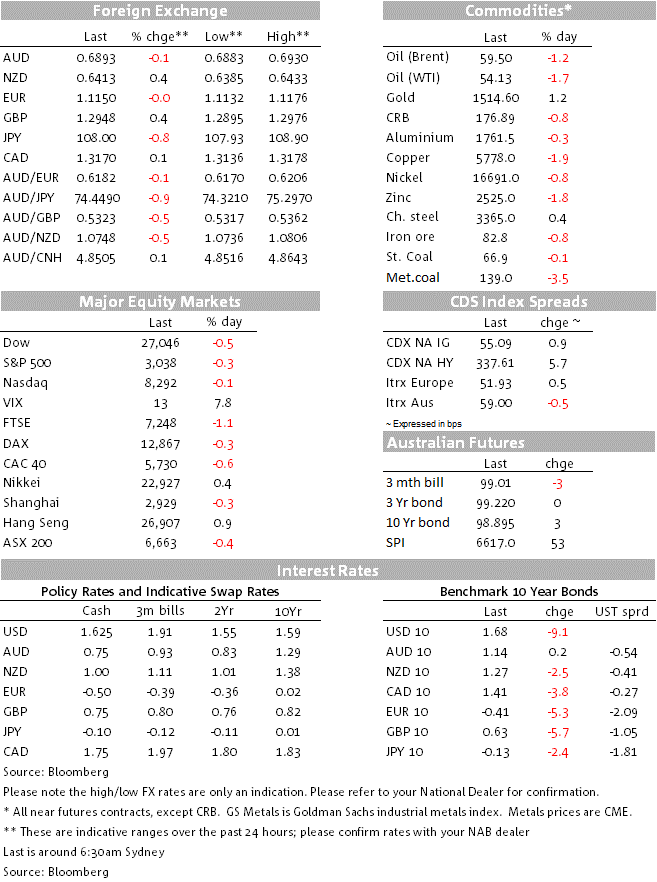

With US stocks reversing Wednesday’s pre and post FOMC gains, US (and global) bond yields smartly lower and the ‘safe haven’ Japanese Yen sitting proud at the top of the G10 FX leader board. The AUD has quickly lost the grip it established above 0.69 yesterday morning, to currently sit at 0.6893.

Top of the list of drivers for overnight market moves has been a report from Bloomberg out of Beijing, where a four day policy plenum is currently taking place. This cites Chinese officials ‘familiar with the matter’ casting doubts about reaching a comprehensive long-term trade deal with the U.S. even as the two sides get close to signing a ‘Phase One’ agreement. The report says China won’t budge on the thorniest issues, and that officials have relayed low expectations that future negotiations could result in anything meaningful — unless the U.S. is willing to roll back more of the existing tariffs.

To our mind, expectations of anything beyond a Phase One agreement which merely agrees not to proceed with further tariff increases while not winding back any existing ones, in return for stepped up China agricultural purchases (along with some modest structural changes – largely already signed off – regarding foreign ownership rules and forced IP transfer, should be running low this side of the 2020 US Presidential elections. Yet some market participants evidently held the view that passage of Phase One could quickly lead to progress on Phase Two next year. We’ll spell out our baseline assumptions on China-US trade and what this means for our currency views in particular, in our forthcoming Global FX Strategist publication on Monday. If you’re a NAB client and not receiving this but would like to, please reply to this email.

Another influence on overnight markets has been a much weaker than expected Chicago PMI, which slumped to 43.2 from 47.1. The Chicago district is the home of Boeing of course and the fall may have reflected a drop in orders there, but we don’t know for sure and the weak print does introduce some potential downside risk to tonight’s all-important Manufacturing ISM, currently forecast at 49.0 up from 47.8 according to the Bloomberg consensus.

News that the US House of Representative has voted largely on party lines to legitimise the Trump impeachment enquiry, which will now switch from behind closed door to the public gaze, was widely expected and doesn’t look to have had direct market impact. Whether or not Trump’s poll ratings shift as the enquiry proceeds will be relevant to markets in coming weeks however, even though no-one sees any chance of the President being convicted by the Senate if the House does ultimately vote to impeach.

Other data to note included the first estimate of Eurozone GDP, coming in 1/10% better than expected at 0.2% (year-on-year +1.1% as expected) but we still don’t know if Germany fell into technical recession in Q3 – its numbers won’t be released until mid-November. Eurozone CPI printed at 0.7% year-on-year as expected down from a (downward revised) 0.8% in September, but the core reading ticked up to 1.1% from 1.0%, 1/10% higher than expected. The US Q3 Employment cost index rose by 0.7% on the quarter in line with consensus while the monthly September PCE data showed the core PCE deflator flat on the month against +0.1% expected but down to 1.7% yr/yr as expected and in line with the quarterly estimate published with yesterday’s GDP data.

Building approvals unexpectedly bounced, by +7.6% with house approvals +3% and units +17%. The data is highly volatile and approvals are still running 39% blow their November 2017 peak, the implication being that housing construction is going to be a significant drag on overall economic activity for a good while to come, notwithstanding the recent pick up in house prices in Victoria and NSW. Privates sector credit growth meanwhile remains very subdued, rising by just 0.2% in September and up just 2.7% on a year ago, down from 2.9% in August.

Yesterday’s shift to ‘state based’ from ‘date based’ forward guidance by the Bank of Japan in conjunction with downgraded forecast for GDP and inflation over the entire three year forecast horizon – which Governor Kuroda described as a form of additional easing – has patently failed to do anything to weaken the JPY. USD/JPY is down 0.8% on Wednesday’s NY closing level at just below ¥108 and AUD/JPY down almost one percent to ¥74.44. More confirmation that the JPY, and AUD/JPY in particular, remains the ‘weapon of choice’ whenever risk sentiment sours.

After the JPY, GBP (+0.4%) and NZD (+0.3%) are the next best performing currencies, NZD seemingly drawing some support yesterday from a change of RBNZ call from Westpac, to no longer expecting a cut in November. The market’s conviction in a November OCR cut had already been slipping in recent weeks, in-line with the decline in RBA and Fed rate cut expectations and the big upside surprise to non-tradables inflation in the latest CPI report. The probability of a November OCR cut has now fallen to 54%. On balance, our BNZ colleagues still think the RBNZ will cut the OCR by 25bps in November in light of weak activity indicators in NZ that point to growth well below the RBNZ’s forecasts.

AUD is siting close to the bottom of the G10 FX league table, currently back just below 0.69. The fall back from the 0.6930 intra-day/night high is almost entirely due to the impact on risk sentiment from the aforementioned China trade story and which also saw USD/CNH pop higher, from 7.03 to above 7.05. Yesterday afternoon, RBA external Board member Ian Harper spoke at a conference in which his main message was that a stronger AUD was highly undesirable and that the upward pressure on the currency from easier Fed policy was a factor in the RBA’s decisions to cut rates here. In this light, we’d note that in trade-weighted terms the AUD is some 2.5% stronger than where it was back in August, and AUD/USD some 3.5% above its early October lows. Reason enough in our view not to rush into thinking that the RBA is now likely on hold until next year at least.

US Equities have just closed with the S&P 500 down 0.3%, the NASDAQ 0.1% lower and the Dow -0.5%. Financials have been the worst performing S&P sector, -1.1% with offsets from consumer staples (+0.6%) Utilities (+0.8%) and IT (+1.1%, including a 2.2% rise for Apple).

US 10-year Treasuries are down 9bp to 1.682%, and 2s -8bps at 1.516%. earlier, European bonds closed 4-7bps lower at 10 years.

Caixin China PMI due at 11:45 AEDT, where the Bloomberg survey median, recorded prior to yesterday’s official PMI numbers – is 51.0 from 51.4

The heavy hitters tonight are first US October payrolls and shortly after the Manufacturing ISM, the latter seen at 49.0 from 47.8 On payrolls, the GM strike is expected to have depressed headline employment by some 40k, so the 85k median estimate needs sot be seen in this context, but would still imply a softening in trend payrolls growth. The unemployment rate is accordingly seen ticking up 3.7% from 3.6% Average hourly earnings growth is seen at 3% up from 2.9% We also get US construction spending.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.