Online retail sales growth slowed in May following a fairly strong April

Insight

The pound weakened as Boris Johnson calls for an election on December 12th.

https://soundcloud.com/user-291029717/arriverderci-mario-pound-hit-by-boris-election-hope?in=user-291029717/sets/the-morning-call

I will stop, I will stop at nothing, Say the right things, When electioneering I trust I can rely on your vote – Radiohead “OK Computer”

PM Johnson now offers more time to debate Withdrawal Agreement Bill (WAB) conditional on MPs agreeing to an election on December 12th, but as always there is a catch, Bojo needs a 2/3 majority to push through. As expected ECB left its policy setting unchanged, but at his last meeting President Draghi departs with a gloomy assessment on the EU economic outlook. US Vice President delivers a stinging speech on China and slams US corporate for not defending US values. Lower core yields and stronger JPY and USD reflect a tinge of risk aversion in the air while earnings reports keep US equities in the green.

As we suggested earlier in the week we still have plenty of twist and turns ahead of us. So after threatening to pull his WAB if MPs didn’t agree to a swift three day debate and the EU agreed to a long extension, now faced with the prospect of the EU granting a 3 month extension (decision expected later today), BoJo has offered MP’s more time to debate the WAB as long as they agree to a December 12th general election. The general election motion will be put to parliament today with a vote expected to take place on Monday. But not so fast! As always with Brexit, there is a catch, the PM needs 2/3 majority to get the election vote over the line and with Labour behind in the polls, there is no certainty they will agree. Shadow leader of the House Valerie Vaz said Labour would back an election “once no-deal is ruled out and if the extension allows”.

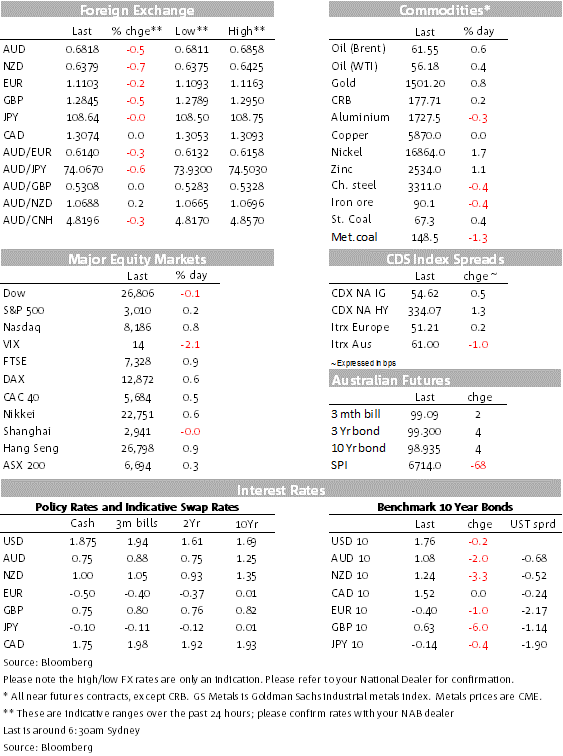

So with election risk back on the table and no certainty Bojo is any closer to getting his WAB passed, the pound is one of the underperformers from the overnight session, down 0.40% to 1.2856, after trading to an overnight low of 1.2789.

As widely expected, President Draghi along with his Governing Council colleagues decided to leave the ECB policy setting and guidance unchanged. At his departing press conference, however, Draghi delivered a gloomy assessment of the Euro-Area economy noting risk to the outlook are “on the downside”, a slightly stronger wording relative to previous characterisation of “tilted” that way.

Consistent with this assessment, Euro-area PMI data were a touch softer than market expectations, with no question that Germany is on the verge of economic recession and the rest of the euro area very sluggish. The US manufacturing PMI was stronger than expected and this will see the consensus pick a recovery in the more widely followed ISM index when released early next month. Core durable goods orders were soft, as expected, with business investment weighed down by the trade war. New home sales dipped but rising mortgage applications put to the upward trend continuing.

US Vice President Pence finally delivered his much awaited speech on China, following a decision to reschedule the speech originally planned for June 4th, on the 30th anniversary of the Tiananmen Square China protest. The Vice president rebuked China for becoming “even more aggressive and destabilising” over the past year, specifically touching on the Hong Kong situation and treatment of Muslim Uighurs in the Xinjiang region. Against a backdrop of rising concern from some voices in Washington that the US President may seek a swift and light trade deal, Pence reinforced the view that the President was committed to a “fundamental restructuring” of the relationship and would “stay the course”. Offering an olive branch, the Vice-President also said that “The United States does not seek confrontation with China. We seek a level playing field, open markets, fair trade and a respect for our values,”. Finally, Pence also had go at US multinationals for seeking access to the Chinese market’s customers and supply chains while leaving their “social conscience at the door”, singling out the NBA and Nike explicitly.

So against a slightly risk off backdrop with renewed Brexit uncertainty, downbeat EU economic outlook and a firm position from the US on China, the USD has regained a bit of its mojo and its up around 0.2% in index terms both against majors and EM/Asia. The DXY index now trades at 97.67 (+0.18%) while ADXY is -0.16%. EUR is down 0.2%, holding in around the 1.11 mark, with not too much damage done by the soft PMI data and with muted reaction to the ECB meeting.

The NZD has been the worst performer since this time yesterday, slipping a little during local trading hours and falling further overnight to 0.6380, down 0.7% and taking it back to the bottom of this week’s (narrow) range. There hasn’t been any obvious news to trigger this, other than a slight risk-off tone feel to markets. The AUD has also been under a little pressure and is down 0.45% to 0.6820. After looking pretty perky the AUD has found the air thinning close to its previous high of 0.6895 on September 12th. Overall recent price action serves as a reminder that while RBA policy is important for the AUD, the aussie remains very sensitive to the mood music on US-China trade tensions and global growth outlook.

A positive start to US equities lost momentum as the overnight session went, that said the S&P 500 looks set to end the day just above the 3000 mark ( +0.19%) while the NASDAQ is +0.81%, the latter buoyed by better that expected Microsoft results after the bell yesterday. As we are about to press the send button, Bloomberg notes that Amazon has reported its first quarterly profit decline in more than two years, missing analysts’ estimates, amid higher spending to speed package delivery. Shares fell more than 7% in extended trading.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.