Coming in for landing in a heavy cross wind

Insight

In the US Jerome Powell spelt out very clearly in his testimony before Congress that more fiscal stimulus was needed and had been assumed by many board members in their policy predictions.

https://soundcloud.com/user-291029717/powell-asks-for-support-debelle-hints-at-easing-nab-revises-rates-forecasts?in=user-291029717/sets/the-morning-call

“What’s it like inside the bubble?; Does your head ever give you trouble?; It’s no sin, trade it in; Hang on, help is on its way; I’ll be there as fast as I can”, Little River Band 1977

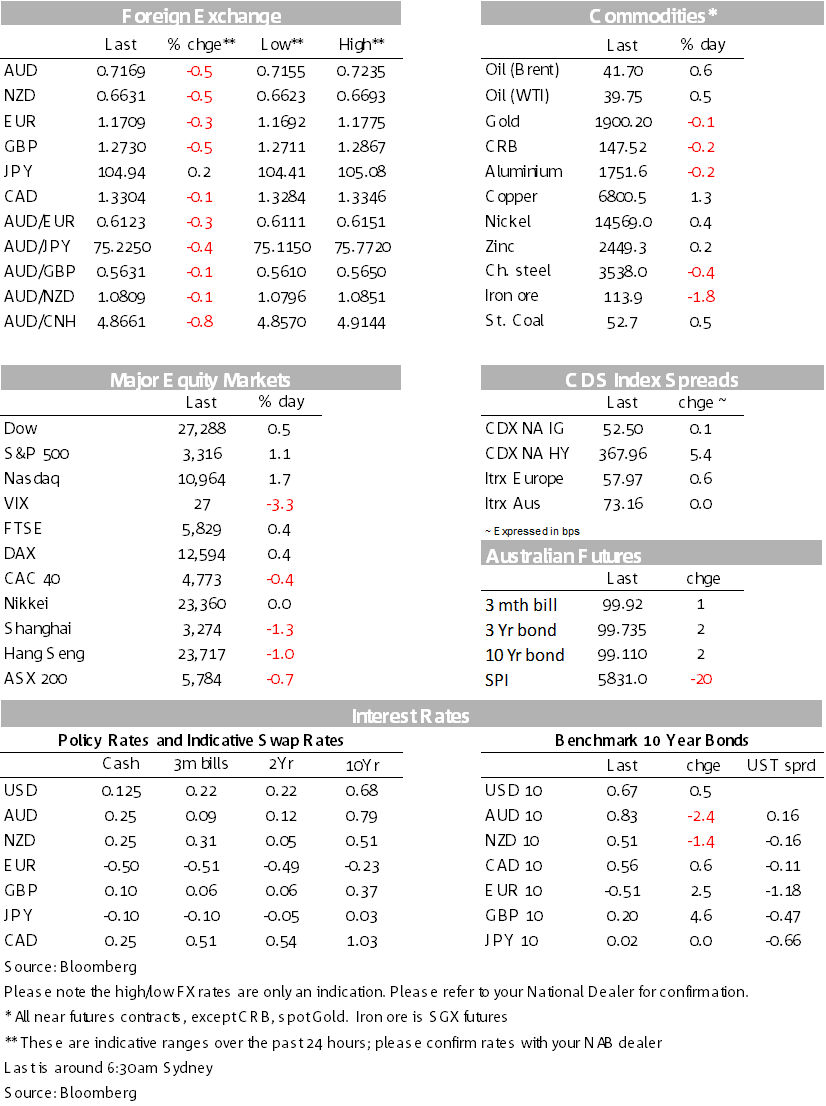

Risk sentiment turned positive overnight with equities snapping four days of declines with the S&P500 +1.1% and the NASDAQ +1.7%. However, there was no catalyst for the move apart from buy the dip and technicals favouring a tech rebound with signs of tech being oversold; the late rally in the ‘hour of power’ on Monday also helping confirm that narrative for some. European equities in contrast were more mixed with the Euro Stoxx50 broadly unchanged at +0.1%. There was also limited flow through to other markets with the USD (DXY) up 0.4% and US 10 yields are little moved at +0.3bps to 0.67%.

Some of the USD move was attributed to misleading headlines when the Fed’s Evans spoke of “FED COULD RAISE RATES BEFORE AVG 2% INFLATION REACHED”, when the thrust of what he said was if the Fed was “timid” and limited its inflation overshoot to 2.25%, then it would take until 2026 or 2028 to average. The more important implication in your scribe’s view was Evan’s comments on QE and reluctance for further easing – reinforcing the narrative post the FOMC that the Fed is showing little willingness to step in and fill the fiscal void given the US Congress continues to seem unwilling/unable to agree to a new package. Chair Powell in testimony overnight reiterated to Congress that more fiscal support would be helpful. Prospects for a new fiscal package have diminished though after Republicans signalled their intention to fast-track confirmation of a new Supreme Court justice before the election. It is also worth noting on the fiscal front that President Trump’s revised unemployment benefit supplement is running out in some states (that program which offered a $300 a week supplement, down from the $600 week, was funded for up to six weeks with at least nine states having already paid out the full benefit according to CNBC).

GBP had another volatile session, with PM Johnson announcing more restrictions given the virus resurgence and BoE Governor Bailey downplaying the probability of negative rates (“in the toolbag but it doesn’t imply anything about the probability of us using negative interest rates at the moment”) and also added that technical preparations for negative rates would take time. The comments plays to our view that if the BoE needed to stimulate in the near term, it would come via increased QE. GBP in the end closed -0.4% with a wide range of 1.2713 to 1.2867, while UK gilt yields rose with the 2-year yield up 7bps and the 10-year up 5bps. As for new COVID-19 restrictions, UK PM Johnson described the current juncture as a “perilous turning point” and asked people to work from home if they could. The government also announced, amongst other measures, that pubs and restaurants would need to close at 10pm and Johnson warned these measures could last for six months. While governments have been reluctant to go back to nationwide lockdowns, moderate restrictions may not work and in the end only prolong the length of necessary restrictions which could then hamper the economy for longer. That appears to have been the experience in Victoria where stagged restrictions eventually gave way to a full lockdown which was then able to control the spread of the virus. The fear for the global economy is if the UK and Europe are unable to control the virus under current restrictions, more stringent measures may be needed over the coming weeks, hampering the global recovery we have seen to date.

The AUD was the underperformer in the G10, down 0.5%, initially in the wake of Debelle’s speech yesterday that flagged further policy easing, and then on USD strength. Australia’s 3-year yield fell to a new record low of 0.2%, below the RBA’s current 0.25% yield target, suggesting the market sees a reasonable risk that the RBA does indeed follow through with easing. As for what Debelle said, in his speech titled The Australian Economy and Monetary Policy, he “outline[d] [the] possibilities for further monetary policy action should the Reserve Bank Board decide that is warranted” and concluded that “the [RBA] Board will continue to assess the merits of the range of monetary options to best support the economic recovery”. NAB expects the RBA’s preferred further easing options to be announced at either the October or November Board meetings, NAB yesterday changed its rate call and is now expecting the RBA to cut the cash rate, 3-year yield target and TFF rate by 15bps to 0.10% (from 0.25%). We also expect the RBA to announce outright QE purchases in the 5-10 year area of the curve, so as to lower longer-dated rates to provide stimulus via the portfolio rebalance effect/a lower $A. Different to YCC, this would likely require a nominated quantum of bond purchases per period to be announced. While NAB remains of the view that further monetary easing will have only marginal impact on the economy, the RBA continues to signal that it will do what it can to support the recovery: “given the outlook for inflation and employment is not consistent with the Bank’s objectives over the period ahead, the Board continues to assess other policy options”. Fiscal policy also continues to be well-placed to support the recovery and further measures are expected to be announced on this front in the Budget on October 6. It is also worth emphasising the RBA continues to rule out negative rates (“empirical evidence on negative rates is mixed”) and the Bank is very reluctant to intervene in the exchange rate (“AUD broadly aligned with its fundamentals”), citing the experience of the Swiss National Bank in today’s speech.

Finally in Australia, Weekly ABS payrolls were broadly stable, falling 0.1% in the week to September 5, though are down 0.7% over the past four weeks. The rapid recovery seen in payrolls to date appears to have slowed with states outside of Victoria seeing a slight fall in payrolls of 0.2% over the past four weeks, while a sharp fall was seen in Victoria (-2.1% over the past four weeks) given the lockdown. To date, around 50% of all payroll jobs lost in the initial months of the pandemic have been recovered, though this still leaves jobs down 4.5% from pre-COVID levels (Chart 1). Looking ahead, with Victorian virus numbers coming within re-opening benchmarks, we will be watching how quickly the Victorian labour market can bounce back. Such a prospective bounce will also be occurring as JobKeeper and JobSeeker is tapered at the end of September and it will be important to monitor the trends in states outside of Victoria for any possible impact. Finally, the stabilisation in the rebound seen in states outside of Victoria (particularly WA) has potential implications for how far state economies can bounce back in an environment of social distancing and when interstate and international borders remain closed – some have termed this the 90% economy.

Domestically, markets are likely to continue to digest the implications from Deputy Governor Debelle’s speech yesterday and assess whether the RBA is likely to cut rates and expand QE as soon as the October meeting. Datawise we get a preliminary read on retail sales. Across the ditch the RBNZ meets, but with no change and refraining from signalling any policy shifts. Offshore, global PMIs will be closely watched on both sides of the pond given the virus resurgence in Europe and the reduction in the unemployment benefit supplement in the US. Consensus sees little impact from either. There is also a bevy of Fed speakers (eight in total) with Powell the one to watch:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.