Total spending grew 0.9% in June.

Jerome Powell has sent the markets back to where they were before the non-farm payrolls data last week.

https://soundcloud.com/user-291029717/powell-ignores-payroll?in=user-291029717/sets/the-morning-call

Today’s titular song reference has nothing to do with Mr Powell, rather a hat tip to the fantastic bowling performance by the Black Caps last night. Time for our kiwi cousins to check whether there’s any of that 2013 vintage champagne still in the fridge ahead of Sunday’s final (against the Poms of course).

It’s also a plug for the debut album release tomorrow by indigenous Australian singer Thelma Plum, who I predict will be huge in the coming years (just as your scribe did Tash Sultana back in January 2017 if anyone recalls – if only some of my FX calls were as good). For those with access to YouTube, you can listen to the title track of Plum’s album here: BetterinBlak (language warning).

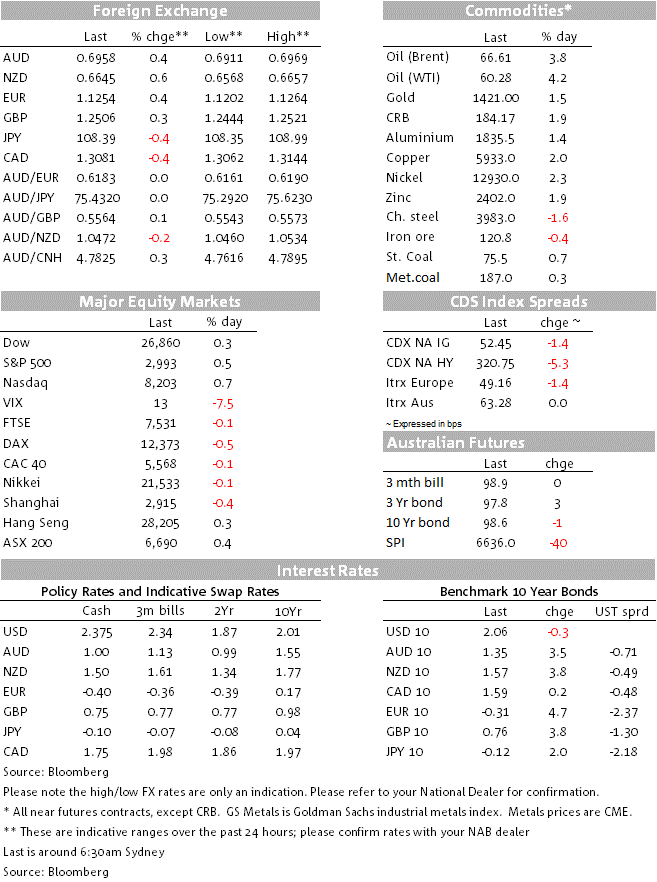

As for markets, anyone fearful that Fed chair Jay Powell might be about to cast aspersions on the likelihood of the FOMC agreeing to cut rates when it next meets on July 30th and 31st needn’t have worried. Indeed, money markets are back showing non-trivial odds of the Fed cutting by 50bps, now priced at about 30% versus 6% this time yesterday and with very slightly more than -100bps priced for 2021 (103bps to be precise).

In the prepared statement prior to Powell’s Q&A, which wasn’t identical to the one he delivered to Congress ahead of time last Friday, the money paragraph read:

‘In our June meeting statement, we indicated that, in light of increased uncertainties about the economic outlook and muted inflation pressures, we would closely monitor the implications of incoming information for the economic outlook and would act as appropriate to sustain the expansion’.

‘Many FOMC participants saw that the case for a somewhat more accommodative monetary policy had strengthened. Since then, based on incoming data and other developments, it appears that uncertainties around trade tensions and concerns about the strength of the global economy continue to weigh on the U.S. economic outlook. Inflation pressures remain muted.’

In the subsequent Q&A, Powell noted the risk that “weak inflation is more persistent than expected”. No longer any reference to ‘transitory’ from the Fed chair. Furthermore, in the FOMC Minutes released a couple of hours ago, they note that ‘many Fed officials In June saw risk weighted to the downside’ and also that ‘many saw inflation expectations as inconsistent with the 2% goal’.

So while the ’25 or 50?’ debate has been rekindled post-Powell – in which respect in answer to that specific question Powell noted only that “we’ll be looking at a full range of data between now and the end of the month” noting some of it is “important” – Fed activist James Bullard has been on the wires in the last hour or so repeating his view that a 50bps cut this month would be overdoing it. He said he would call for a 25bps cut this month and look for another 25bps before year-end.

Bullard also says that a Fed Governor nominee Christopher Waller has views “close to his”. Waller has, in our view, much more chance of getting his nomination approved in the Senate than Judy Shelton (about whom Jay Powell declined to comment last night, though he did say he didn’t think it would be a good idea to return to the gold standard, one of Shelton’s key policy prescriptions). Incidentally, Fed says he won’t leave if Trump tries to fire him, saying he has a legally mandated 4-yar term.

The upshot of latest Fed communications has been a partial reversal of the recent run up in both US bond yields and the dollar. US 2-year Treasury yields are 8bps lower on the day so far at 1.83%. And while 10s are barely changed on 24 hours ago, they are down from an intraday high of 2.11% to 2.06% now.

US equities continue to listen to the interest rate messaging out of the Fed not the underlying reasons for it, the major indices closing up by between 0.3% (DJIA) and 0.8% (NASDAQ). Within the S&P500’s 0.5% gain, Energy (+1.4%, on higher commodities) and Communication Services (+1.3%) are the best performing sectors.

In currencies, the narrow DXY index is 0.4% down at 97.12. USD dollar losses are fairly evenly distributed across the G10 spectrum save for a 0.9% rise in NOK, with NZD (+0.54% to 06645 faring a bit better than AUD (+0.43% to 0.6959 now and a high of 0.6969). The antipodean currencies have both fared slightly better than European currencies or CAD, all up between 0.3% and 0.4% versus Tuesday’s’ New York close.

The Bank of Canada left its policy rate unchanged at 1.75% as widely expected but hasn’t dislodged market pricing that still ascribed about a one third chance to a 25-point rate cut by the end of September. This on the basis that the central bank made repeated reference to risk from trade protectionism in the one-page statement (subsequently, Deputy governor Wilkins said that trade issue could reduce the level of Canadian GDP by up to 2% through 2021). That said, BoC Governor Stephen Poloz in his post-meeting press conference echoed what is rapidly becoming a familiar refrain from central bankers, namely that you “shouldn’t assume monetary policy can fix the impact” of a trade war.

Prior to the Powell testimony, both the EUR and GBP received slight boosts from better than expected economic data, in particular French industrial production coming in at +4%m/m vs. +1.6% expected – all those yellow vest protestors returning to work presumably – and UK production very slightly better than expected at 1.5% (1.4% forecast). UK Construction Output was also better than expected at 0.6% on the month (0.1% consensus) while the monthly (May) GDP read was 0.3% in line with expectations.

Commodity markets have all benefited from the Fed messaging and softer US dollar, save for some minor slippage in iron ore and steel futures. Oil is up ±4%, base metals mostly +1-2% and gold by $20 to $1,418 and versus it‘s recent (June) high of $1,439.

AU May Home Loans. NAB expects that home loan approvals likely fell further in May, looking for a larger fall of 2% in owner-occupier approvals relative to the consensus of a 1% fall. Home loan approvals have been falling for some time and we suspect that uncertainty around the federal election in May weighed further on approvals. These data will be important to watch in coming months. Anecdotal evidence suggests that inquiries to property developers picked up sharply post the election, although inquiries have not necessarily translated into sales.

Tonight (23:10 AEST) RBA Deputy Governor Guy Debelle will give a speech by video conference to the FX Week New York conference (remarks to be published on the RBA website)

The US has CPI (core seen +0.2% m/m for an unchanged 2.0% y/y), weekly jobless claims

Fed Chair Powell delivers the second of his Humphrey Hawkins testimonies, this time to the Senate Banking Committee, commencing at midnight AEST

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.