Coming in for landing in a heavy cross wind

Insight

Trump tweeted as Jerome Powell spoke saying shares were falling the more he spoke.

https://soundcloud.com/user-291029717/powell-talks-shares-down-aussie-rises-britain-on-hold-rbnz-today?in=user-291029717/sets/the-morning-call

US stocks have been rallying, reportedly due to subsidence from peak coronavirus fears, after the rate of new infections reported by China yesterday (for February 10) was smaller than the day before and some factories in China have begun to re-open, including Airbus and Caterpillar. No matter that the China’s health commission has reportedly changed the way infection cases are henceforth to be reported, with patients testing positive for the virus but not displaying symptoms no longer to be counted in the statistics. This is at a time when some 160 million Chinese are said to be about to return to the cities to restart work in the factories. What could possibly go wrong?

Meanwhile and reminiscent of the PFJ Union meeting scene in Life of Brian, it’s reassuring to know that the World Health Organisation, slow off the mark to classify the nCoV outbreak as an epidemic have, one month on, now agreed an official name for the virus, Covid-2019.

In truth, US stock market gains also owe something to M&A news, yesterday’s news of approval of the T-Mobile-Sprint merger more than two years after it was first announced, seeing the shares of both telecom firms rise strongly, Sprint by some 75% in what will in effect be an (all-stock) takeover of the Softbank-owned wireless operator by Deutsche Telkom-owned T-Mobile. Amazon, up over 2% earlier in the session, has been the biggest contributor to the overall gains for the NADAQ and S&P, but where both indices are well back from their intra highs coming into the close, now +0.09 and 0.05% respectively.

On this pull back, POTUS has been quick off the mark with new criticism of Fed chair Jay Powell, viz, “When Jerome Powell started his testimony today, the Dow was up 125, & heading higher. As he spoke it drifted steadily downward, as usual, and is now at -15. Germany & other countries get paid to borrow money. We are more prime, but Fed Rate is too high, Dollar tough on exports”

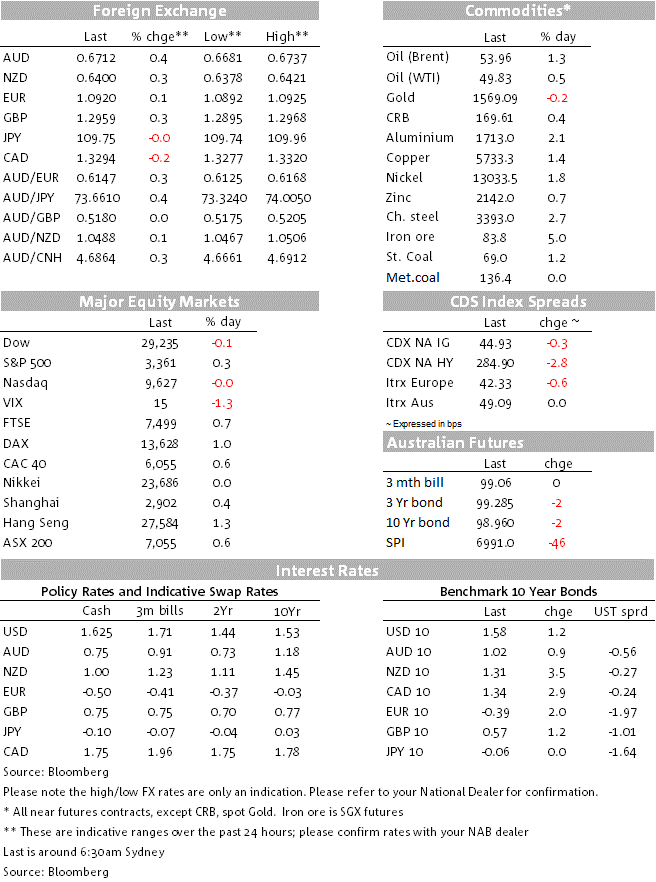

The USD is a bit softer versus where we left it yesterday, the DXY index currently -0.13%, with the drift lower commencing some time before Powell started speaking. There’s no obvious catalyst for the slippage. EUR (57% of DXY) is little changed but GBP (12%) and CAD (9%) are up 0.4% and 0.2% respectively. GBP is up after Q4 GDP came in unchanged on the quarter as expected but December alone was +0.3% suggesting a bit of positive (post-election) momentum heading into 2020, albeit industrial production at 0.1% in December was softer than the 0.3% expected. Confirmation that the go-ahead has been given for the £100bn+ ‘HS2’ high speed rail network may also have been helpful to the GBP cause via the prospect of a fiscal boost to the economy (we’ll learn more in the March 11 Budget).

Neither AUD or NZD feature in the DXY of course, but AUD/USD is (just) pipping GBP/USD to top slot in the G10 leader board, up 0.4% on Monday’s NY close to 0.6714. Gains during our time zone yesterday, that have been slightly extended overnight, look to be more a function of the firmer CNY(+0.25%) than yesterday’s strong housing finance data and failure of the latest NAB business survey to show any significant hit to business confidence or conditions from the bushfires.

There was nothing in his opening prepared statement to move markets, repeating the all too familiar mantra of the needing for a material change in the outlook for the Fed to deviate from a steady as she goes policy course in 2020. Powell said “”The FOMC believes that the current stance of monetary policy will support continued economic growth, a strong labor market, and inflation returning to the Committee’s symmetric 2 percent objective. As long as incoming information about the economy remains broadly consistent with this outlook, the current stance of monetary policy will likely remain appropriate. Of course, policy is not on a preset course. If developments emerge that cause a material reassessment of our outlook, we would respond accordingly”.

Risks to the outlook, via a hit to Chinese and global growth from the coronavirus, subsequently rated a mention (Fed is ‘closely monitoring’) but unlike the views of POTUS, not the strong dollar.

US data overnight included a strong NFIB small Business Optimism Survey (104.3 from 102.7 and above the 103.5 expected, doubtless aided by strong market gains) but another big fall in job-openings (JOLTS 6,423k in December down from a downward revised 6,787 in November and against a rise 6,925 expected). This was one of former Fed chair Janet Yellen’s favourite labour market statistics, and is suggestive a significantly slower monthly payroll gains down the not too distant track.

In conjunction with firmer US stocks and an apparent easing in coronavirus concerns, US treasury yields are a touch firmer, 10s by 1bp to 1.58% and 2s +2bps to 1.41%.

Commodities are also mostly firmer, Brent crude +60 cents to $53.96, base metals all stronger with copper +1.4% and aluminium +1.9% and Singapore iron ore futures a full 5% to $83.80.

RBA’s Alex heath is due to speak shortly (07:50 AEDT) in Sydney at the Abe’s forecasting conference.

Westpac January consumer confidence is at 10:30

The RBNZ’s policy announcement is at 12:00 AEDT)

Tonight we get EZ industrial production (slated to be down by at least 2% after German French nd Italian numbers already released) . ECB chief economist Lane is due to speak in Dublin

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.