Confidence and Conditions Lift

Insight

There’s been a sharp rise in US equities after comments from the Fed’s Jerome Powell, signalling rate cuts are likely.

https://soundcloud.com/user-291029717/powells-balancing-act-lowe-hints-at-further-cuts?in=user-291029717/sets/the-morning-call

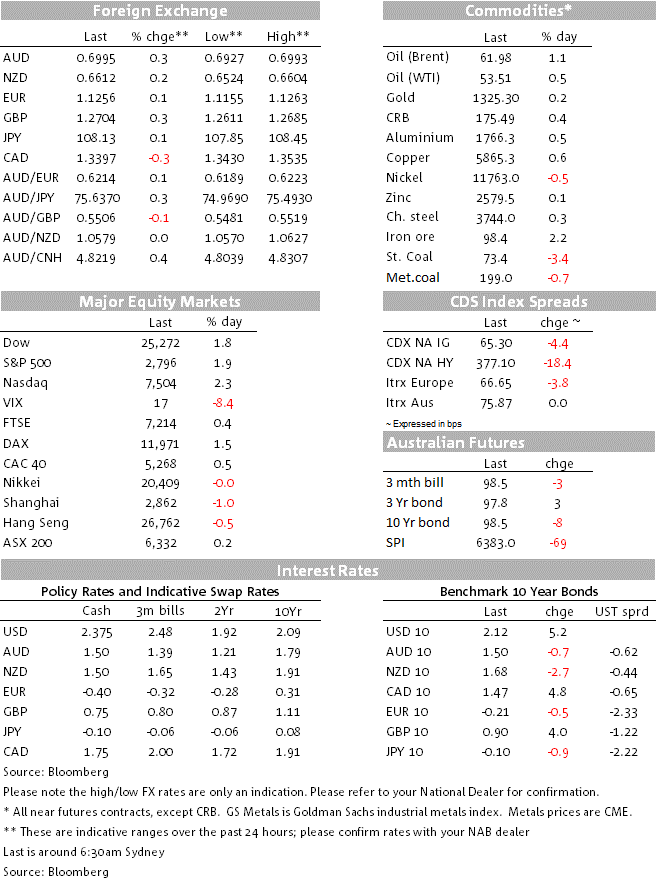

US equities rebounded smartly overnight boosted by soothing words from Fed Chair Powell alongside optimistic comments from Mexican officials lifting hopes of an end to the US-Mexican stand-off. UST yields bounced off their lows on the improvement in sentiment and lack Fed funds pricing endorsement by Powell. USD soft trading continues with GBP and commodity link currencies the outperformers. RBA Lowe say “not unreasonable to expect a lower cash rate”, but much will depend on the labour market outlook.

Fed Chair Powell speech hit the right balance appeasing equity markets by confirming the Fed stands ready to act in order to sustain the current economic expansion if trade tensions hamper US economic growth. But at the same time ,the Fed Chair also warned that “Using monetary policy to push sufficiently hard on labour markets to lift inflation could pose risks of destabilizing excesses in financial markets or elsewhere,”. So while appeasing the equity market on the one hand, on the other hand Fed Chair Powell effectively rejected the recent aggressive pricing of Fed rate cut expectations. His comments also highlight the importance of the labour market on the Fed ‘s thinking, suggesting the recent UST rally could be at risk of a reversal if we get a solid non-farm payrolls report on Friday.

Also talking a good game and backing the Fed Chair’s position, Chicago Fed President Evans pushed against the idea of any market pressure to cut rates, saying that “With inflation being a little bit on the light side, there’s the capacity to adjust policy if that’s necessary, but the fundamentals for the economy continue to be solid. The consumer is solid. I think we have to think through what this really means.” In a CNBC interview, vice-chair Clarida said that Fed policy wouldn’t be “handcuffed” to market prices and he was generally upbeat about the economy.

US equities enjoyed a very solid session with sentiment also boosted by comments from Mexico’s Foreign Minister saying there’s an 80% chance that the country will be able to avoid tariffs. However, during a visit to the UK Trump said that the US will likely move forward with applying the 5% tariffs to Mexican products next week. Mexico has indicated that it’s prepared to retaliate against the tariffs, choosing retaliatory measures strategically. In spite of Trump’s comments, all major US equity indices recorded gains over 2%, the S&P 500 closed at 2.14% with carmakers and chip manufacturers leading the gains.

The improvement in risk sentiment and lack of Fed funds pricing endorsement by Fed speakers lifted UST yields along the curve with the 10y tenor climbing 4bps to 2.1296% while the 30y rate jumped 6.44% to 2.596%.Fed pricing expectations also ease a bit with the market now pricing a 62bps of Fed rate cuts before the end of the year, about 5bps lower relative to yesterday’s levels. Meanwhile in Europe, 10y Bunds closed unchanged at -0.201%, overnight, EU inflation missed at both the Headline and Core by a tenth in May (details below). It is clear that Core Inflation continues to under-club the ECB’s inflation target (of close to 2%) and importantly inflation expectations have fallen back to their lowest levels since 2016 (5Y5Y inflation swap now 1.29%, down from 1.6% at the end of 2018, and almost at its life-time low 1.28%). ECB meets on Thursday and it is very likely their new forecast will reveal downgrades to the Bank’s inflation outlook, talk of the new TLTRO is likely to be the focus, but can the ECB wait for a new president before announcing further stimulatory measures?

Meanwhile in currency land, the USD has continued to trade with a soft tone notwithstanding the relative move higher in UST yields. In Index terms the USD was weaker against both majors ( DXY -0.09% to 97.129) and EM currencies (EMCI +0.37%). MXN had good day (+1.05%, now at 1956) reversing some of the losses incurred early in the week while in G10, GBP and commodity linked currencies were the outperformers.

President Trump is in the UK and he promised a “phenomenal” trade deal if the UK leaves the EU, but controversially he also added the caveat that NHS would need to be part of the discussion ( good luck with that!). Cable now trades at 1.2699, up +0.37% over the past 24 hours.

The AUD momentarily broke up through 0.70 this morning on USD weakness, but the pair now trades at 0.6991.There was little sustained market reaction to the widely anticipated RBA rate cut yesterday to 1.25% or Governor Lowe’s speech last night. The positive overnight backdrop also helped the AUD, iron ore and oil prices had a good night ( see table below) while the unwinding of USD longs also appears be at play. Why cut the cash rate? The Governor noted that because despite strong employment growth, spare capacity was likely to remain with the possibility then of inflation staying too low for too long – a problem because it would then weigh on inflation expectations and possibly make the inflation target harder to reach (note 5Y inflation swaps are 1.6%). What the outlook? Dr Lowe stated “it is not unreasonable to expect a lower cash rate” and forecasts were conditioned on a technical market rate assumption of 1%. Importantly though, much depends on how the labour market evolves. NAB forecasts a further reduction in the cash rate to 1% at the Bank’s August Board meeting – and the risk of a further reduction in the first half of 2020, amid our expectations of further softness in the labour market and somewhat slower growth in the horizon.

Last but not least, against a soft USD, the NZD is up to 0.6610 mark, close to its highest level in a month. The GDT dairy auction confirmed that prices have likely peaked after a strong run, with the price index down 3.4%. As we noted in our weekly FX commentary yesterday, in broad terms, the NZD is being pulled in two directions. On the negative side, a weaker global growth dynamic, alongside weaker commodity prices is a major headwind for NZD performance. On the positive side, a possible major turning point in the USD trend might only be just beginning. The latter has been central to our forecasts for some time, which has underlined our year-end target of 0.70. This currency tug-of-war is likely to continue over coming weeks until we have some clarity about the outlook. Much will depend on Trump’s next moves on tariffs and how his meeting with President Xi goes at the end of the month

We have revised our Q1 GDP forecast from 0.4% q/q / 1.7% y/y to 0.5% q/q / 1.8% y/y given Monday’s inventories data were stronger than expected and yesterday’s the partials were also solid: net exports contributed 0.2ppt to growth (NAB, mkt: +0.2ppt), while public demand contributed 0.2ppt on the back of strength in public consumption. The RBA’s implied forecast is for 0.6% growth in GDP, while the consensus is currently for a 0.4% rise.

Consensus is looking for an almost unchanged ISM Non-Manufacturing Index print in May (54.5 vs 55.5), so still comfortably in expansionary mode, but slowing relative to the 2018 average of 58.9.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.