Online retail sales growth slowed in May following a fairly strong April

Insight

The US President offered nothing new about where trade talks are at and the markets little moved.

https://soundcloud.com/user-291029717/president-talks-but-gives-nothing-away?in=user-291029717/sets/the-morning-call

You say it best, When you say nothing at all – Ronan Keating

The much awaited Trump was heavy on rhetoric and light on detail, leaving markets none the wiser. A positive lead from Europe, earnings reports and solid US data boosted US equities early in the overnight session with the market showing a bit of disappointment after President Trump’s speech, giving back some of the early gains. Moves in core yield have been pretty subdued and the USD has made broad, but modest gains with NZD underperforming post yesterday’s softer than expected inflation expectations print and ahead of today’s RBNZ decision.

President Trump gave an uplifting speech at the Economic Club of New York and with one eye on the November elections next year. The President talked up the economy noting how American Markets have “vastly outpaced” the rest of the world, he also delivered his customary criticism of the Fed (Far too slow in cutting rates while other Central Banks are cutting interest rate) and in the end didn’t give much away in terms of Trade negotiations with China and or Europe for that matter. The President said that “We’re close. A significant phase one trade deal with China could happen, it could happen soon.” but “If we don’t make a deal, we’re going to substantially raise those tariffs,” adding “ that’s going to be true for other countries that mistreat us too”.

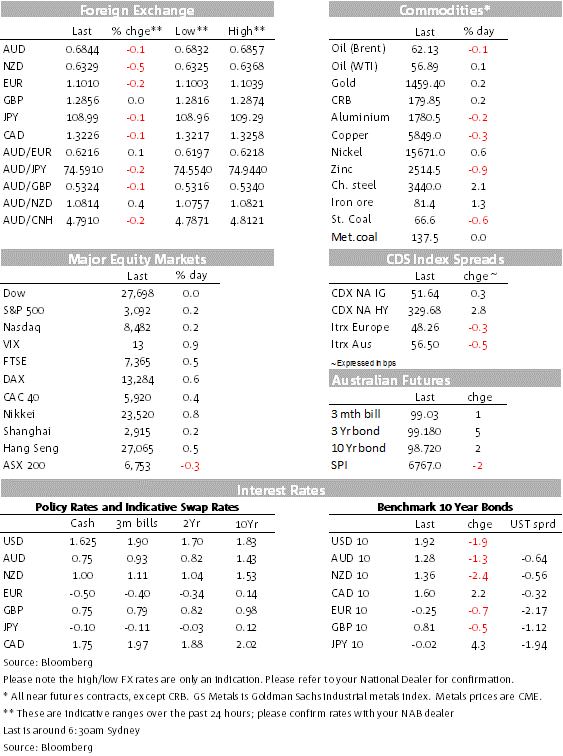

US equity markets were travelling in a subdued but upbeat mood, boosted by a positive lead from Europe, good earnings reports and a solid NFIB survey. European equity markets closed higher, (Euro Stoxx 50 up 0.4%, FTSE 100 up 0.5%, DAX up 0.6%, CAC 40 up 0.4%, IBEX -0.87%) with IBEX the exception following news the Spanish Socialist party struck a coalition deal with left wing Podemos. European Telecoms led the gains as Vodafone jumped 3.1% after reporting sales growth in the second quarter. Health care shares led the gains in the US as drugmaker AbbVie rose on the back of what may be the largest bond sale of the year to fund its Allergan acquisition. Walt Disney also advance following the unveiling of its streaming service. As we are about to press the send button US equities are paring back earlier gains reflecting disappointment on the lack of new trade news from President Trump’s speech. S&P 500 noa trades 0.10% on the day after being 0.50% at one point, briefly trading above the 3100 mark.

It was mostly good news. France’s BdF Industry Sentiment for October was a little better than expected at 98 after 96 and 97 expected, Germany’s Survey for November showed a big improvement in German expectations (from -23.5 to -1.0 ) although current conditions remain negative and little changed (24.7 after -25.3 and below f/c -22.3). UK labour market data showed falling employment and softer wage inflation, although the “discouraged worker” effect saw the unemployment rate nudge back down to 3.8%.

The small business survey (NFIB) showed an insignificant lift in confidence, but encouragingly a small lift in capital spending expectations. Commenting on capex, the Survey found “Trade policy is impacting many small firms adversely; about 30 percent recently reported negative impacts. Making commitments about production and distribution will be more difficult until import and export prices are stabilized with trade agreements”. The survey also reported tight labour markets restricting expansion and capex because of skilled labour shortages, reflected also in higher compensation, though not in selling prices.

The USD has made broad but modest gains with the DXY index up 0.11% to 98.30 and BBDXY +0.17% to 1204.9. NZD is the big underperformer in G10, falling -0.47% over the past 24hrs following yesterday’s release of a softer than expected inflation expectations report. The RBNZ’s survey of expectations showed 2-year inflation expectations slipping from 1.86% to 1.80%. While the slippage was forewarned by the ANZ survey and soft headline CPI data, this was enough to see Westpac change its OCR call again and move into the pack seeing a 25bps cut later today. OIS pricing for today’s meeting fell 4bps to 0.81%, suggesting that the market is now 76% priced for a 25bps cut (up from a 60% chance). The NZD was weaker heading into the inflation expectations report and it fell further after its release, seeing it unwind its outperformance during the overnight session and finding support at 0.6330, back to where it began the week.

Yesterday’s fall in the kiwi dragged the AUD to an intraday low of 0.6832, but after an up and then down pattern the aussie is now little changed and currently trades at 0.6844. Amid uncertainty on the US-China trade front the AUD continues to find the air thinning just above the 69c mark. Today’s Wage price index is the domestic focus ahead of the Labour force report tomorrow.

GBP is little changed at 1.2854. There has been lots of press coverage on Farage’s decision yesterday not to stand candidates in Tory seats, a big boost for the Conservative Party. The FT has suggested that Farage could also give the Tories a clean run against Labour seats too, but this morning press reports suggest Brexit Party leader Farage has snubbed calls not to contest Labour seats. A YouGov poll release overnight shows the Conservatives 42% vs labour 28% ( 39% vs 26% previously).

The Bank of America’s November survey of fund managers showed a bullish tilt towards markets, with net expectations for a stronger world economy back into positive territory for the first time in over a year. Cash levels plunged to their lowest level since mid-2013 as managers reallocated to equity markets, seeing them as the best performing asset class, ahead of commodities, while bond allocations were also cut.

Events in Hong Kong remain a concern with the local police noting that Hong Kong’s rule of law has been pushed to the “brink of total collapse” after more than five months of protests. China’s top agency overseeing Hong Kong on Tuesday said it firmly supported Hong Kong’s government and police to act more strongly and effectively to punish crimes and restore order, Xinhua News Agency reported.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.