Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

It’s a sea of red for global equities and US bond yields.

https://soundcloud.com/user-291029717/q4-off-to-a-bad-start-as-stocks-tumble-on-slowdown-fears?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know.

Good times, bad times, You know I had my share – Led Zeppelin

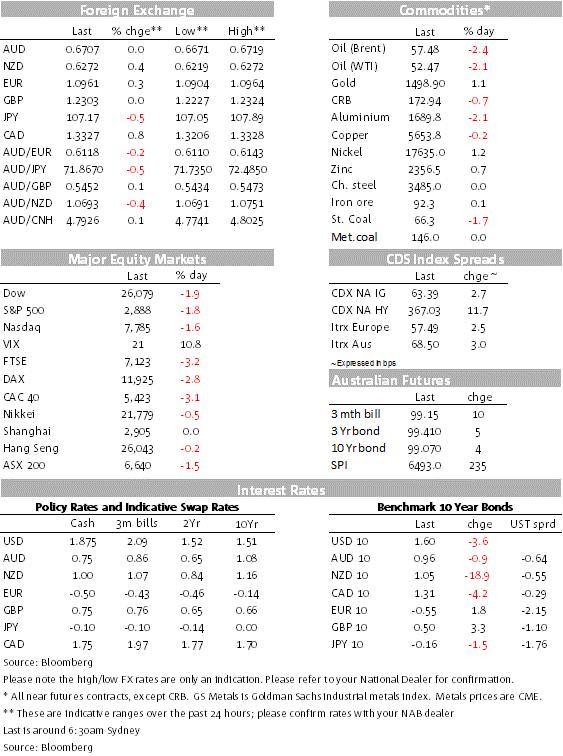

Well some say bad news come in three and after yesterday’s disappointing ISM manufacturing, risk sentiment has taken another beating overnight following news of a WTA ruling allowing the US to impose tariffs on EU products while also raising the prospect of EU retaliation. Earlier in the session, a soft ADP report didn’t help the mood adding concerns over the resilience of the US consumer. US and EU equity indices closed sharply lower while short dated US Treasuries led the decline in yields. GBP had a volatile session as PM Johnson delivers his Brexit plan, AUD is unchanged while NZD enjoyed a decent bounce.

The WTO has allowed the US to impose close to $7.5bn in tariffs on EU products ranging from wine, whisky, luxury goods and aircraft parts in order to repair damage done to Boeing by illegal EU aid to Airbus. But the WTO also has found that Boeing received illegal tax breaks and government-research windfalls, and will rule next year on whether the EU Commission can also apply retaliatory tariffs.

Reacting to the news, departing EU trade commissioner Cecilia Malmstrom said that the ruling has ” comes at an unfortunate moment in time, because this has been going on for almost two decades” adding that she had “not received any positive (US) response” to EU trade proposals to sidestep new tariffs. A French trade official was also quoted as saying that if the U.S. persist to use this strategy to put tariffs, of course, the EU must answer.”.

So against a back drop of slumping global manufacturing activity, the market has reacted badly to the prospects of an escalation in US-EU trade tensions. Earlier in the session, the US ADP private sector payrolls estimate printed at +135K in September, below the 140k expected by consensus while the August number was revised to 157k from 195k. The ADP report has a patchy record in predicting what the US non-farm payrolls will look like, but amid a heightened level of concern over the resilience of the US consumer, the soft report added another layer to the ongoing market uncertainty.

Main EU equity indices closed 2.5% to 3% lower while in the US the S&P 500 ended the day -1.79% and the NASDAQ was -1.56%. Looking at the Bloomberg Europe 500 index and the S&P 500 in the US, all sectors in both indices show hefty declines with consumer discretionary, IT and energy at the bottom of the pile. The latter likely not helped by a ~2% drop in oil prices following a report showing US crude inventories had increased. Auto makers in the US also underperformed with disappointing reports from Ford and GM confirming the dire picture in the sector which was already evident in reports from Japanese auto US sales the day before.

The souring in the risk sentiment triggered a bid in US Treasury yields with shorter date tenors leading the decline. The 2y rate fell 6.2bps to 1.485% and the 10y note now trades at 1.5957, 3.5bps lower on the day. The down trend in 10y UST yields evident since late 2018 remains in place and now with the move sub 1.60% many will be looking at the previous low of 1.467% as the next major resistance.

The USD is little changed and mixed in index terms. DXY is -0.11%, largely reflecting gains in JPY while against EM, the USD is a tad lower ( -0.23%) but against Asia FX the USD is a tiny bit stronger (ADXY +0.06%).

The move lower in UST yields is probably the main factor for JPY outperformance with USD/JPY,-0.51% down on the day. The steepening in the JGB curve and GPIF changes in its offshore bond allocation played into JPY weakness earlier in the week helping USD/JPY trade to an intraday high of ¥108.45 yesterday, but the following sharp decline in 10y UST yields has become an overriding force with pair now trading at ¥107.18. The risk aversion evident in equity markets has also played into JPY’s safe haven bid.

EUR is also a tad higher +0.23%, but bucking the trend, it is surprising to see CHF as part of the overnight underperformers, down 0.37% at 0.9971. Overnight Swiss inflation in September missed median estimates and was the lowest in almost three years. Deflationary concerns and a strong CHF have increase the prospect of the SNB lowering its already super negative interest rate.

Notwithstanding the risk off mood, the AUD is little changed at 0.6707, after trading down to an overnight low of 0.6671. The sharp decline in shorted date UST yields on the back of soft data and trade tension news has increased the prospects of the Fed lowering the funds rate again later in the month. Since Monday pricing expectations for an October Fed funds rate cut have increased from 41% to 74% currently, this has been a drag for the USD, but probably worth noting too that the RBA has become very sensitive the rate decision by other major central banks with RBA Governor on Tuesday acknowledging that “lower interest rates globally” was one influence on the Bank’s decision to lower the cash in Australia. So the Fed easing again will increase expectations on the RBA to follow shortly after.

Somewhat unusual, the NZD is the G10 outperformer today, making a massive U turn around 8pm last night. The USD was under broad pressure, but the outperformance of the kiwi has been impressive. After trading down to a low of 0.6219, the pair now trades at 0.6269 , we can only attribute the outperformance of the NZD overnight to short covering; we have noted in recent weeks the build-up of large speculative short positions in the NZD according to CFTC data.

The GBP hasn’t shown much movement to Boris Johnson’s unveiling of his plans for the Irish border, which were mostly leaked to media yesterday. Johnson’s proposal is that Northern Ireland should remain aligned to EU rules on food, agricultural and manufactured goods and freedom of movement of people would be respected, in order to get over most of the issues on the border (although there would still likely need to be some checkpoints away from the border itself). This would be a special temporary arrangement for four years until start 2025, at which time the Northern Irish parliament would vote on whether to extend the arrangement or not. The plan received a positive response from both the DUP and Brexiteers but Irish Prime Minister Leo Varadkar said the backstop proposal didn’t fully “meet the agreed objectives”. EC President Juncker said there were “positive advances” and didn’t rule out the plan but said it had “some problematic points”. The question appears to be whether there is enough middle ground for the two sides to come to some sort of agreement by the time of the EU Summit on October 17th.

Bernie Sanders, the US Democratic presidential candidate has undergone a heart procedure for an artery blockage after experiencing “some chest discomfort” at an event on Tuesday. All campaign evenst have been cancelled until further notice. An adviser for the Vermont senator said he was in “good spirits” and will be resting over the next few days, It is unclear how long Mr Sanders will need to recover and whether he will be able to attend next Democratic debate on 15 October.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.