Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Europe's done it, Australia's done it. Now it's the US' turn to extend their fiscal support, and the deadline is looming.

Keep pushin on, Things are going to get better

It won’t take long ,Keep-on pushin to the top

Keep on movin, movin, Keep on pushin-pushin to the top – Boris Dlugosch

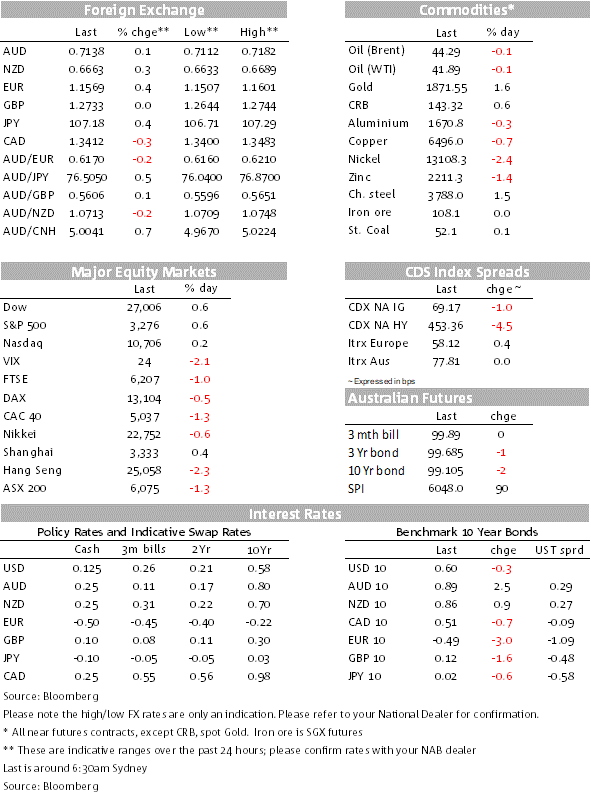

Well as it has been the case for quite some time, the resilience of US equities remains unabated no matter what you throw at them. All major US equity indices have ended the day higher, notwithstanding an increase in US-China tensions and another daily record of virus infections in California. The USD has extended its decline with AUD and NZD making fresh new highs. Movement in core yields remain subdued, although the rally in Italian BTPS continues.

In a move with huge diplomatic consequences, early in the overnight the US gave China three days to close its Houston Consulate. The US State Department said it ordered the consulate shut “to protect American intellectual property and Americans’ private information,” without giving more details. When asked about the decision at a briefing later in the day, US Secretary of State Michael Pompeo said “We are setting out clear expectations for how the Chinese Communist Party is going to behave and when they don’t we’re going to take actions that protect the American people,”.

The US has consulates in Shenyang, Shanghai, Chengdu, Guangzhou and Wuhan, so it seems like a good bet that one of them will be asked to shut.

The Houston news triggered a mini collapse in the S&P 500 futures during the European session (-0.86%) and a small rally in UST (2bps decline in 10y UST to 0.5807%). All major European equity indices ended the day with losses between 0.5% and 1.40% with mixed earnings reports. Quarterly losses for major energy companies saw the BBG Europe 500 energy sector end the day down by 2.75%. Meanwhile and as it been the case since the Fed began its huge stimulus late in March, US stocks rebounded during the US session with the S&P 500, NASDAQ and Dow all closing in the green.

The USD continues to find no loving, recording its fourth consecutive day of decline in index terms. Both BBDXY and DXY indices are down ~0.15% and technically they still have room to decline a little bit more. For instance, BBDXY now trades at 1193 with key support is seen around the 1183 area.

Similar to US equities, the increase in US-China tension has not had a lasting impact. For instance, although the Houston news contributed to the recording of overnight lows for both the AUD ( 0.7112) and NZD (0.6633), as US equities rebounded both antipodean currencies regained their mojo and ended the day stronger. AUD now trades at 0.7142, up 0.17% over the past 24 hours and NZD is at 0.6653 (+0.3%).

The euro has also had a good overnight session. The break of previous range high along with momentum from the EU recovery fund agreement helped the euro briefly trade to an overnight high of 1.1601, before easing to 1.1569 where it currently trades. In our latest Global FX strategist publication published on Tuesday we noted that now we see the euro moving into a higher trading range from 1.10-1.15 to 1.12-1.18.

The broad USD weakness has had some exceptions. In G10 JPY -0.33%) has underperformed the USD with USD/JPY now trading at ¥107.18. Moves in USD/JPY remain dominated by equities direction and calmness in 10y UST yields. The other notable underperformer has been CNH, after making another excursion below 7, the increase in US-China tensions see USD/CNH back above the mark at 7.016.

The rebound in US equities has helped 10y UST yields head back towards 0.60% and the UST curve has ended the day with a mild flattening bias. Front end yields a little bit higher while longer dated yields are little bit lower. Of note Italian BTPS are still enjoying the EU funding news with the 10y tenor down another 5.7 bps to 1.035%.

Senate Republicans and the White House are struggling to reach a consensus on another stimulus plan but Bloomberg and the WSJ report that there has been some discussion of a short-term extension of unemployment insurance to provide some cover after payments expire at the end of this month. News of a potential extension played into the recovery in US equity sentiment late in the session.

US existing home sales broke a declining trend, jumping more than 20% and with leading indicators pointing to a further increase, while Canadian CPI data were stronger than expected, and ignored by the market.

US hotspots Arizona and Florida showed decreasing growth in infection rates, but California recorded a new daily record of infection. The US has agreed to pay Pfizer and BioNTech nearly $2b to secure 100m doses of their experimental COVID19 vaccine should it be cleared to regulators and the option to acquire an additional 500m doses. The vaccine would be provided to Americans free of charge. So while the US continues to secure doses, the prospect for vaccines to countries in most needs remain uncertain.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.