Total spending grew 0.9% in June.

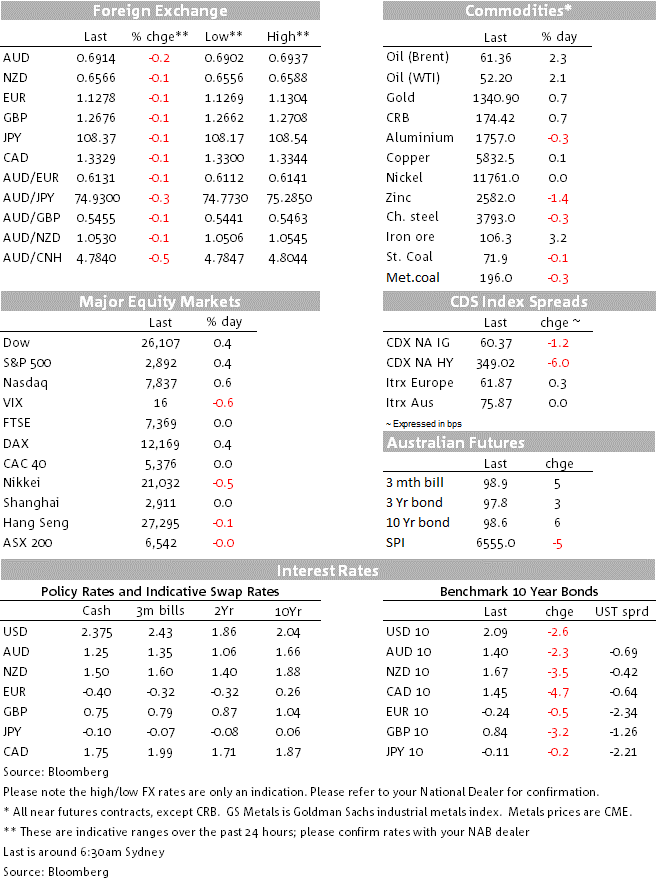

The Aussie dollar was the worst performing of the major currencies overnight following yesterday’s unemployment numbers.

https://soundcloud.com/user-291029717/expectations-of-rate-cuts-rise-unrest-in-the-gulf-grows?in=user-291029717/sets/the-morning-call

Whodunnit (a colloquial elision of “Who [has] done it?” or “Who did it?”) is a complex, plot-driven variety of the detective story in which the puzzle regarding who committed the crime is the main focus

Late yesterday two oil tankers were attacked near the Strait of Hormuz triggering a spike in oil prices while also increasing concerns over a potential escalation in geopolitical tensions between the US and Iran, with the former blaming the latter over the incident. US and European equities ended the day modestly higher, notwithstanding the increase in geopolitical tensions.Fed hike expectations continued to build on little new news, steeping the UST curve. The USD is little changed with AUD the underperformer following yesterday’s lacklustre labour market report.

News that two oil tankers had been attacked off the coast of Iran triggered an initial 4% spike in oil prices ( Brent oil closed 2.32% higher) . The news has also reignited fears of oil supply disruptions given that around 40% of seaborne crude oil is shipped through the Strait of Hormuz. Later in the session Secretary of State Mike Pompeo said that based on “intelligence, the weapons used, the level of expertise needed to execute the operation, recent similar Iranian attacks on shipping”, Iran had to be the culprit. Meanwhile Iran denied the accusations adding that “All countries in the region should be careful not to fall in the trap of those who benefit from regional insecurity.

The ease in oil prices later in the session appears to have been driven by the perception that there is nothing to see here with a similar tanker war in the 1980’s subsiding following the US decision to escort foreign tankers. Some commentators, however, have warned that this conclusion may be too simplistic with the WSJ noting that today Iran has the ability to create some damage via with conventional and cyber-attacks while the US pressures to limit Iran’s ability to export oil may also suggest Iran may not have a lot to lose by escalating tensions in the Gulf of Oman. As we go to print the Us has said that the introduction of tanker escorts is a consideration while a military response has not been ruled out.

Given this backdrop alongside ongoing US-China trade tensions where the latest news has provided further fuel to the notion that the trade war is not only likely here to stay, but also potentially intensify even further, it is somewhat surprising that the US equity market closed the day in positive territory, ending a two day losing streak.

Yesterday, according to a CNBC report the White House Office of Management and Budget told the US Congress it will now meet a two-year deadline to ban federal contracts with companies that do business with Chinese telecom giant Huawei, meanwhile the Chinese Ministry of Commerce said that China would “fight to the end” if the US escalated the conflict.

So while China and the US look to be gearing up for the long haul, the buoyancy in equity markets appears to be driven by expectations of Fed easing coming to the rescue. Market expectations of Fed cuts have continued to gradually build, with a July cut now almost fully-priced and 68bps priced-in by the end of the year.

The UST curve has bull steepened over the past 24 hours with the 2y tenor down 4.5bps to 1.835% while the 10y rate is down 2.6bps to 2.0945%. Nick Smyth, our BNZ strategist, noted today that the sharp rise in oil prices hasn’t done much for market inflation expectations, with the US 10 year breakeven inflation rate falling 1bp to 1.69%, its lowest level since the start of January. While breakeven inflation reflects liquidity premia and other factors, in addition to pure inflation expectations, at face value, market pricing is consistent with PCE inflation (the Fed’s favoured measure) averaging around 1.5% over the next 10 years (breakeven inflation references CPI, which tends to be higher than PCE).

Looking at currency land, the USD is little changed in index terms with DXY (+0.03%) still hovering above 97 while moves in EM FX have also been pretty subdued ( EMCI index -0.04%). CHF has been the outperformer in G10 followed by JPY with both benefiting from a mild safe haven bid meanwhile the AUD has been the laggard following yesterday’s lacklustre labour market report.

AUD now trades at 0.6915, down 0.17% over the past 24hrs and largely reflecting a softer trading tone after yesterday’s labour market report that revealed 42.3k jobs vs 16K consensus (40k NAB), with 2.4k full time, 39.8k part time. Focus was on the jobless rate unchanged at 5.2% vs 5.1% expected. The rise in the participation rate by 2 tenths to a new all-time high of 66% was seen as the main culprit for the unchanged outcome. Bearing in mind the RBA’s desirability of a lower unemployment rate as per RBA Ellis speech on Wednesday night (which confirmed the Bank estimates of NAIRU at 4.5%), the unchanged unemployment rate of 5.2% unsurprisingly has encouraged the market to increase the probability of a rate cut in July. At one point yesterday expectation for a July rate cut climbed to 78%, overnight these expectations ease a bit down to 63% following an article from RBA-watcher Terry McCrann overnight that mentions a second rate cut is now certain, but not yet.

CHF initially underperformed at the start of the overnight session on the back of the SNB decision to keep its policy setting unchanged. The Bank yet again pledged to intervene in FX markets should the CHF rise. The SNB noted global economic risk are more pronounced than at our previous monetary policy assessment and the franc is “somewhat stronger” and thereby “highly valued”. The SNB kept policy rates unchanged at -0.75%, shifting away from its 3M Libor Target Range to a new ‘SNB Policy Rate’ as a consequence of Libor not being guaranteed after 2021.

The GBP has been little moved by the results from the first round of voting for the Conservative party leadership, which saw Boris Johnson receive more votes from fellow MPs than the next three candidates combined. Betting markets now have Brexiteer Johnson as an 80% favourite to become the next Prime Minster

Last but not least worth noting that iron prices have climbed yet again (+3.6% to $106.3) outperforming other commodities including oil. Yesterday GS said the physical market remains tight and estimated the number of ships waiting to unload cargoes in China is near a record low. Disruptions at top exporters Brazil and Australia have led to forecasts of a global deficit.

The May activity readings are going to be closely watch by markets in order to assess whether there has been any negative impact on China’s economy from US led trade tensions. At the same time many will be hoping to see a positive impact from the government stimulatory measures, whether or not we see a rebound in retail sales is also likely to be a focus.

US retail sales likely rebounded in May (0.4% exp.) following a disappointing 0.1% read in April, as for consumer sentiment, the preliminary University of Michigan reading for June is expected to have eased to 98 from 100 reflecting a combination of softer economic data, shaky equity markets and heightening trade tensions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.