Coming in for landing in a heavy cross wind

Insight

The RBA meets in Darwin today and is expected to cut interest rates.

https://soundcloud.com/user-291029717/rba-in-darwin-to-add-some-heat-to-the-economy?in=user-291029717/sets/the-morning-call

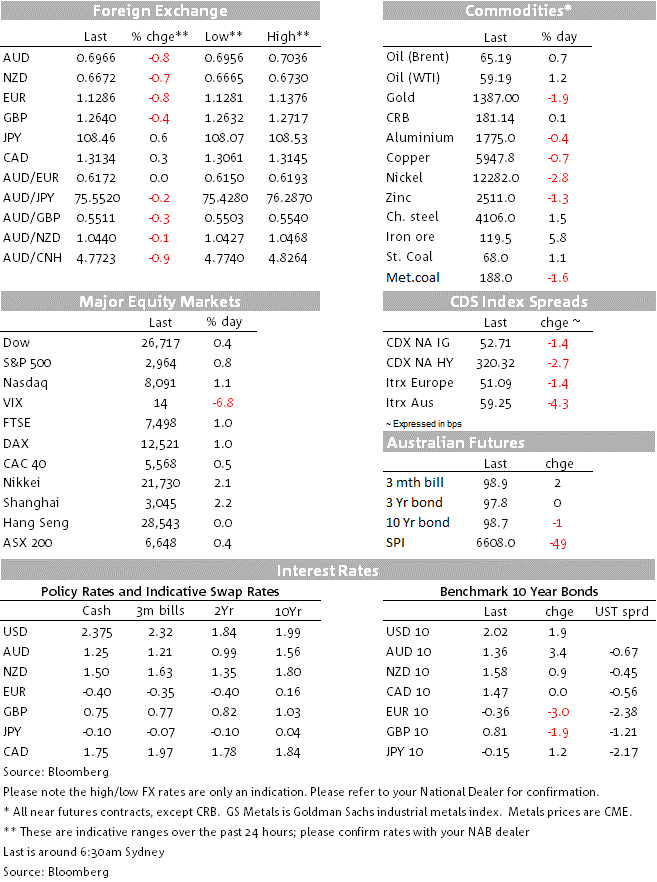

In today’s Morning call Podcast, which you can listen to here, your scribe was lamenting the fact that between March and May this year, US 10 year Treasury yields fell from 2.75% to 2.20% but the US dollar hardly moved; then overnight, US 2 and 10 year yields have each added back a mere 3bps while Eurozone benchmark equivalents have fallen by about the same amount (Bunds -2.8bps) and the US dollar is, in narrow DXY index terms, up by a full 0.75% on Friday’s New York close.

The latter is the reason AUD/USD sits at 0.6966 at the start of Tuesday, down from an early Monday morning high of 0.7036. The NZD has fared similarly, down to 0.6673 from a high of 0.6730. the post-G20 bounce in the antipodean currencies has therefore proved to be very much of the ‘dead cat’ variety, while the juxtaposition of iron ore futures prices, up a heady 5% in Singapore yesterday post G20 – helped too we suspect by the strength in the Construction sub-series of the latest China PMI data – but a falling AUD, plays very much to the point our FX Strategy team makes ad nausea: namely, that the day-to-day correlation between the price of Australia’s biggest commodity export and the currency is practically non-existent and very often negative – in this latest case because of the overwhelming influence of the firmer USD.

Also somewhat curious is that AUD and NZD weakness has come in the face of strength in Emerging Market currencies out of G20, with the offshore CNH the best part of 1% firmer at one point yesterday and an index of global emerging market currencies up nearly 0.2%. Admittedly EM currencies peeled back gains during the offshore session but are still mostly up on Friday night’s close.

US equity markets have closed with gains of just over 1% for the NASDAQ, 0.8% for the S&P 500 and 0.4% for the Dow. Within the S&P, the IT sub-sector is the best performing, +1.45% and within that the semi-conductor sector faring best, up over 2%. This is inevitably linked to the news out of Osaka an Saturday that President Trump was minded to allow US firms to continue supplying components to Huawei, even if this doesn’t resolve the more deep seated national security concerns that are preventing Huawei from being able to participate in the likes of 5G networks in the US and many other parts of the world, including Australia.

All up, no-one seems to be under any illusion that the agreement between President Trumps and Xi in Osaka greatly improves prospect for a comprehensive trade deal being struck anytime soon, but the mere fact that they two sides have agree do restart talks in earnest has provided the pretext for the moves in equities and bond markets. Yet rather than this being a green light for a resumption of US dollar weakness, the FX market has instead gone with the relative moves in bond yields – for today at least.

Overnight economic news has been dominated by PMI data. The US manufacturing ISM was better than expected at 51.7 in June, down from 52.1 in May but better than the 51.0 forecast. The report plays to the notion that the regional Fed surveys for June that were polled early in June when new tariffs on imports from Mexico were feared had a material impact on confidence at the time. That said, among the components, New Orders were down to 50.0 from 52.7, the first time that orders have not grown in 41 months. Employment rose to 54.5 from 53.7.

Tariffs continue to get a lot of airplay in the ISM report. For example, this comment: “Tariffs continue to adversely impact decisions and forecasting. Our increasing fear is that current trends will weaken the global economy, influencing our ability to grow in 2020 and beyond.” (A comment from the Fabricated Metal Products sector.) And this: “Tariffs are causing an increase in cost of goods, meaning U.S. consumers are paying more for products.” (Chemical Products). Not all comments were so worrisome: ”Global demand remains very strong ….. but in the same breath mentioned adaption in their supply chains: “[We] shifted shipments to China from our U.S. plants to our Canadian and European plants because of tariffs.” (Food, Beverage & Tobacco Products)”. Also released Monday, US construction spending for May down -0.8%, but after upwardly revised 0.4% in April for this very volatile and often-revised series. In the aftermath of these two reports, the Atlanta Fed’s GDPNow has been left unrevised at 1.5%.

Eurozone PMI data was mostly revised down slightly from the ‘flash’ releases earlier in the month, e.g. German manufacturing to 45.0 from 45.4, and pan Eurozone manufacturing to 47.8 from 47.6. Also notable was the weakness evident in almost all Eurozone economies outside Germany and France, notably Spain, the Netherlands, Italy and Ireland.

UK manufacturers had a poorer June too: The UK Manufacturing PMI fell to its lowest level since Feb 2013 at 48 from prior 49.4. Markit said this once again reflected the stockpiling build-up and then run down around the 29 March original Brexit date. The sub-50 reading is the second month in a row – also first time this has happened since 2013. New business intakes fell to the greatest extent in almost seven years, weakness in both domestic and foreign demand, with specific mentions of US, Europe, and Australia. Business optimism dipped to its third lowest in history, though there was a rise in optimism that things will be better in one year’s time.

RBA (2:30pm AEST). NAB expects the RBA to cut the cash rate 25bp to 1% today, with a follow up cut in November to 0.75%. In our view, RBA Governor Lowe’s recent communication clearly points to an RBA rate cut in July. In Lowe’s words, during Q&A on Thursday: “I’ve been pretty clear that you could expect, there’s a high probability that interest rates will be cut again, whether that occurs in our historic meeting in Darwin [in July], or at a meeting back in Martin Place [in August].”

As such, the market consensus and NAB expect a 25bp cash rate cut on Tuesday, with markets pricing a 75% chance of a cut. If the RBA doesn’t cut the cash rate in July, we would expect it to cut to 1% in August. Governor Lowe has made it clear that the cash rate will likely be 1% by August and we will take him on his word.

Governor Lowe will likely use his post-meeting speech in Darwin this evening (19:30 AEST) to reiterate that the RBA is easing because “we can do better”, not because the economy is deteriorating. In our view, the RBA’s outlook for growth is too optimistic – activity has halved in the past three quarters and, unlike the RBA, we don’t expect a sharp rebound. The headwinds of weak consumer spending and a slowdown in residential construction are likely to persist into 2020. Further, although we expect some additional fiscal stimulus late this year, we don’t expect a rapid boost to the economy.

NY Fed President John Williams speaks tonight on the Global Economic and Policy outlook (20:35 AEST)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.