Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Central bankers and finance ministers are hooking-up on a conference call later today to discuss a coordinated response to the impact of the coronavirus.

https://soundcloud.com/user-291029717/rba-ready-to-cut-g7-phone-hook-up-helps-markets?in=user-291029717/sets/the-morning-call

Free money, free money, free money, free money, free money, free money, free money, free money, free money, free – Patti Smith

An impending round of fresh central bank easing is not going to make COVID-19 go away; indeed the more draconian and successful efforts at containing the spread of the virus are worldwide, the bigger will be the negative economic consequences. But this thought is playing second fiddle so far this week to the prospect of yet more central bank largesse. This began yesterday with the Bank of Japan and should be quickly followed by 25-point cut to the Cash Rate from the RBA at 2:30pm ET today. As my colleague Rodrigo calculates, when money markets have priced a rate cut with the degree of confidence they currently do, the RBA has delivered some 94% of the time.

We’ve had confirmation of a G7 central bankers’ conference call to take place at 12:00 GMT (11:00 pm ET tonight). This means the Fed, Bank of Canada, ECB, Bank of England and Bank of Japan, though maybe Messrs Lowe and Orr also got an invite?. The Bank of Canada meets tomorrow so should be next cab off the rank after the RBA. Unless, that is, the Fed beats them to the punch with an emergency or intermeeting rate cut, something Treasury Secretary Steve Mnuchin and President Trump’s chief economic adviser Larry Kudlow have just called for, doubtless at the behest of POTUS, who tweeted earlier in the night:

“As usual, Jay Powell and the Federal Reserve are slow to act. Germany and others are pumping money into their economies. Other Central Banks are much more aggressive. The U.S. should have, for all of the right reasons, the lowest Rate. We don’t, putting us at a competitive disadvantage. We should be leading, not following!” We’d rather think the Fed will wait until march 18 then cut by 50, than deliver an intermeeting cut of say 25bps and then another at mid-month, if for no other reason than not being seen to be pandered to political pressure”.

The rally across global equity markets, that sees the US market come into the last hour of NYSE trade with gains of between 1.9% and 2.8% for the main indices, began in our time yesterday after the Bank of Japan followed up its announcement of willingness to provide adequate liquidity support to the financial system with a ¥500bn repo market injection and, on some reports, a step up in its purchase of equity ETFs. Shanghai also had a very good day with obvious suspicions of an invisible hand at work, the Shanghai Composite adding 3.3% (the ASX 200 in contrast was down 0.8%).

Bond markets are continuing on their road of discounting ever lower central bank policy rates and in some cases more balance sheet expansion (first BoJ, then the ECB?). US 10-year Treasuries are down another 9bps to 1.06%. Considering 100bp of Fed rate cuts are now priced by year end, which if delivered would take the mid-point of the Fed’s policy target range to 0.625%, predictions for sub-1% 10-year Treasury yields is hardly ambitious, considering that in Europe, the 10-year Bund yield roughly matches the ECBs -50bp policy Discount Rate.

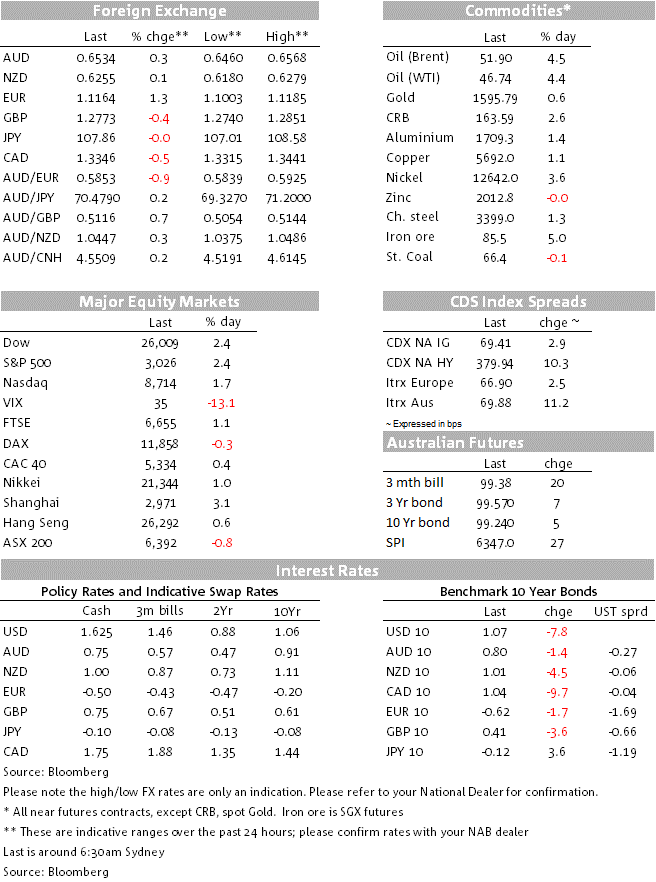

The USD continues to be pressured by, amongst other things, the unwinding of carry trades for which the Euro has been the favoured funding currency of recent year, hence EUR/USD is driving the overall decline in USD indices, in the case of DXY and BBDXY by 0.7% and 0.5% respectively (EUR/USD is currently 1.24% higher at 1.1163 and tops the G10 leader board). AUD more so than NZD look to be drawing support from USD slippage, up 0.28% and 0.11% respectively to 0.6533 and 0.6253. The bird has nevertheless spent a bit of time beneath 0.62 overnight and so below its October 1 prior cycle low

Commodity markets are having a good night, whether its oil, precious or industrial metals. Friday’s weakness in gold, that was attributed to the monetization of long positions to fund loss-making positions elsewhere (or put another way, to bring Value At Risk (VAR) back inside acceptable limits), has not had to feature today, thanks largely to the bounce in global equities.

The US Manufacturing ISM fared a little worse than forecast but remained just above 50 (50.1 from 50.9 and 50.5 expected). New orders fell quite sharply though, to 49.8 from 50.2. The final Markit US manufacturing PMI was 50.7 versus the 50.8 ‘flash’, while the various final Eurozone manufacturing PMIs all deviated very slightly (up or down) from the flash estimates with the pan-Eurozone reading 49.2 up from the 49.1 ‘flash’. Somewhat more significant, US January construction spending rose by a much stronger than expected 2.8% with December revised up to 0.2% from -0.2%. As a result, the Atlanta Fed has lifted its latest Q1 GDPNow estimate to 2.7% from 2.6%.

Ahead of the RBA at 2:30 ET where we expect a 25-point rate cut, we get January Building Approvals and Q4 Balance of Payments, the latter including the net export contribution to GDP. Building approvals are showing tentative signs of stabilisation after holding on to recent gains. We forecast an increase of 2.5% m/m (mkt: 0.5%) led by a small increase in house approvals of 1.5% and a further increase of 4% in apartment approvals. For Net exports, the Q4 GDP contribution is seen by NAB at +0.3% (consensus +0.2%)

Tonight, EZ Feb CPI is seen 1.2% from 1.4% in January and EZ unemployment is expected unchanged at 7.4%.

In the US it’s ‘Super Tuesday’ where 15 states and territories will allot about one third of the total delegates to the Democratic Convention. Results are likely to filter in from Wednesday afternoon Australia time. Overnight, Anne Klobucher is the latest to pull out of the race, in doing so pledging her support to Joe Biden. Partly as a result, Bernie Sanders’ odds of winning the nomination have come down to 49% from an earlier peak of 65%..

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.