NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The markets have reacted firmly to news from the RBA yesterday.

https://soundcloud.com/user-291029717/rba-takes-aim-us-manufacturing-shoots-lower

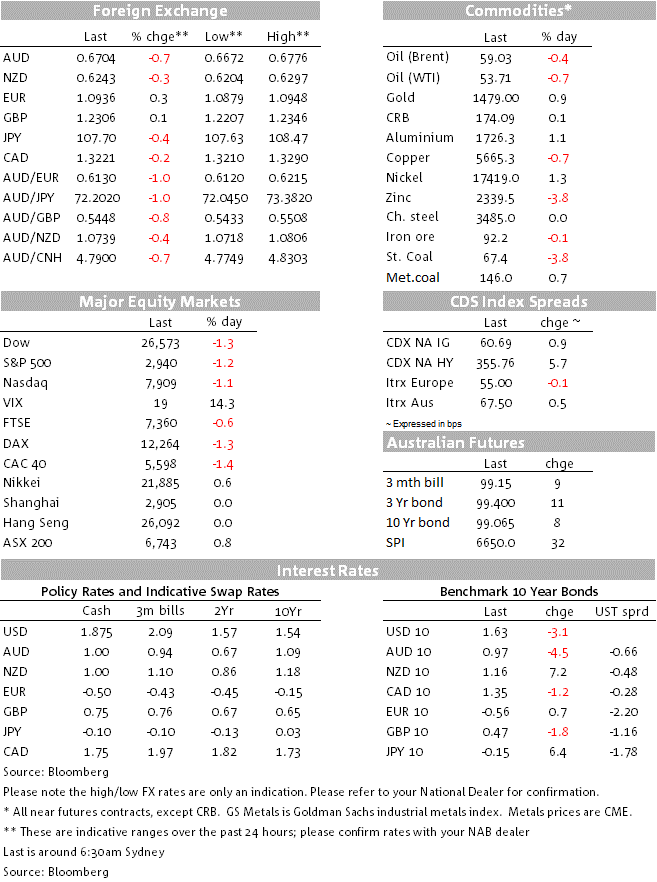

The Blur song of today’s title is actually about the UK shipping forecasts, but let’s not allow the lyrics to get in the way of an apposite headline. Overnight markets have seen the AUD fall to a low of 0.6672, its weakest since March 2009, and the USD in narrow index terms rise to its highest since May 2017, before the USD recoiled and the AUD was pulled up by much weaker than expected US manufacturing ISM (PMI) reading, also the lowest since March 2009. US interest rate markets have undergone a rapid about-face post the ISM report, to see an October 30th follow-up quarter-point Fed rate cut, after the one seen on September 18th, now priced with 77% confidence versus little more than 50% pre-release. US equities didn’t like the ISM messaging despite the potential Fed policy implications, the main board indices all closing with losses in excess of 1%.

Yesterday the RBA cut the Cash Rate by 0.25% to 0.75% as widely expected, but in contrast to the perceived ‘hawkish cut’ by the Fed on September 18th, the post-meeting Statement had more of a ‘dovish cut’ read to it and which quickly stood in the way of any ‘buy the fact’ AUD FX response, unlike that which followed both the June and July RBA moves. Specifically, the last paragraph of the Statement which said the Board will conduct policy to achieve “full employment and the inflation target”, in contrast to “make progress in reducing unemployment and achieve more assured progress towards the inflation target” as appeared in the September (and prior months’ Statements). The impact of this has been to see the ‘terminal’ Cash Rate now priced at 36bps (by November next year) from about 4bps prior to the RBA.

Last night’s speech from RBA Governor Lowe hasn’t offered much by way of additional enlightenment on the likely way forward for the RBA from here, rather it was slanted more toward the justification for Tuesday’s rate cut. . The Governor did highlight downside global risks and structurally lower global interest rates, noting that geopolitical uncertainty has caused firms to hold back on investment. Dr.Lowe reiterated that a global shift in demand for investment and saving has meant the global interest rate had lowered. Here, Lowe noted government was better placed to address these issues, rather than central banks – but that the RBA was nonetheless reacting to these developments, in which respect he stressed that “Monetary policy still works” by way of supporting , “employment, jobs and income growth”. That, in turn, promotes the welfare of the Australian people, the “ultimate goal of monetary policy”, Lowe said.

Local price action post the RBA was quickly usurped by the US Manufacturing ISM report, which showed the headline index drop to 47.8 from 49.1 and against expectations for a rise to 50.0. There was always more than usual uncertainty about this month’s release following very mixed regional PMI readings in the run up, but the release was a shock nonetheless. With the exception of a very minor rise in the overall new orders sub-index (47.3 from 47.2) all the other main sub-readings were lower (production to 47.3 from 49.5, employment to 46.3 from 47.4 and supplier deliveries to 51.1 from 51.4). And while overall orders rose by 0.1%, the separately reported export orders index plunged to 41.0 from an already very weak 43.3. There’s the trade war for you in all its glory as the global economy sinks further towards, albeit still quite far from, recession.

Also out last night was US construction spending which rose by a less than expect 0.1% (market +0.5%). Together with the ISM, this prompts the Atlanta Fed to lower its Q3 GDPNow forecast to 1.8% from 2.1% prior.

Other non-US releases last night included UK manufacturing PMI, which unexpectedly rose to 48.3 from 47.4 but seen reflecting some fresh inventory rebuilding ahead of a potential October 31st no deal Brexit; final Eurozone PMIs which went much changed on the ‘flash’ readings; and Canada monthly GDP for July which came in unchanged against 0.1% expected.

US equity markets didn’t like the ISM messaging, leading the S&P500 to a 1.23% loss, the Dow to a fall of 1.28% and the NASDAQ down 1.1%. Every S&P sub-sector finished in the red, with the largest losses meted out to the financial, industrials, energy and materials, all down by more than 2%. The latter two have suffered despite a somewhat more mixed picture for commodities than yesterday.

Bond markets saw a rapid reversal of the pre-ISM move higher in yields, led by the front end where UST2s dropped from 1.68% to 1.54% to be 8bps lower on the day. 10s fell from 1.72% to 1.635% post-ISM to be 3bps down on 24 hours earlier.

FX saw AUD as by far the weakest G10 currency, clawing back onto a 0.67 handle post ISM from its intra-day low of 0.6672 but still ending NY trade 0.7% down on the day. NZD finished down a lesser 0.3%, hit earlier in the session by the weak QSBO survey. The safe-haven CHF and JPY both benefited from the US equity market sell-off and lower Treasury yields, by 0.4% and 0.3% respectively, while the EUR was also up 0.3% thanks to the post-ISM USD sell-off.

GBP had another volatile night, initially lower before bouncing on a report that the EU was considering offering a time limit on the backstop arrangement in the Withdrawal Agreement. Later, an EU spokesperson said it was “not considering this option at all” and, in any case, such an option would still need to be agreed to by Ireland. The GBP spiked up from around 1.22 to 1.2340 after the initial report hit the headlines before easing back to 1.2293 now. Boris Johnson is expected to produce his detailed plans for a deal with the EU tonight.

Nothing of note on Wednesday’s calendar, US ADP the likely highlight ahead of Friday’s September non-farm payrolls report. Philly Fed President Patrick Harker and NY Fed president John Williams are the two designated Fed speakers.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.