Coming in for landing in a heavy cross wind

Insight

The RBNZ has slashed rates this morning to a quarter percent.

https://soundcloud.com/user-291029717/rbnz-latest-to-cut-in-global-whatever-it-takes-moves?in=user-291029717/sets/the-morning-call

I don’t care if Monday’s blue, Tuesday’s gray and Wednesday too

Thursday I don’t care about you, It’s Friday I’m in love – The Cure

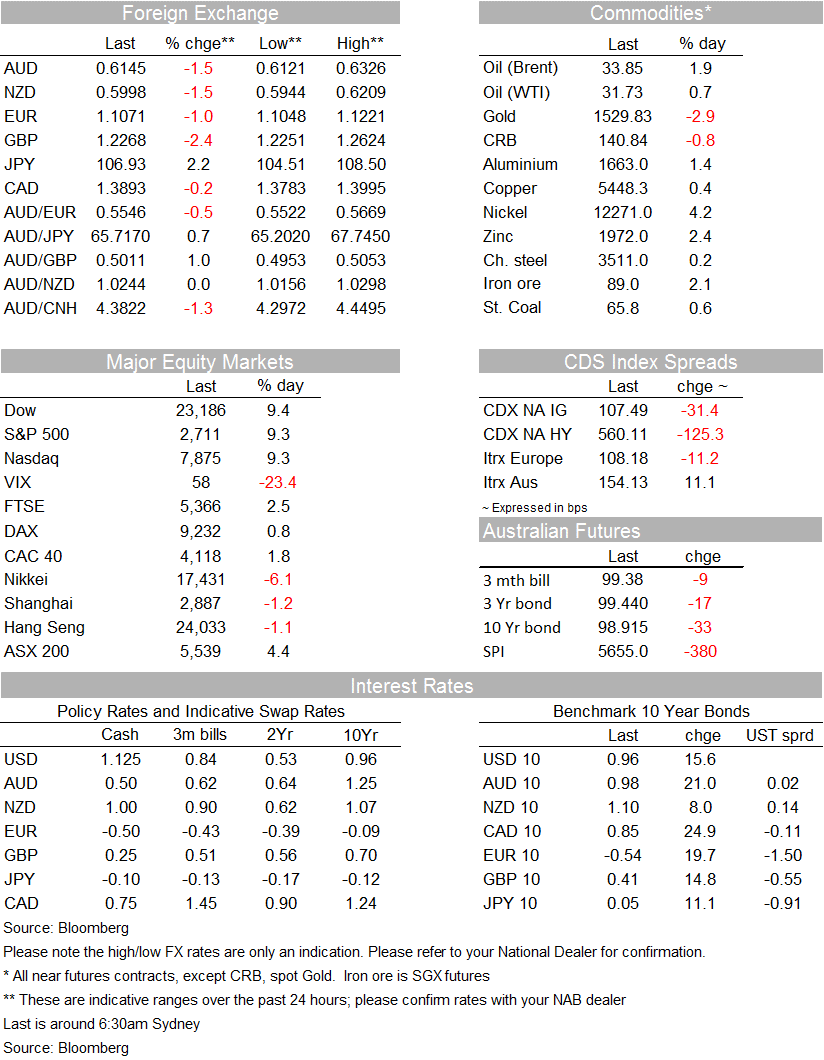

European and US markets enjoyed a positive end to the week with the latter closing with gains over 9%, reversing most of the previous day’s losses. News and then confirmation over the weekend of a US economic relief boosted sentiment, President Trump also declared a National Emergency, freeing emergency funds while Germany’s made a commitment to spend billions. Volatility also remained elevated in the bond market with the 10y note closing the week at 0.96% while the curve bear steepen. Emergency cuts by the BoC and Norges Bank on Friday, have been followed by the RBNZ this morning. The latter has lowered the cash rate by 75bps to 0.25% and suggested next step is QE, not negative rates. The USD was broadly stronger on Friday with JPY and GBP the big underperformers. AUD and NZD ended the week under pressure and now start the week lower, the RBNZ move raises prospect of RBA emergency move too.

The wild moves in markets on Thursday spurred policy makers across the globe into action on Friday. President Trump declared a national emergency, releasing access to $50bn in financial assistance for states, localities and territories. The President also said the Federal government would stop charging interest on student loans indefinitely and promised a relief plan. After intense negotiations, on Saturday, the House passed an economic relief plan backed by President Donald Trump. The package aimed at “combating” the virus includes two weeks of paid sick leave, increased food aid, improved unemployment insurance and more funding for Medicaid. The bill also takes a number of steps to ensure expansive availability of free testing for the virus in the US. Encouragingly, after early signs of an impasse ( voted 363-40) the passing of the Bill shows the ability of Republicans and Democrats to put differences aside to work together. House Democrat leader Pelosi said Congress would now start work on another stimulus package. The WSJ reported that policymakers were looking at a range of “significant” stimulus options.

Early in the session Germany gave strong commitments to increase spending while a European Union executive said the bloc is ready to trigger a crisis clause allowing fiscal stimulus. German Finance Minister Scholz said Germany would deploy a “bazooka” to combat the crisis, saying “we will use it to do whatever it takes”. Scholz said Germany would offer “unlimited” liquidity to affected businesses, facilitated by loans from state bank KfW. Borrowing undertaken by KfW isn’t classed as central government borrowing which means the government can notionally keep to its “black zero” balanced budget policy but still help the economy. Scholz added that the country would consider full-blown fiscal stimulus if the situation got worse. The package, even in its first stage, is bigger than the 500 billion-euro help offered by the German government during the 2008 financial crisis.

European Commission head Ursula von der Leyen said she’s ready to recommend that member states trigger an emergency clause that would allow the whole Euro area bloc to engage in fiscal stimulus if there’s a big downturn. von der Leyen also said that restrictions on providing state aid could be softened, allowing governments to help prop up struggling firms in affected industries. There will be an “extraordinary” G7 leaders’ summit held by videoconference tonight, so we can expect further headlines coming from that.

Central Banks were also in action on Friday with both the BoC and Norges Bank making 50bps emergency rate cuts to 0.75% and 1% respectively. BoC Governor Poloz cited the economic impact of the coronavirus and the fall in oil prices, adding that the Bank would “do what is required” to support the economy and financial system. Meanwhile, ECB Governing Council members were in damage limitation mode, a day after ECB President Lagarde said the ECB was “not here to close spreads” between different sovereign bonds. The comment suggested a reluctance to backstop Italy, which has seen its spreads to German bunds widen sharply since the market turmoil kicked off. ECB Chief Economist Lane said “we stand ready to do more and adjust all of our instruments, if needed” to ensure elevated spreads didn’t disrupt the monetary policy transmission. Bank of Italy Governor Visco implied the ECB could front-load Italian purchases.

This morning the RBNZ has also made an emergency rate cut, lowering the cash rate by 75bps to 0.25%. Importantly as well and in contrast to previous guidance, the RBNZ no doesn’t see the OCR heading below sub zero as the next step, instead “the Committee also agreed that should further stimulus be required, a Large Scale Asset Purchase programme of New Zealand government bonds would be preferable to further OCR reductions”. So now its QE before negative rates. The minutes of the meeting said “Staff also advised that an OCR of 0.25 percent was currently the lower limit, given the operational readiness of the financial system for very low or negative interest rates.” Once the financial system can be geared for negative rates, then theoretically lower rates could be possible, but I’d rule it out for the foreseeable future.

The market is pricing 95bps of rate cuts and after last week’s expansion of the bills purchasing programme along the curve, the market is now looking for a formal announcement of a new QE programme with many speculating on the prospect the Fed will reopen USD swap lines and introduce a Term Asset Back Securities Loan facilities. The bear steeping of the UST curve and appreciation of the USD ( more below) would be a concern for the FED and if the Bank does not deliver a powerful stimulus, the risk is that could end up with higher UST yields and a stronger USD.

In response to a sharp liquidity decline in the US Treasury market, The NY Fed said it would purchase $37b of US Treasury bonds on Friday, almost half its monthly $80b target, in a bid to smooth out what it described as “temporary disruptions.” There have been reports of investors selling government bonds to fund redemptions and as some close out losing making positions. It’s also the case, however, that a 10-year US Treasury yield of 0.5% or below is just not going to provide the same level of portfolio insurance for multi-asset funds looking to hedge the likes of equities.

Equity markets increased over the course of the London session before spiking higher while Trump was speaking, leaving the S&P500 9.3% higher on the day (and almost 12% above the intraday lows implied by futures markets). The recently battered Financials sector led gains (+13%) while Trump’s promise to buy crude oil helped support a 9% recovery in Energy sector stocks. Despite Friday’s rise, the 10th biggest one-day gain recorded on the S&P500, the index was still some 9% lower on the week. The Stoxx 600 Index ended Friday up 1.4%, after earlier rallying as much as 8.8% following Germany’s pledged to spend “billions” to help cushion the blow from the pandemic.

The UST curve bear steepened on Friday with the 10y note climbing 13bps to 0.96% after trading in a range of 0.8211% to 1.0152%. Moves in the 30y part of the curve have also been pretty will, the long bond ended the week at 1.536%, after experiencing 109bp range on the week, comparable to the annual ranges seen over the past 8 years.

The USD was stronger almost across the board. The BBDXY index made a new 3 year high, up more than 1% on the day with CAD and Norwegian krona the outperformers in response to the sharp rise in oil prices (Brent crude +1.9%), even as both central banks surprised markets with emergency rate cuts. . The JPY slumped more than 2.5% amidst the surge in equities and increase in global rates. USD/JPY finished the week just under 108, a far cry from its lows just above 101 on Monday, which had prompted speculation about potential intervention by the Japanese authorities.

The NZD and AUD both fell on Friday amidst broad-based USD strength, but the late-session surge in equities helped both recover somewhat into the market close. The AUD closed the week at its lowest level since late-2008, at around 0.6180 while the NZD was at around 0.6065, its lowest level since 2009. News over the weekend of additional containment measures as well as closures of stores from Apple and other US/global retailers has not helped sentiment at the open ( USDJPY now trades at 106.95) and the RBNZ announcement has put more pressure on both antipodean currencies. NZD now trades sub 60c and the AUD is at 0.6145.

On Friday we published a note highlighting the fact that stock market crashes and global recessions are historically very unkind to the AUD and NZD. So too are lower oil prices. Measures of risk aversion have hit GFC-levels and are currently consistent with much lower levels for AUD and NZD, such that if they are sustained we are almost certainly not done with the downside on both AUD and NZD. We think the AUD is at risk of exceeding its GFC lows of 60 cents while NZD could easily see levels as low as the mid-50s (see the note).

The Central Banks emergency moves seen over the past couple of the days increases the risk of an emergency RBA rate cut. NAB has forecast a follow-up 25bp rate cut to 0.25% in April, but fast-changing events mean the risk of an inter-meeting rate cut by the RBA to 0.25% is likely to have increased sharply. This was not how the RBA behaved during the global financial crisis or even after the 9/11 terrorist attacks, preferring to move at scheduled Board meetings. However, with the next Board meeting still three weeks away on April 7 and the world and Australian economies continuing to rapidly deteriorate, there seems little point in waiting three weeks to deliver further support to the Australian economy on the interest rate front.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.