NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Risk adversity drives yields to record lows in Europe.

https://soundcloud.com/user-291029717/more-rate-cut-talk-except-in-nz-risk-adversity-drives-yields-to-record-lows-in-europe?in=user-291029717/sets/the-morning-call

No light, no light, Tell me what you want me to say.. you want a revelation, You want to get it right – Florence + the Machine

Risk aversion permeated the overnight session with US equities decline deepening following comments from Fed speakers while underwhelming US data releases didn’t help the cause either. European bonds reached new record lows while a non-committal Fed Chair Powell alongside Fed Bullard pushing back on a 50bps cut triggered a short lived spike in UST yields. The USD regained a bit of lost ground mainly against European currencies, AUD is little changed while NZD outperforms ahead of the RBNZ today.

The much awaited Powell speech has the left the market none the wiser in terms of whether or not the Fed will look to embark on a new easing cycle at the end of July. In line with his post FOMC remarks, the Fed Chair said that “many FOMC participants judge that the case for somewhat more accommodative policy has strengthened.” But he added that “…we are also mindful that monetary policy should not overreact to any individual data point or short-term swing in sentiment”.

So while the word “patience” was dropped in the FOMC statement, it seems that Powell is still on a wait and see mode noting that much will depend on the incoming data and specifically the near-term risks (which we take to mean upcoming trade discussions).

Earlier, Fed President Bullard said in a Bloomberg TV interview that by holding rates in June there’s now a high probability of a cut at the July meeting, but he also said that the situation doesn’t call for a 50bps rate cut. He added that “I don’t think we have to take urgent action. This is more in the realm of insurance”. Bullard was a dissenter in June and while he is a known dove, his push back on a 50bps cut in July triggered a spike in UST yields. His comments along with Powell non-committal stance resulted in a pricing recoil for a 50bps cut at the end of July from about 72% to 66%.

That said if the Fed is looking for more data to confirm the apparent deterioration to the economic outlook, then overnight US data releases have certainly added to the case for further easing. Consumer confidence fell by much more than the market expected, with talk of trade and tariff tensions suggested by the Conference Board being the key reason for the fall, against a backdrop of a stronger equity market. New home sales underwhelmed and fell to a 5-month low despite lower mortgage rates. Slightly going against the grain, the regional Richmond Fed manufacturing index didn’t quite fall as much as expected, a contrast to the series of other regional Fed surveys which have been disappointing.

Prior to the opening of the US session, markets were already trading with some caution following comments from Iran saying the path to a diplomatic solution with the US had closed (forever!!) after the Trump administration imposed sanctions against its supreme leader and other top officials. News that President Trump “mused privately” about withdrawing from a longstanding defence treaty with Japan didn’t help sentiment either.

Meanwhile on the US-China trade front, Bloomberg reported that US officials sought to play down expectations for the meeting, “insisting the US wasn’t prepared to compromise on its demands for meaningful Chinese economic reforms”. They also noted that Trump was comfortable that the tariffs he already had in place on $250b in imports from China meant he was in a strong position going into his meeting with Xi. A senior administration official said that the two Presidents may agree to reopen trade talks. But the US won’t accept conditions on tariffs as part of reopening negotiations and no trade deal is expected from the summit.

So amid ongoing US-Iran tension, the equity market appears to be getting increasingly nervous ahead of the Xi-Trump meeting at the end of the week. US equities are lower with the IT sector leading the declines, S&P500 is -0.95% and NASDAQ is -1.51%. At this stage it seems the US is clearly unwilling to accept further conditions on tariffs as part of reopening negotiation and it remains to be seen if the threat of more tariffs will be enough to get China back on the negotiating table. Worth noting too that the Trump-Xi meeting is scheduled to be on Saturday, the final day of the two-day G-20

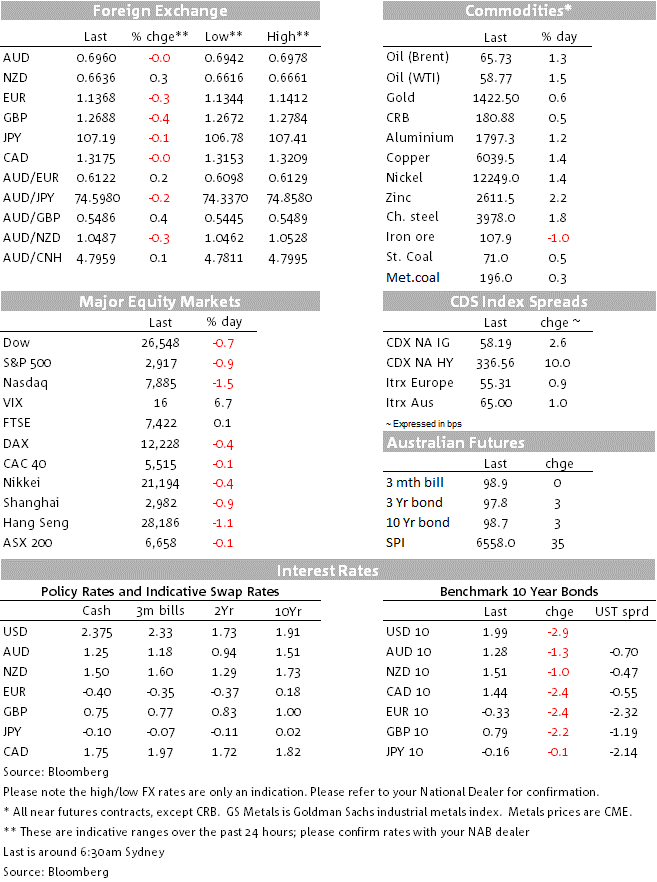

All these news sees global rates lower, with the US 10-year rate down 2bps to 1.99%, while there has been a slight flattening in the curve, with the 2-year rate little changed at 1.73%. Germany’s 10-year bunds fell by 2bps to a new record low of minus 0.33%, with rates across France, Finland, Austria, Belgium, Ireland and Portugal also falling to record lows. Bond funds are enjoying very strong inflows, as investors take the view that interest rates will stay lower for longer, given concerns about the economic outlook.

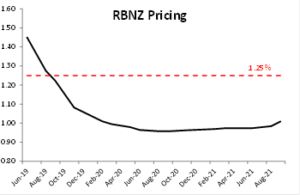

Looking at currencies, the USD has consolidated in index terms with the DXY index settling just above the 96 level. The NZD has been the best performing over the past 24 hours, with much of the gain coming during NZ trading hours. The currency met some resistance near 0.6660 this morning and currently sits at 0.6636. A paring of significant short positions ahead of the RBNZ OCR announcement later this afternoon, might have been in play while the move sub 1.05 on the AUD/NZD cross may have also been another supporting factor.

The AUD is little changed at 0.6961 with Fed induced volatility in the overnight session briefly sending the currency down to an overnight low of 0.6942. Meanwhile, NOK (-0.66%) and GBP (-0.42%) are the underperformers with latter now trading below the 1.27 mark ( now at 1.2689) following weak retail data and Boris Johnson sounding tougher on Brexit during a round of media interviews

RBNZ the focus with market pricing a 20% chance of cut today

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.