Online retail sales growth slowed in May following a fairly strong April

Insight

US equities rose higher still on the back of the latest US retail numbers.

https://soundcloud.com/user-291029717/retail-numbers-push-us-equities-even-higher?in=user-291029717/sets/the-morning-call

There’s some lovely images in The Australian this morning following the rain that fell across swathes of New South Wales yesterday, including the beleaguered South Coast, one in particular of two RFS volunteers in Milton dancing in the puddles. The shift in the Indian Ocean Dipole from extreme positive to neutral that the Bureau of Meteorology has been noting in the past week or so looks to be weaving its magic, bringing cooler and wetter conditions to the north of the country and now travelling south. Go rain.

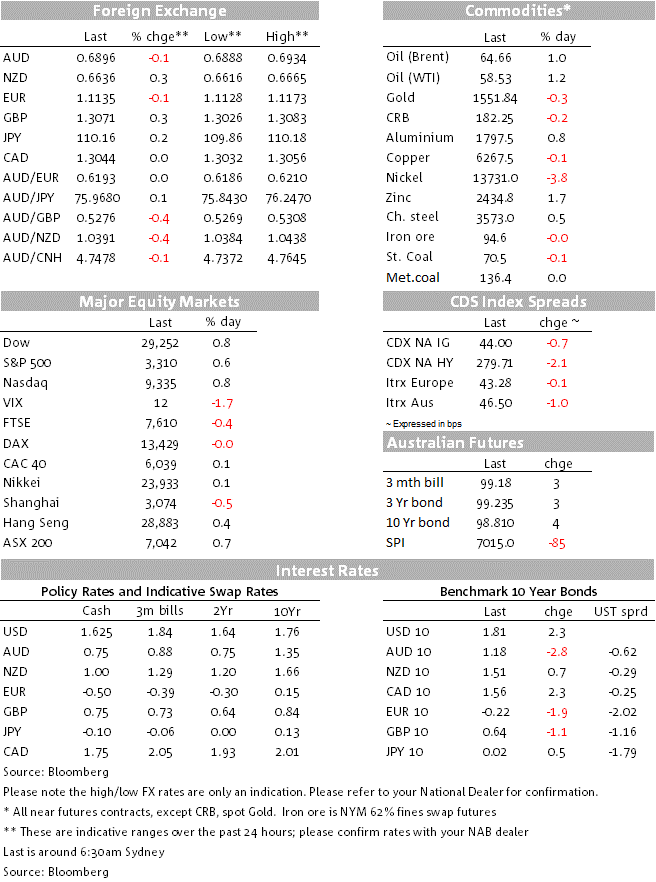

Suffice to say it’s been onwards and upwards for US equites to fresh record highs (hardly needs saying really does it?) accompanied by a fresh nudge higher in US Treasury yields of 1.5-2.5bps and a slightly higher US dollar, up about a tenth of percent and aided by strong headline prints for last night’s economic data but which aren’t nearly so impressive under the hood.

The banner U.S. release last night was December retail sales, which in headline terms rose by 0.3%, in line with consensus, but ex-autos by 0.7%, above the 0.5% consensus and the so-called control measure which feeds into the personal consumption component of GDP, rose by 0.5% against 0.4% expected. The good news ended there, since the October and November control reading were collectively revised down by 0.5%, the significance of which is that the Atlanta Fed has revised down its estimate of Q4 US GDP to 1.8% from 2.3% where it stood after last week’s US employment report.

The Philadelphia Fed index jumped impressively, to 17.0 in January from 2.4 in December, and while the new orders and employment sub-indices both rose, delivery times and inventories both fell. It’s also being the case that the Philadelphia region is less exposed to trade with China, such that the strength in the headline and orders readings should not be seen as a harbinger of strong nationwide (ISM) data when released at the start of February.

Weekly jobless claims have now retraced all of their early December jump to be back at the lowest levels since last November.

Also out last night, soon after we went home, was the December China credit and money supply data, which come in front of today’s Q4 GDP and December activity readings. Here, the most closely watched Aggregative Financing component rose by a much stronger than expected ¥2.1tn. though this is flattered by the inclusion of all types of government bond issuance, not just ‘special’ government bonds – the latter typically used by local governments with the blessing of Beijing to finance stimulus activity/infrastructure spending off-balance sheet. When the prior months’ numbers are adjusted for this, the November comparative statistic is ¥1.9tn, not the originally reported ¥1.75tn. Nevertheless, still a positive change against expectations for a small fall, and a positive indicator for today’s December activity. This after China’s VP Liu He yesterday was out saying growth is projected to be above 6% in 2019 with data indicating a better than expected outlook.

Following the formal signing of the Phase 1 US-China trade agreement yesterday, the Vice Premier revealed that the agreement to increase US purchases by $200bn over two years was to comprise $32bn extra agricultural imports (above 2017 levels), $52.4bn of energy products, $77.7bn in manufactured goods and $37.9bn of services. He claimed that the deal on agriculture will not affect third party’s interests (i.e. wouldn’t come at the expense of reduced imports from other parts of the world) but did not explicitly say the same about these other three sectors. So there is already chatter that in order to meet their commitments, China could scale back some imports of manufactured goods and energy products from elsewhere. Paranoia perhaps, but something to keep in mind vis-a-via Australia and New Zealand.

US equities come into the last hour of NYSE trade with the S&P up 0.6% and the Dow and NASDAQ both +0.7%. All S&P sectors are in the green, including a 0.6% gain for financials and where Morgan Stanley jumped some 8% at the open after reporting better than expected earnings, led in particular by stronger bond trading revenue.

It’s quite a mixed picture, where the NZD and GBP are both showing gains of about 0.25%, the NZD boosted by yesterday morning’s ANZ inflation indicator – a good proxy for non-tradeables inflation – which rose 0.8% q/q. Our BNZ colleagues note this is above their and RBNZ estimate of 0.6% q/q. A 0.8% result would see the annual rate lift to 3.3% a fresh decade-high, not great optics compared to prevailing expectations of a slight dip. It was seen to add to the case for no RBNZ easing in sight and indeed whether the RBNZ’s language might shift to adopt a more hawkish tone. Why GBP is stronger is anyone’s guess, having recently been under the pump from weak incoming industrial production and monthly GDP data alongside dovish comments from various BoE officials.

Other G10 currencies are down by between 0.1% and 0.3%, with AUD/USD 0.1% lower on Wednesday’s New York close at 0.6895, so giving back the gains we saw during our session yesterday and where the Aussie arguably drew a little support from a firmer CNY and better than expected domestic Home Loans data.

China GDP and December activity data at 13:00 ET. Consensus is 6.0% for the YTD y/y figure and 6.0% for the straight y/y number. Risk is to the upside following VP Premier Liu’s comments noted above. Ditto for the monthly activity numbers after last night’s credit and money supply data. All of them are expected to show virtually unchanged annual growth rates versus November, at 5.6% for Industrial Production, 5.2% for Fixed Asset Investment and 8% for Retail Sales.

This evening, the major releases are UK Retail Sales (expected +0.8% m/m ex-auto fuel), final EZ CPI, US Industrial Production (expected -0.2% after 1.1% in November), JOLTS job openings and the preliminary January University of Michigan Consumer Sentiment Index.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.