Online retail sales growth slowed in May following a fairly strong April

Insight

There’s a strong risk off mood in the air, which has pushed the US dollar higher and hit stocks.

https://soundcloud.com/user-291029717/risk-off-mood-as-virus-cases-rise-lowes-dovishness-hits-bond-yields?in=user-291029717/sets/the-morning-call

I need a dollar dollar, a dollar is what I need. Hey hey

Well I need a dollar dollar, a dollar is what I need – Aloe Blacc

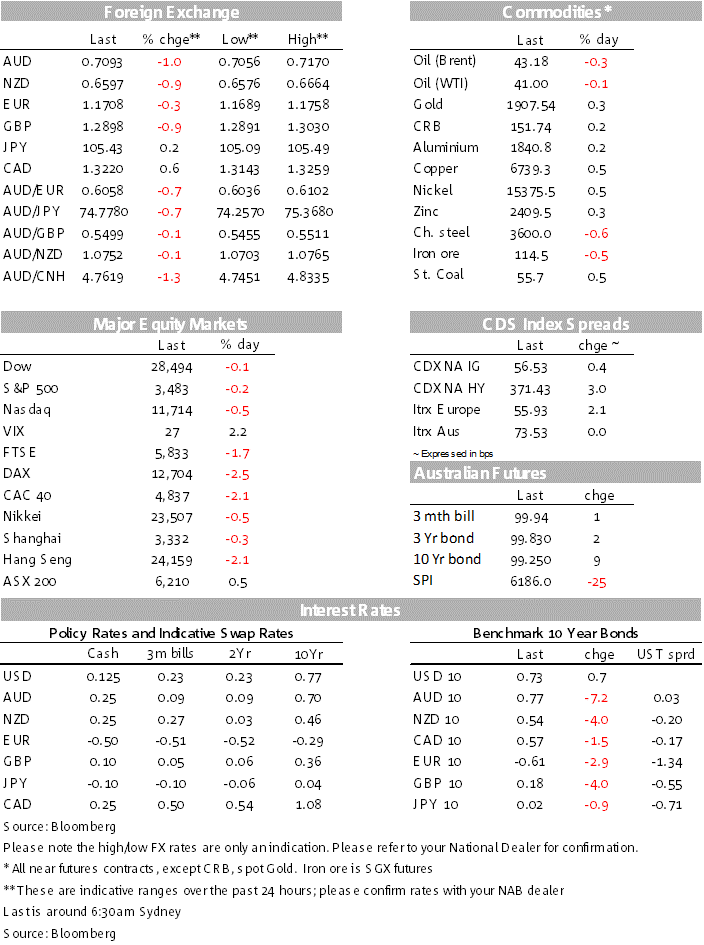

Tougher social restrictions across many European cities have triggered a sharp a decline in European equity indices, US stocks look set to end lower for a third day in a row, although a recovery in financials has triggered a reversal in fortunes late in the session. The extension of risk aversion sees the USD broadly supported with NZD and AUD amongst the biggest underperformers.

US equities fell sharply at the open (S&P 500 down 1.36%) adjusting for the big decline that was underway in Europe.

The acceleration in Covid-19 infections through out European cities has triggered the introduction of tougher restrictions as governments become increasingly concern over the lack of compliance in social distancing rules and prospect of health care services inability to cope with the number of hospitalisations.

Londoners are to be banned from socialising with other households indoors from midnight on Friday evening (effectively closing pubs and restaurants.) in a bid to contain the spread of coronavirus in the capital, this follows yesterday’s news of fresh restrictions in France with nine of the biggest cities including Paris imposing a night time curfew for residents from Saturday.

Meanwhile Germany looks to be heading in the same direction with German Chancellor Angela Merkel imploring citizens to abide by distancing rules and avoid groups if stricter lock-down measures are to be avoided.

European equity indices fell the most in more than three weeks with the Stoxx Europe 600 Index ending the day at – 2.08%, almost erasing all its gains for October ( now 0.5% month to date). After a sharp decline at the open US stocks have trimmed their early losses with the S&P 500 now down by just 0.15% while the NASDAQ is at 0.47%. Morgan Stanley (+1.1%) has led a financials ( up 0.80%) driven recovery following better than expected EPS and sales figures.

Early this morning the FT reported that the much anticipated Solidarity trial by the World Health Organisation which studied the effects of Remdesivir and three other potential drug regimens on 11,266 hospitalised patients has concluded that Remdesivir has little effect on Covid-19 mortality. The news follows a series of recent disappointing vaccine outcomes with Eli Lilly and Johnson and Johnson pausing their trials amid sickness in volunteers.

Initial jobless claims last week rose to their highest level since August, against expectations for a fall. The data is consistent with the idea that the spread of COVID19 and removal of fiscal stimulus has seen a stalling of the economic recovery and a deteriorating labour market, adding to the chance that October data will show a fall in non-farm payrolls.

The two regional PMIs from Philadelphia and New York released overnight showed contrasting fortunes, indicative of a patchy recovery in the manufacturing sector.

Against a backdrop of restriction news in Europe Germany’s 10-year rate fell for a sixth consecutive day, down 3bps to minus 0.61%, its lowest level since mid-March.

Meanwhile in the US longer dated UST yields are little changed, after declining early in the session, UST yields reversed course as US equities embarked on their steady recovery. 10y UST yields traded to an overnight low of 0.6892%, but now trade at 0.7306%.

US stimulus news may have been a factor playing on the move up in UST yields, House Speaker Nancy Pelosi is scheduled to speak with Treasury Secretary Steven Mnuchin ( US Thursday evening) and overnight President Donald Trump said he was prepared to increase the $1.8trn White House stimulus proposals. That may be the case, but later in the session Senate Majority leader Mitch McConnell ( Republican) has gone on record saying that he won’t support $1.8 trn White House stimulus bill—even if Pelosi and Trump make a deal. This is a three way negotiation process and prospects of an agreement this side of the elections remain pretty low in our view.

The USD is broadly stronger with the risk off mood resulting in a safe haven bid on the greenback. The USD is up about 0.4% in index terms while JPY and CHF, the other two preeminent safe have currencies are 0.1% and 0.3% down on the USD.

Risk sensitive currencies such as the AUD and NZD are the big underperformers, down just under 1%.

The AUD was already on the backfoot after further hints from RBA Governor in a speech yesterday noting the Bank is likely to consider further easing measures at its November 3 meeting. AUD pushed down 30 pips from 0.7040 as Lowe spoke, opening the European session at around 0.7130, then falling further, below 0.71 as risk appetite waned, currently trading around 0.7092, after trading to an overnight low of 0.7056 around midnight. The AUD is now effectively trading close to the lower segment of its wider 0.70-0.74 range that ha been in place since late July.

RBA Governor Lowe noted that the Board was considering the case for additional policy easing, which made more sense now that the worst of the pandemic is over and the economy is opening up. In the Q&A the Lowe reiterated it was possible to cut the cash rate to 0.10% from 0.25% and that the Board was evaluating the case for outright QE in the 5-10 year space.

We expect both of these policy measures to be adopted next month. In reaffirming forward guidance of low rates for a long time, he noted that the Board will not increase the cash rate until actual (not forecast) inflation is sustainably within the 2-3% target range

The pair now trades at 0.6596, after making a low of 0.6576 overnight. Despite the dovish RBA, we still see it nowhere near matching the RBNZ’s substantial QE programme and NZ-Australia short rate spreads can fall when/if the RBNZ takes the OCR negative, so we still think that the recent softeness in the AUD/NZD cross will prove temporary.

EUR and GBP are lower, with lockdown restrictions not helping sentiment either. EUR has traded sub 1.17 overnight while GBP went sub 1.28. Bloomberg reported on sources that suggest the ECB sees little reason to rush into new stimulus this month, despite fresh pandemic-related restrictions, reinforcing the idea that any decision will be deferred to December, following a quarterly update of growth and inflation forecasts. The EU leaders’ summit has begun and after tonight we will know if EU-UK trade talks will continue for another couple of weeks.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.