Total spending grew 0.9% in June.

Scott Morrison’s job retention program helped equities yesterday but doesn’t explain the rise in the US and Europe.

https://soundcloud.com/user-291029717/see-you-on-the-other-side?in=user-291029717/sets/the-morning-call

Those of us searching desperately for some positive news on COVID-19 developments could take a little heart overnight from (i) a slowdown in the reported rate of new infections in Italy, the Netherlands and Portugal; (ii) the accelerating roll out of test kits for the virus in various parts of the world; and (iii) by way of evidence that necessity really is the mother of invention, news that the Mercedes F1 team, in conjunction with engineers at University College London and clinicians at the UCL Hospital have, in under a week, built a device that can deliver oxygen to the lungs without the need for a ventilator. If proven helpful, the device could be produced at the rate of 1,000 per day within one week.

Whether any of this has been behind the modestly better showing by most equity markets overnight is debatable, but it certainly hasn’t hurt. There is also a suggestion that gains – where the S&P500 has ended +3.4% – could be in part related to the some necessary month-end rebalancing, whereby balanced funds now underweight equities versus fixed income given this month’s valuation destruction, need to buy stocks to get back into balance. If so, there might be more where that came from in the next 24 hours or so.

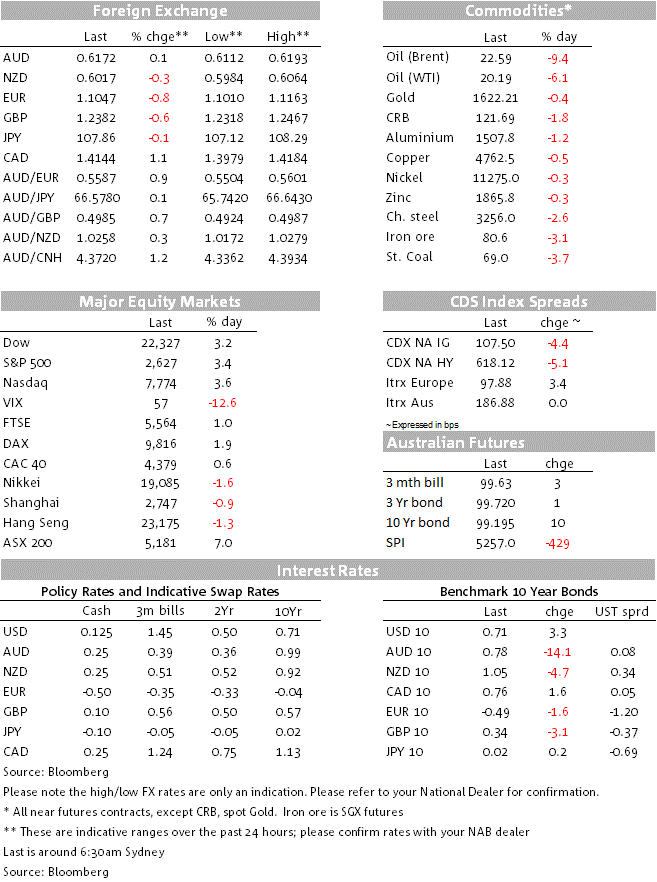

Australian equities outperformed the rest of the world and by some margin (I can’t recall ever writing that before). A good chunk of the 7% gains for the ASX 2000 came late in the day as details of the third fiscal support package from the Morrison government in as many weeks were unveiled, dubbed the ‘hibernation’ strategy. The plan to offer wage subsidies of $1,500 per fortnight for firms suffering a 30% loss of turnover or more (50% for those with turnover in excess of $1bn) as the centrepiece of a $130bn plan, equivalent to 6.5% and bringing total fiscal support announced to date to some 10% of GDP, was simply too impressive to be ignored.

The US dollar is bid once more, the DXY index up by just under 1% led by weakness in the SEK (-1.3%) CAD (-1.2%) EUR (-0.9%) and CHF (-0.8%). AUD/USD is currently down just 0.1% on Monday’s New York close at 0.6166. That the USD is up on a day when risk sentiment was at least slightly improved hints at more hedge adjustments by international fund managers who have found themselves over hedged on their US equity holdings given this month’s sharp fall in valuations – albeit the month-to-date fall in the S&P had now been reduced to ‘just’ 11.0). This may be so, though given the late-month rebound in US stocks, we also expect some fund managers to be selling back some USD they bought earlier in the month at the depths of the US equity sell-off. In Australia, we are not convinced that today’s 4pm London WM Fix will see an excess supply of AUD, in which resect we’d note that AUD/USD firmed during Friday’s and now Monday’s 4pm fixes.

There has been no respite for the relentless downward pressure on oil prices, on a day when the previous OPEC+ production cut agreement is due to expire. WTI crude has fallen from $22 at last Friday’s close to as low as $19.27 ($20 now) and Brent Crude as low as $21.65 from $25 last Friday. Base metals are also lower, the LMEX index down 0.5%.

Incoming economic data continues to warrant little more than a glance, but includes the Dallas Fed manufacturing survey falling to -70 from 1.2 so exceeding its -60 GFC low, and the EC’s Economic Confidence reading falling to 94.5 from 103.4. On the monetary policy front, China yesterday lowered its 7-day repo rate by 20bps to 2.2%, a likely harbinger of cuts to official policy lending rates in coming days.

There’s very heavy data calendar Tuesday, much of which is for February or final Q4 numbers, so irrelevant (including RBA credit numbers which would have aroused a bit of interest pre pandemic). Those with some value include:

NZ ANZ Business Confidence and Own Activity Outlook (11:00 AEDT)

China official March PMIs (12:00 AEDT). These should bounce strongly with large upside risks given the way a PMI is constructed as a net balance of expansion/contraction (the actual magnitude of any such expansion or contraction is not measured). Thus assuming the majority of firms restarted operations, that would be counted as an expansion relative to last month. The consensus is 44.8 for Manufacturing (from 35.7) and 42.0 for non-manufacturing (from 29.6) but we wouldn’t be surprised by much stronger readings than this, but don’t be fooled by what that would mean.

March Chicago PMI ahead of Wednesday’s manufacturing ISM. 40 is the consensus vs. 49.0 in February.

US Conference Board Consumer Confidence, expected to have fallen to 110 from 130.7.

UK March GfK Consumer Confidence and Lloyds Bank business barometer

Other data which is for March include German unemployment (expected 5.1% from 5.0) and preliminary Eurozone CPI (seen at 0.8% from 1.2% for headline, 1.1% from 1.2% for core).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.