Online retail sales growth slowed in May following a fairly strong April

Insight

The extent of the spread of the coronavirus in South Korea, Europe and numerous other countries, has driven a major fallout in markets overnight.

https://soundcloud.com/user-291029717/sharp-moves-as-covid-19-concern-reaches-fever-pitch?in=user-291029717/sets/the-morning-call

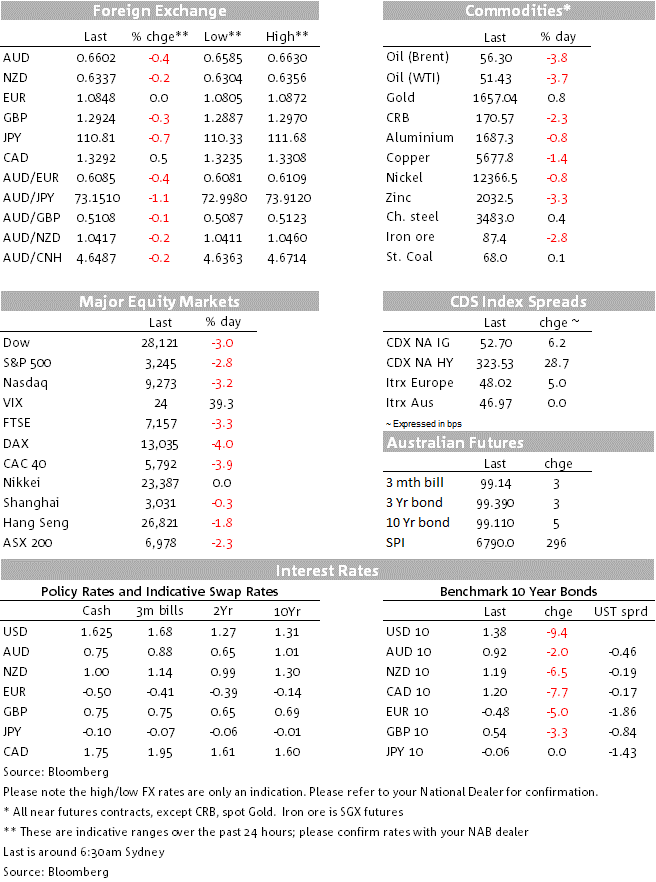

In moves comparable with early August 2019 immediately after President Trump announced that he was lifting the tariff rates on China imports and widening the range of imports to be subject to tariffs, US and European equity markets have had a torrid night. European equity markets suffered losses of plus or minus 4% on Monday, including for the Eurostoxx 50 and German DAX

In the vein of ‘the bigger they are the harder they fall’ the NASDAQ has led the way down for US stocks, currently down just over 3% having been down closer to 4% earlier in the day. From its 19 February high to overnight low, the NASDAQ has fallen some 6.6% over three days; in early August, it fell by over 7% over the same three day time-frame. It then took until the end of October to fully recoup the losses.

As our BNZ colleagues noted earlier this morning, confirmed cases of COVID-19 now extend to some 30 countries, with the total approaching 80,000 and the worldwide death toll over 2,600. Italy reported more than 200 cases, with 7 deaths, while the number of deaths rose to 12 in Iran. Afghanistan, Bahrain and Kuwait reported their first cases. The head of the World Health Organisation still says the outbreak is not a global pandemic – defined by an uncontrollable geographical spread – but the increase in the number of cases in Italy, Iran and South Korea is “deeply concerning”. He noted that while the number of cases outside China remained relatively small, the WHO was concerned about the number of cases with no clear epidemiological link, such as travel history to China or contact with a confirmed case.

Spoking markets somewhat at the start of the European day yesterday was an announcement from the Wuhan local authority than an earlier announcement that it would let some people leave the city was made without authorisation and has been revoked. This has played to the concerns that factories are still struggling to get production back to pre-outbreak levels because of ongoing staff shortages, evidenced by the likes of traffic congestion in major cities run well below normal level for the time of year, as too pollution level in many cities.

Bond markets have responded in predictable fashion to tumbling stocks and heightening expectations that the economic impact of the viral outbreak will draw a monetary as well as fiscal response by some countries. US 10-year Treasury yields are currently 10bps low at 1.375%, so less than 6bp from their record low of 1.318% in mid-2016 (this during what turned out to be a prolonged Fed pause after the Fed had first lifted the Fed Funds rate target off the 0-0.25% floor in late 2015). US money markets now have a quarter-point rate cut fully priced by June and three rate cuts almost fully priced by the time of the November 2020 FOMC meeting (which, incidentally, starts a day after the 3 November US elections).

That the USD is barely changed on Friday night’s NY close doubtless owes something to the building speculation of Fed rate cuts at a time when few other central banks have any conventional policy bullets left in the chamber. This is not really reflected in anything other than the Japanese Yen however, which has quickly re-discovered its traditional safe-haven attributes as well as the pull from lower Treasury yields, to be over a yen down on where we left it. USD/JPY spent time above ¥112 on Thursday and Friday last week and on Monday time below ¥110.5. It’s almost like the good old days of foreign exchange (for an FX Strategist at least). As for AUD, its actually hasn’t done much since dropping from 0.6625 to 0.6600 at Monday’s market re-open, meandering between 0.6587 and 0.6620. Testament perhaps to how much bad news already looks to be priced in at current level.

We had the German IFO which by and large corroborated the message from the flash German PMIs last Friday, i.e. surprising strength or at least resilience, in this case to 96.1 for the headline reading from 96.0 in January and an expected fall to 95.2. It was led – even more surprisingly – by the expectations sub-reading, up to 93.4 from 92.9. We are going need to see March survey day later next month before we can realistically gauge the impact of the spread of the coronavirus outside China and the disruption to intermediate supply chains from the halt to China industrial production only now coming back on line.

In the US the Dallas Fed was the latest of the regional Fed surveys o be released ahead of next week’s ISM reports, and against showed strength inconsistent with last Friday’s Markit flash PMI, rising to 1.2 from -0.2 in January.

Nothing of note locally today, including in NZ.

Offshore this evening in Europe it’s detailed German Q4 GDP (where the headline-only read last week was 0.0%) but does anyone really care about 2019 data? The UK has the Feb CBI distributive sales survey, which may offer a lead on January retail sales

The US has the Conference Board’s Consumer Confidence survey (following a strong University of Michigan preliminary read earlier this month) and the Richmond Fed manufacturing index. The latter will garner more attention than usual in the countdown to the ISM surveys next week and trepidation as to whether they will replicate the sharp drop in the Markit PMIs reported last Friday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.