Total spending grew 0.9% in June.

Yesterday’s retail numbers showed Australians are cutting back on their shopping habits.

https://soundcloud.com/user-291029717/shocking-shopping-statistics-but-rba-likely-to-hold?in=user-291029717/sets/the-morning-call

Phase 1 US-China trade deal optimism continuing to be trotted out as the justification. The S&P 500 is currently up 0.3% at 3,076 half an hour before the close, led by the rise of more than 3% in the energy sector in conjunction with an earlier 2%+ rise in crude oil prices, though oil has given back a good portion of these gains in the last hour or so of New York trade to be only 35-45 cents up on the day.

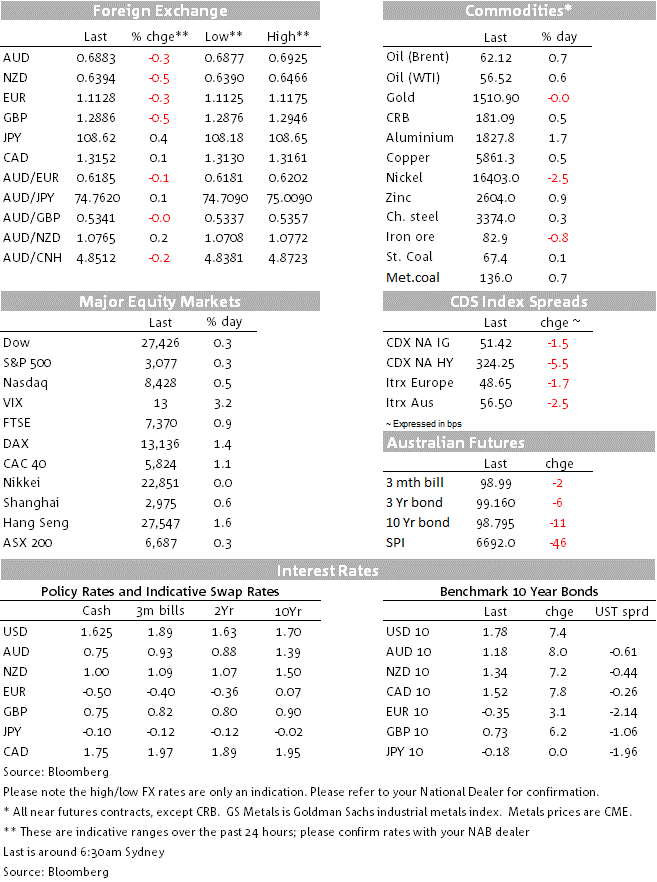

In contrast to the last five business days where positive global risk sentiment has been associated with across-the board US dollar weakness, it has been the opposite overnight with the DXY dollar index up over 0.3%. Losses range from 0.1% for the Canadian dollar through to 0.6% for the Swedish and Norwegian Crowns. Here, we would point to a fresh rise in US Treasury bond yields as a source of support for the dollar, whereas since last week’s FOMC meeting, bond yields have generally been falling alongside positive risk sentiment, to pressure the US dollar on two fronts. USD/JPY has accordingly been lifted in conjunction with higher UST yields, were 10-year Treasuries are currently 7.5bps higher at 1.784%. European bond yields earlier closed 2-5bps higher.

Is that having left here yesterday with plenty of chatter about AUD/USD looking poised to test some pretty significant overhead technical resistance levels, the pair is back down below 0.69 close to where it was before the US dollar started selling off after Fed Chair Jay Powell’s post FOMC press conference last Wednesday in which he made clear that the bar to the Fed resuming lifting policy rates was very high indeed.

Last night, NAB revised its FX forecasts to reflect the view that China and the US would complete this Phase 1 deal in coming weeks, whereupon one of the upshots would be a willingness by China to ensure that the USD/CNY rate not be allowed to rise above its earlier highs just shy of 7.20, more likely then trading in a fairly narrow range just above 7.00 for the most part, unless or until there is agreement to wind back some or all existing US tariffs on Chinese imports. The latter is not something we expect to occur anytime soon. This in turn is now seen limiting the risk that AUD/USD, which has been so highly correlated with the CNY of late, will make new lows this year beneath its early October post-GFC low around 0.6670. The new forecasts see AUD/USD at 0.69 at year end, but not seen breaking sustainably back above 0.70 through H1 2020 at least.

Yesterday, the AUD suffered only temporarily from another poor set of local retail sales figures. Retail volumes fell by 0.1% in Q3, well below market (0.3%) and NAB expectations (+0.2%) and September nominal sales were up by just 0.2% but aided by a solid increase in retail prices. Retail volumes have now recorded falls of 0.1% in three of the past four quarters to be 0.2% lower than a year ago. By way of comparison, the last time volumes fell on an annual basis was the 0.6% decline seen in the early 1990s recession. These data are a worrying sign that overall consumer spending growth was weak in Q3 despite support from the $7.2b of income tax refunds that started flowing from July and the RBA rate cuts in June and July. This suggests that the underlying trend for the consumer may have deteriorated, whereas the RBA expects a gradual improvement to support a “gentle turning point” in the economy. Let’s see what the RBA has to say about this in today’s post-Board meeting Statement, which might flag potential forecast revisions to be included in this coming Friday’s Statement on Monetary Policy.

As for the Statement on the Conduct of Monetary Policy expected to be published later today and about which there has been much speculation since the weekend, Treasurer John Frydenberg has pre-empted the release of the Statement writing an op-ed piece in the AFR, saying there is no change to the inflation target. The Treasurer appears to have blinked on his earlier push to introduce BoE-style accountability measures, saying, “Not changing the statement provides continuity and consistency at this time of global economic uncertainty”.

Incoming ECB President Christine Lagarde has just made her inaugural speech, but doesn’t offer any direct comments on monetary policy thinking.

The RBA’s latest decision at 2:30 AEST is widely expected to be a ‘no change’ as the Board decided to sit out more information on the impact of this year’s 75bps worth of cash rate reductions before deciding what if anything to do next. Assuming so, interest will be any guidance the Statement provides on potential changes to the economic forecast to be published in Friday’s Statement on Monetary Policy.

On the data front, the highlights are the Caixin Services and Composite PMIs at 12:45 AEDT and tonight the Non-Manufacturing ISM, the latter seen up to 53.5 from 52.6. US trade numbers and UK services PMIs also feature.

As for the Melbourne Cup, I know much less about horses than I do about financial markets (a pretty low bar some might say) but skimming the runners and riders on my way in, struggled to look past my namesake Raymond Tusk (albeit, at least until my colleagues walked in the door just now having listened to our daily Podcast (link below) only my mother calls me Raymond).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.