Online retail sales growth slowed in May following a fairly strong April

Insight

The US government shutdown is now in its 25th day but the direction of the global economy is a bigger concern.

https://soundcloud.com/user-291029717/shutdown-slowdown-and-voted-down

Yesterday’s seemingly dire China December trade numbers cast a pall over risk market as well as AUD and NZD during our afternoon Monday and this carried though to offshore market, albeit AUD is back to 0.72 and the sell-off in European and US stock markets has been limited to +/-0.5%. Citi kicked off the US earnings season with better than expected results and meaning is stock is up 4% and financials are bucking the trend of US stock weakness across all other S&P sector. Bond yields are little changed on Friday’s closed.

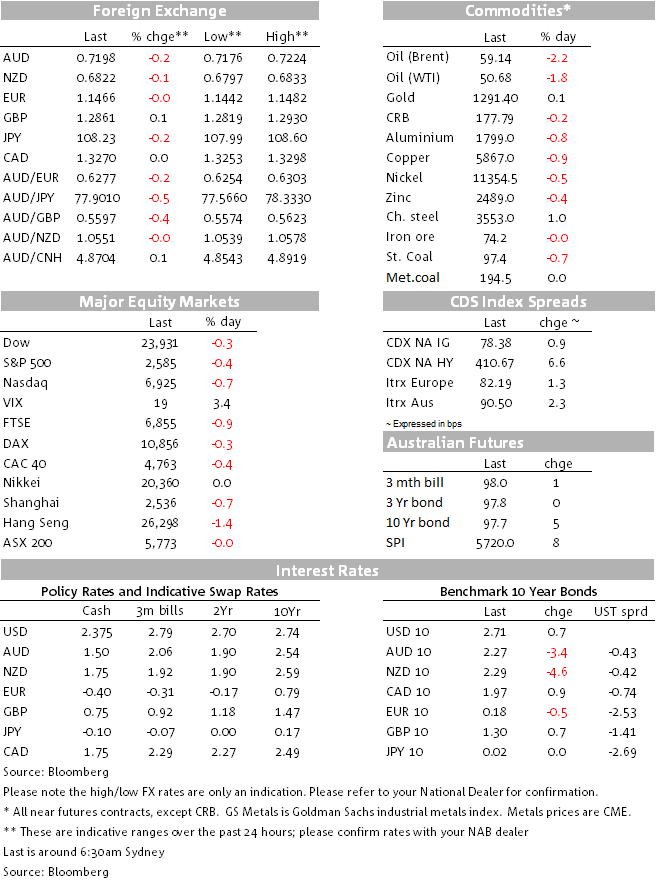

FXAUD and NZD both took a knock upon the release of the December China trade data yesterday showing exports -4.4% y/y against expectations of a +2.0% and imports down -7.6% y/y against +4.5% expected. The former is seen to be symptomatic of weaker global demand that transcends the impact of US tariffs, with weaker exports to the Eurozone as well as the US. Weaker imports meanwhile are viewed as evidence of an even sharper slowdown in China’s economy. If there is silver lining in yesterday’s numbers, it is that they surely further incentivize China to do what’s necessary to strike a reasonably comprehensive trade deal with the US (and where talks resume in Washington on Jan 30th). AUD/USD has recovered to as high of 0.7210 in overnight markets and currently suits around 0.72, about a quarter of a cent up on its post-trade data lows, amid what is a generally flat performance by the big dollar, include EUR/USD, the biggest component of USD indices. The latter is despite another downside surprise in Eurozone data (EZ Industrial production 1.7% vs -1.5% expected ) and warnings that both Germany and Italy may have fallen into technical recessions in Q4 (both countries having recorded negative Q3 GDP readings). Q4 numbers will be revealed at the end of the month. ECB President Draghi speaks tonight in Strasbourg, ostensibly only to deliver the 2017 (yes 2017) ECB annual report, but might choose to say something about recent Eurozone data. GBP has been quite volatile ahead of the parliamentary vote on Theresa May’s deal tonight (time not known) but is currently up about 0.2% on Friday’s close. EC President Juncker and European Council President Tusk sent a letter to Theresa May saying the EU was firmly committed to work speedily on a subsequent trade deal by the end of 2020, so the Irish backstop need not be triggered. But the letter didn’t provide any of the legal reassurances that Brexiteers are clamouring for, so political analysts expect May’s deal will be comprehensively voted down tomorrow. MP Steve Baker, who is part of the Brexit-supporting ERG, said that its group would vote against the deal. Bloomberg reported a survey of FX strategists that forecast GBP could move to 1.34-1.35 in the event of a second referendum or May’s deal passing and as low as 1.22 in the event of a general election (raising the risk of a Jeremy Corbyn government with socialist tendencies). Strategists saw GBP heading to 1.15 in the event of no-deal, although this seems a less likely outcome with parliament stepping up its efforts to take control of the process to prevent such a scenario. EquitiesWith half an hour of US trade to go, the S&P500 is down 0.35% and the NASDAQ -0.65%. moves which followed the risk off tone engendered by the China trade numbers. Financials have held up the S&P where all other sub-indices are in the red. This is after CitiiGroup reported Q4 earnings per share of $1.61 against a street consensus of $1.55, even though its trading revenue suffered during the Q4 market volatility. Both JP Morgan and Wells Fargo report their earnings prior to Tuesday’s market open, BoAML pre-market open on Wednesday and Netflix at the closing bell on Thursday. BondsUS yields are narrowly mixed, with the 2-year Treasury Note currently 0.6bp lower at 2.535% and 10s +0.7bp at 2.708%, so really nothing to see here. Eurozone yields are lower, with 10 year German yields -1bps and some peripheral yields as much as 2.7bps lower (Spain). CommoditiesOil fell by over $1 on Friday and is off about the same again overnight (WTI -90 cents and Brent -$1.30). The message about the (ill?) health of global demand is the obvious fundamental pretext for lower prices. By the same token, base metals are all lower and iron ore flat, though steel rebar futures are up 1%. Gold is up $1. |

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.