Online retail sales growth slowed in May following a fairly strong April

Insight

The fact Trump wasn’t entirely keen on giving up existing tariffs hasn’t stopped investors from pushing equity prices higher.

https://soundcloud.com/user-291029717/trump-wont-rollover-on-rollbacks?in=user-291029717/sets/the-morning-call

10-year Treasuries adding another 2.5bps to 1.94%, bringing the rise for the week to 23bp and up 27bp from the lows seen in the aftermath of the late October FOMC meeting, following which Fed Chair Powell signalled that a resumption of interest rate hikes wasn’t a realistic prospect for a long time given what was happening with inflation.

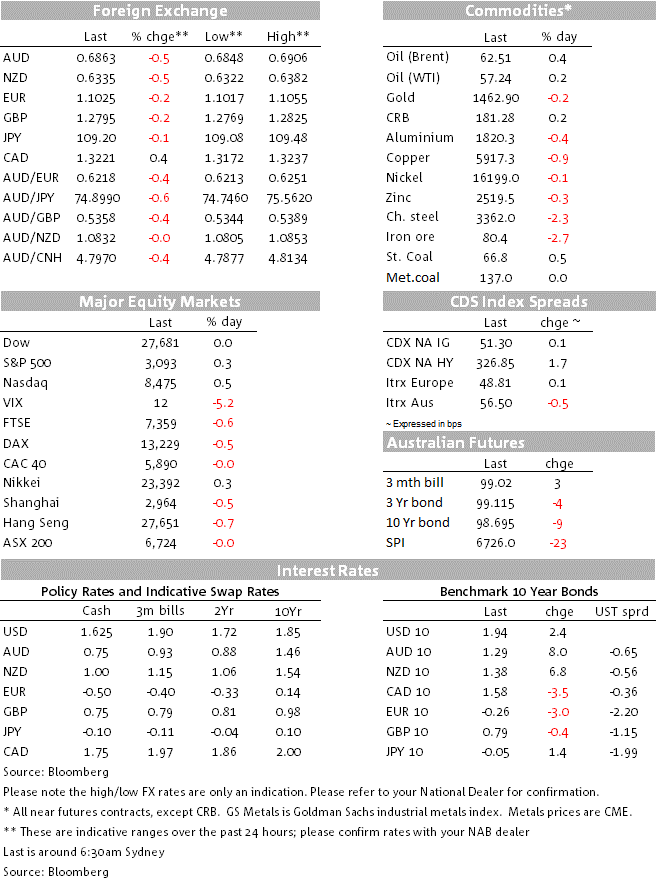

While inevitably dragging up other global benchmarks in its slipstream is nevertheless seeing yield spreads widening out in favour of the US and, we’d suggest, is instrumental in providing fresh support under the US dollar. In the words of the late Robert Palmer, US yields look Simply Irresistible. This is even though risk sentiment, supported by US-China trade optimism and typically associated with a softer dollar, is pulling the other way. So in narrow DXY terms, the USD was up 0.2% of Friday and 1.2% on the week. The latter helps explains why the AUD and NZD were both weaker on Friday (-0.5% and -0.6% respectively) and also on the week. Indeed, the NZD was the worse performing G10 currency last week, down a full 1.5% in front of this week’s RBNZ decision.

Losses have come despite a strengthening in the RMB, both the onshore CNY and offshore CNH back below 7.00 on Friday and over 0.5% stronger on the week, implying somewhat of a decoupling with the antipodean currencies for the first time in many months. This is thanks to the impact of broad based USD appreciation but to which the RMB is displaying immunity. In turn, this reflects ongoing optimism that a Phase 1 China-US trade deal can be struck and which entails at least a partial roll-back of some exiting tariffs. Current focus is on whether President Trump will at least agree to rescind the 15% tariffs imposed on $110bn worth of China imports on September 1st (most of which are consumer goods).

POTUS said “They’d like to have a roll-back. I haven’t agreed to anything. China would like to get somewhat of a rollback [but] not a complete rollback because they know I won’t do it.” Does that mean Trump is potentially amenable to at least a partial roll-back? We’d say yes, but that seeing is believing.

Is that China is genuinely willing to sharply step up its purchases of US pork and soybeans – the primary feedstuff necessary to rebuild its swine herds – almost regardless of it forming an integral part of any Phase 1 trade agreement. On Saturday China’s October CPI was reported at 3.8%, up from 3.0% in September and well above the 3.4% expected. Key to the rise was an acceleration in pork price inflation, now 101.3% yr/yr up from 69% in September.

China Producer Prices shows deepening deflation, led by falling raw material prices, including for ferrous metals. PPI is now -1.6% down from 1.2% in September and beneath the 1.5% expected. The upshot here is that China is back exporting disinflationary pressures to the rest of the world.

Among the countries for whom this will make achieving their domestic inflation targets even harder, is Australia. Friday’s Statement on Monetary Policy (SoMP) shows the RBA giving up on getting underlying CPI above the bottom of its 2-3% target band through the 3-year forecast horizon (its forecast is now 1.9% in 2022). More correctly, the RBA is saying that on current policy settings, it will not hit its target. This should strengthens conviction that the RBA expects to have to undertake further easing down the track, even though the narrative in Friday’s SoMP included comment that “further easing could unintentionally convey an overly negative view of the economic outlook”.

Or rather co-incidentally, the SoMP contain a box showing the results of a simulation on their MARTIN econometric model with the exchange rate (trade-weighted) either 5% higher or 5% lower than the assumed unchanged level that feeds into the baseline SoMP forecasts. Here, if the AUD TWI is 5% lower and stays there, unemployment gets down to 4.5% rather than the 4.9% forecast, and inflation up to 2.25% by 2022 rather than 1.9%. If instead the TWI is 5% stronger, unemployment stays at 5.25% and inflation never gets close to the bottom of the target band. Is it any wonder RBA officials are being so vociferous in expressing their distaste for a stronger AUD?

Putting in a particularly big spurt just in front of the close, seeing the S&P 500 finish 0.3% higher and NASDAQ +0.5% (the Dow in contrast was flat). IT and Healthcare were the biggest gainers by sector.

The main US data point was the preliminary University of Michigan consumer sentiment index, up slightly to 95.7 from 95.5 previously and 95.5 expected, the gain led by expectations (85.9 from 84.2 – driven by trade deal optimism perhaps?) whereas current conditions fell to 110.9 from 1123.2).

Canada’s labour market data showed employment falling by 1.8k against an expected 15.0k rise, but this followed a 53.7k jump in September. More pertinent, the unemployment rate held steady at 5.5% while hourly wages growth picked up to 4.4% from 4.3% last time and against a fall to 4.2% expected.

Moody’s put the sovereign rating on negative watch, citing the plans for whoever forms the next UK government to increase spending. All three agencies have the UK on the second highest rating, so Moody’s is the first to threaten a rating 3 rungs below AAA. Sterling was weaker Friday but largely in line with USD gains across all G10 currencies bar USD/JPY which was flat. The latest UK opinion poll, for the Guardian, shows the Conservatives holding a 12-point lead over Labour, down four points on a week ago.

Known highlights this week include the RBNZ on Wednesday, where 12 of 18 firms in the Bloomberg poll, including BNZ, expect a cut to 0.75% and 6 see no change.

Australia has the NAB Business Survey Tuesday, Consumer Confidence and Wage Price Index Wednesday, Labour market data Thursday and RBA’s Debelle speaking Friday

Internationally, Powell testifies on Thursday, China October activity data also Thursday and of course latest US-China trade developments. The Trump impeachment hearings will re-commence in public views sometime this week. , NZD -0.6%

Today, just UK Q3 GDP and industrial production.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.