Total spending grew 0.9% in June.

Not much movement in currencies or equities.

https://soundcloud.com/user-291029717/slow-day-with-steepening-yields-and-softer-pound?in=user-291029717/sets/the-morning-call

It was remiss of us last week not to have paid homage to Roxette’s Marie Frederickson upon news of her untimely death. We belatedly do so today with one her songs, fitting on a day when the Swedish Riksbank is expected to be the first ever central bank to kick the negative interest rate habit, seen lifting its repo rate from -0.25% to 0.0% (after having moved from -0.5% to -0.25% at the end of 2018). Norway’s Norges Bank also makes its last policy decision of the year, where its Deposit Rate is seen holding at 1.5% (already 75bps up on where it was at the start of the year). The BoJ is sure to keep its policy rate at -0.1% and the Bank of England at 0.75%.

Predictably quiet overnight markets with the known big global event risks for the year behind us (news expected imminently of a vote to impeach the sitting US President for only the fourth time in American history doesn’t qualify in this regard). This isn’t the case here however, with the November labour market report due his morning and which has the potential to move the dial on expectations for whether the RBA will resume cutting the cash rate as early as next February, and with that all things AUD. NZ GDP also this morning is also capable of causing a ripple or two in kiwi markets. See Coming Up below for details on both. AUD and NZD are both unchanged on where they were 24 hours ago but which means they are both a little firmer than where we left them at yesterday’s local closes.

Has been the German December IFO survey, which in contrast to the disappointing PMI readings earlier this week has instead mimicked the earlier ZEW survey and shown evidence that the German economy may be in the process of pulling itself up by its boot straps. The Business Climate index lifted from 95.1 to 96.2 (95.5 expected) and the Current Assessment from 98.8 from 98.0 (98.1 expected). Expectations rose to 93.8 from 92.3 (93.0 expected). The news proved capable of producing only fleeting gains in the Euro (from 1.1126 to 1.1143) before resuming its mild intra-day downturn. Testament it would seem to the lack of anything other than order-driven FX trading in the run up to Christmas, but a positive omen nevertheless for the EUR at the start of the new decade. Improvement in the German – and broader Eurozone – economy – is fundamental to our expectation for a softer US dollar and stronger Euro next year – as per our Global FX Strategist and 2020 Outlook published yesterday afternoon. If you are a NAB Wholesale client and haven’t received this but would like to, let us know by return mail.

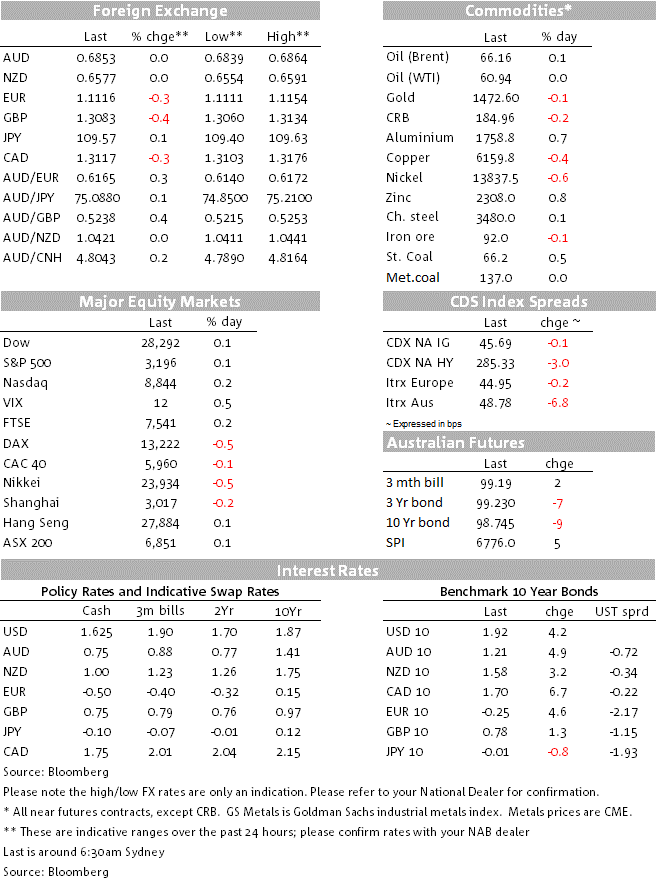

New inflation readings were out last night from Canada and the UK (final Eurozone CPI was confirmed at 1.0% for headline and 1.3% for core). In Canada, the average of the three core measures was a smidge higher than last time at 2.15% from 2.1% and 2.1% expected, with headline up to 2.2% from 1.9% – as expected. This serves to underscore the limited likelihood of the Bank of Canada cutting rate at least though the first half of 2020. In the UK, CPI held at 1.5% rather than fall to 1.4% as had been expected, while the core reading was unchanged at 1.7% in line with consensus. The British pound was weaker again overnight, nothing to do with the data but rather an ongoing drag from Monday night’s news of the Brexit Withdrawal Agreement being altered to hard code a December 31 2020 transition end date. Its again the weakest of the major (G10) currencies, -0.35%, followed by the EUR (-0.3%) and the SEK (also -0.3%, notwithstanding today’s expected Riksbank news).

Seemingly helping keep the USD afloat (DXY +0.18% to 97.4) has been further rise in US bond yields, 10-year Treasuries +4.2bps to 1.92% whereas most equivalent European benchmarks are barely 1bps changed. US equities come into the last hour showing gains of between 0.1% and 0.25%

Fed speak has included NY Fed president John Williams running the now familiar line that “monetary policy is in a good place”. The outlook for policy depended on how economic conditions change, with a “material” change needed to adjust “our” policy view, consistent with the line being run by Fed Chair Powell ever since the last (end October) rate cut. Chicago Fed president Charles Evans has been out ion the last hour saying that policy is ‘at a good setting’ and that he’s comfortable with a projection for no change in rates though 2020 (presumably then that’s where his ‘dot’ lies). He does though say that getting inflation up to 2.5% would reinforce the Fed’s symmetric inflation goal.

Today’s Australian Labour Force Survey is realistically the last piece of domestic economic news capable of moving the currency and rates markets this year. The NAB survey employment index and SEEK job ads suggest that the demand for labour remains weak, such that we continue to expect slower trend growth in employment. Accordingly, NAB expects a moderate bounce of 17k in November after last month’s surprise 19k fall. Alongside moderate employment growth, we expect unemployment to remain unchanged after ticking up to 5.3% last month. Note, our medium-term view remains for a gradual increase in unemployment.

Ditto for the NZ rates and currency market, Q3 GDP is the last major release of the year. BNZ anticipates a 0.5% increase, compared with the RBNZ’s 0.3% forecast (consensus: 0.5%). Note the likelihood of substantial upward revisions to history affecting the last few years, but which might wash out with respect to inflation implications.

We get the Riksbank (+25bp to 0.0% expected) the BoE (seen unchanged at 0.75% but where, recall, 2 MPC members wanted an immediate rate cut last month) and the BoJ (no change at -0.1%). Data highlights include UK retail sales, US Q3 current account, Philly Fed survey, weekly jobless claims and Existing Home Sales.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.