NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There wasn’t much movement in shares, bond yields or currencies overnight, despite weaker retail numbers out of the US.

https://soundcloud.com/user-291029717/slow-movement-soft-data?in=user-291029717/sets/the-morning-call

“Sweet dreams are made of this; Who am I to disagree; I travel the world and the seven seas; Everybody’s looking for something” Eurythmics 1982

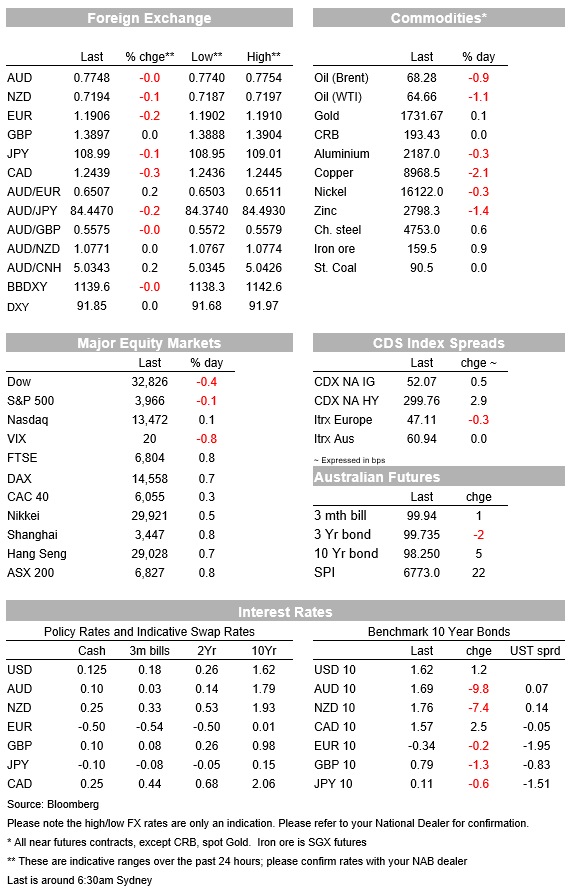

Sweet dreams by the Eurythmics probably sums up overnight price action the best with very quiet trading conditions ahead of the FOMC announcement (5am Thursday Sydney time). Most markets are broadly tracking sideways. The S&P500 is down slightly (-0.1%), while the US 10yr yield has traded in a tight range (1.585-1.63) and is currently up 1.2bps to 1.62%. A US 20yr note auction also drew strong demand, highlighting appetite for bonds at current yields. G10 FX has seen little in the way of significant moves with most pairs +/-0.3% and the USD DXY is flat at 91.87. Quiet trading is likely to persist until the announcement. With positioning largely close to neutral ahead of the FOMC CFTC data, there is the potential for large moves in either direction with Powell needing to walk a fine line of acknowledging the improvement, but also that the Fed isn’t intending on changing its policy guidance despite Treasury Secretary Yellen’s observation the US could be at full employment by mid-2022 (see Coming Up below for details).

Weaker than expected US data has been largely ignored due to the impact of recent storm activity and as it pre-dates the latest stimulus package where payments are hitting the economy. US Retail Sales for Feb fell -3.0% m/m against -0.5% expected with the core control group also weak at -3.5% m/m against -0.6% expected. Prior months were also revised higher with core control for December now +8.7% m/m from the initially reported 6.0%. As for next month, JPMorgan and BofA’s respective trackers of credit-and-debit-card transactions shows a lift in spending in early March even ahead of the stimulus payments.

US Industrial Production was also weaker than expected (-2.2% v. 0.3% expected). Highlighting the impact of the weather, the Fed (who publishes the data) noted “severe winter weather in the south central region of the country in mid-February accounted for the bulk of the declines in output for the month” and excluding he effect of the weather, manufacturing production would have only fallen ½% (see Fed for details ). Finally the NAHB Housing Market completed the trio of weaker than expected prints at 82 from 84.

The vaccination rollout in the EU remains uncertain after at least 16 countries suspended or limited the use of the AstraZeneca vaccine after a few reports of blood clotting. The European Medicines Agency reiterated overnight that the vaccine’s benefits outweighed its risks and on Thursday its Pharmacovigilance Risk Assessment Committee will meet to conclude a detailed investigation into the issue. AstraZeneca themselves note that “ Around 17 million people in the EU and UK have now received our vaccine, and the number of cases of blood clots reported in this group is lower than the hundreds of cases that would be expected among the general population” (see AstraZeneca for details).

Risk markets are largely ignoring the vaccine headlines given the high degree of efficacy seen in the vaccines that have been approved with any potential setback only being about timing, which is still seen as a matter of months rather than quarters. Accordingly European equities have been little impacted with the EuroStoxx50 +0.6% and DAX +0.7%. FX markets though are using it as a justification for Euro underperformance with a slower vaccine rollout likely meaning US outperformance – EUR was -0.2% to around 1.19.

Other FX pairs are little moved. Both the AUD and NZD have tracked sideways ahead of the FOMC. While a 3.8% fall in the GDT dairy auction price might have weighed on NZD on another day, the fall follows the previous 15.0% surge, so the latest auction won’t see any revision in milk price assumptions.

Closer to home, yesterday’s RBA Minutes confirmed the Board having discussed the 3yr YCC target with a decision on whether to maintain the April 2024 bond as the target or shift to the November 2024 bond being made “later in the year”. On deciding whether to extend YCC, the Board will monitor “ the flow of economic data and the outlook for inflation and employment”. Importantly the Board also agreed that “it would not consider removing the [YCC] target completely or changing the target yield of 10bps” and that any exit strategy would involve allowing the target bond to mature (“the maturity of the target would gradually decline until the bond finally matured”).

A key question remains what hurdles for inflation and unemployment the RBA will be looking at in deciding whether to extend the 3yr YCC target, such a decision presumably having to be made by August 2021. Before then we have only a few wage and inflation prints, but no-one is expecting a significant pick-up in the pace of wages or inflation outside of base effects on the y/y calculations. Some hint could be from the Board’s discussion of the end of JobKeeper. The Minutes note: “However, in the near term there was some uncertainty relating to the effect that the end of the JobKeeper program would have on labour market conditions… .[but] The end of the JobKeeper program was seen as unlikely to result in a sustained increase in the unemployment rate”. Note, we are unlikely to see the full impact from the end of JobKeeper on the labour market until mid-May when the April employment data is published.

Weekly Payrolls data yesterday in Australia were also strong, suggesting another strong employment print on Thursday.

Finally in geopolitical news, the Biden Administration has aligned with Australia in its recent tensions with China, with the Biden administration telling China that normalising relations with Australia is a precondition to Washington taking any substantial step towards improving relations with Beijing according to Reuters (see Reuters for details ). Note US Secretary of State Blinken will meet with China’s top diplomat Yang Jiechi and State Councillor Wang Yi on March 18.

A quiet day for Australia with no data scheduled, while an RBA speech on “Small Businesses Finance in the Pandemic” is unlikely to be market moving. Offshore focus will be on the FOMC meeting announcement (5.00am Thursday AEDT) with markets likely quiet ahead of that. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.