Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

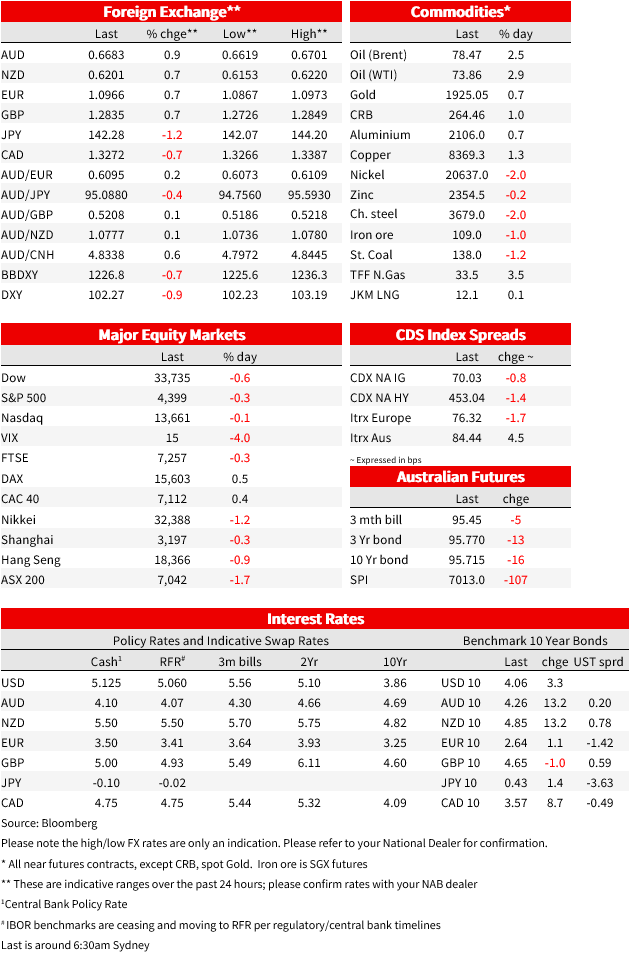

Payrolls failed to deliver the upside surprise feared following strong data earlier in the week, seeing some pullback in the USD and short-end yields on Friday.

GE: Industrial production (m/m%), May: -0.2 vs. 0.0 exp.

US: Nonfarm Payrolls (chg, k), Jun: 209 vs. 225 exp.

US: Unemployment rate (%), Jun: 3.6 vs. 3.6 exp.

US: Average hrly earnings (m/m%), Jun: 0.4 vs. 0.3 exp.

US: Average hrly earnings (y/y%), Jun: 4.4 vs. 4.2 exp.

CA: Unemployment rate (%), Jun: 5.4 vs. 5.3 exp.

Payrolls on Friday failed to deliver on the upside risk feared following Thursday’s very strong ADP print the strong employment intentions in the Services ISM. Headline payrolls came in a little below consensus. US 2yr yields were 4bp lower on Friday, while the US dollar was weaker and US equities closed showing small declines after reversing earlier gains.

Non-farm payrolls rose 209k, a little below consensus for 230k, with downward revisions of 110k over the past two months. That’s suggestive of modest trend slowing in the pace of net hiring, but still robust pace of employment gains. The unemployment rate dipped a tenth to 3.6%, in line with consensus. More concerning from the Fed’s perspective, however, was an apparent reacceleration in wages growth. As the WSJ’s Timiraos writes over the weekend, while shelter and used car should be helpful in pushing down core inflation in the near term, the ‘last mile’ of the inflation fight “could force the Fed to keep monetary policy tight until the labor market weakens.” (See Last Mile of the Inflation Fight Will Be the Hardest). Average earnings per hour rose 0.4% m/m, matching an upwardly revised May to leave the year-ended rate at 4.4% from 4.3%. The average earnings data can be noisy and are subject to revision, but the combination of still healthy payroll gains and concern elevated wage outcomes are far from a compelling case to wrest the Fed from its signalled path for further policy firming.

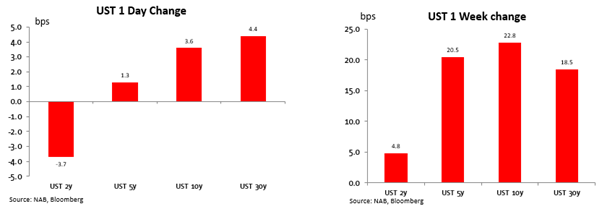

Speaking after the data, Chicago’s Goolsbee pointed to policymakers’ median forecast for two more rate hikes this year and said, “I haven’t seen anything that says that’s wrong.” That said, he was less committal on a hike coming as soon as July, “We have to figure out when, but there are some modest increases to come.” Near term market pricing is little changed, with 89% priced for the July meeting late this month, and 35bp of further tightening priced by November. 2yr yields were 4bp lower over the day to 4.95%, after partially retracing a dip down to an intraday low of 4.86%, and to be well below their intraday high of 5.12% touched on Thursday. Longer dated bonds, however, continued to sell off. The 10yr yields was 4bp higher over the day to 4.06%, some 23bp higher over the week and just 2bp from its intraday high reached on Thursday. Curve steepening has seen the 2s10s spread back inside -90bps.

The bond market selloff over the past week was not just a US phenomenon. German 10yr bunds were 25bp higher to 2.64%, their highest since March, while 10yr Gilts were 26bp higher to end the week at 4.65% after reaching a new post-2008 high of 4.71%. Markets currently price a peak Bank Rate of 6.37%. Markets price an additional 51bp of tightening from the ECB, up 4bp on a week ago. The ECB’s Villeroy, speaking on Sunday, played into the high-for-longer assessment reflected in the selloff in bond markets. Villeroy believes “we will soon reach the high point of interest rates” but warned that rather than a peak, that would mark “a high plateau, on which we will have to remain for a sufficiently long time to fully transmit all the effects of monetary policy. ” ECB President Lagarde on Friday said that policymakers still have work to do and indicated that official were watching to see whether profits were being squeezed alongside growing wages, “a simultaneous increase in both [wages and profits] would fuel inflation risks, and we would not stand idly by in the face of such risks.”

Canadian employment jumped 60k after its May fall, sharply exceeding forecasts for +20k and driven by full-time employment. Despite the jump in employment, the unemployment rate increased to 5.4% from 5.2% amid high population growth and a lift in the participation rate. Market pricing for a BoC hike on Wednesday rose to 67% from 59%.

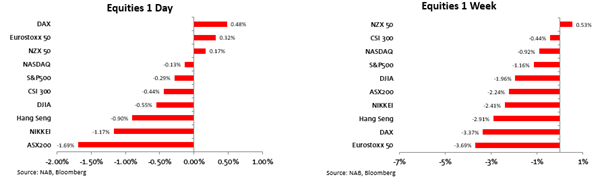

US equities were lower on Friday. The S&P500 lost 0.3% after reversing early gains on Friday to be 1.2% lower over the holiday-shortened week. The Nasdaq was 0.1% lower on Friday and 0.9% lower over the week. Energy stocks gained led gains on Friday, with the S&P500 sector up 2.1% on Friday. European equities fared worse, the Euro Stoxx 50 down 3.7% over the week despite a 0.3% gain on Friday.

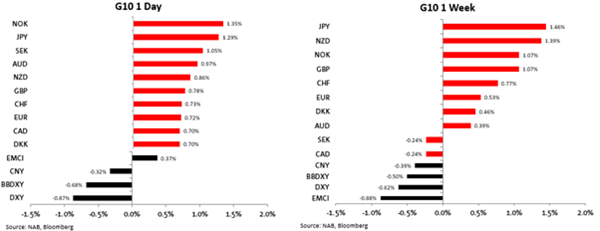

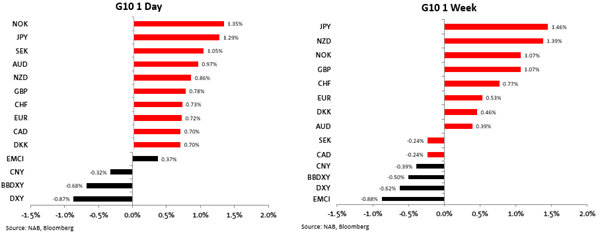

The US Dollar was softer on the DXY following payrolls data, losing 0.9% on Friday. The yen was up 1.3% against the dollar on Friday and 1.5% over the week to see USDJPY ending the week near 142. The dollar was weaker against all G10 currencies on Friday. The euro was 0.7% higher to 1.0966 and 0.5% higher over the week.

The AUD gained 1.0% against the broadly weaker dollar but was towards the bottom end of the G10 leader board over the week, up just 0.4% to end the week around 0.6690. The NZD in contrast, was 1.4% higher. The RBA decision to hold rates steady on Tuesday was one factor behind the relative underperformance, though amid the broader global sell off in bond markets there has been little impact on near-term market pricing, indeed, futures imply a year-end cash rate of 4.69%, up from 4.58% a week ago.

The Peoples Bank of China (PBOC) continued to signal its discomfort with Yuan weakness, setting Friday’s fix stronger-than-expected by the largest margin since November. The fix has been set consistently strong recently. The CNY was 0.3% higher on Friday 0.4% stronger over the week to 7.23.

Oil was also higher on Friday, with Brent up 2.5% to $78.47. That’s its highest since May and takes gains over the week to 4.8%. Saudi Arabia and Russia this week announced extensions of voluntary cuts to exports until the end of August, a signal that Saudi Arabia is committed to prevent prices from falling further. Commodities more broadly were mixed over the week, with key base metals generally seeing small weekly moves.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

Uncertainty remains high ahead of July reciprocal tariffs

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.