Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

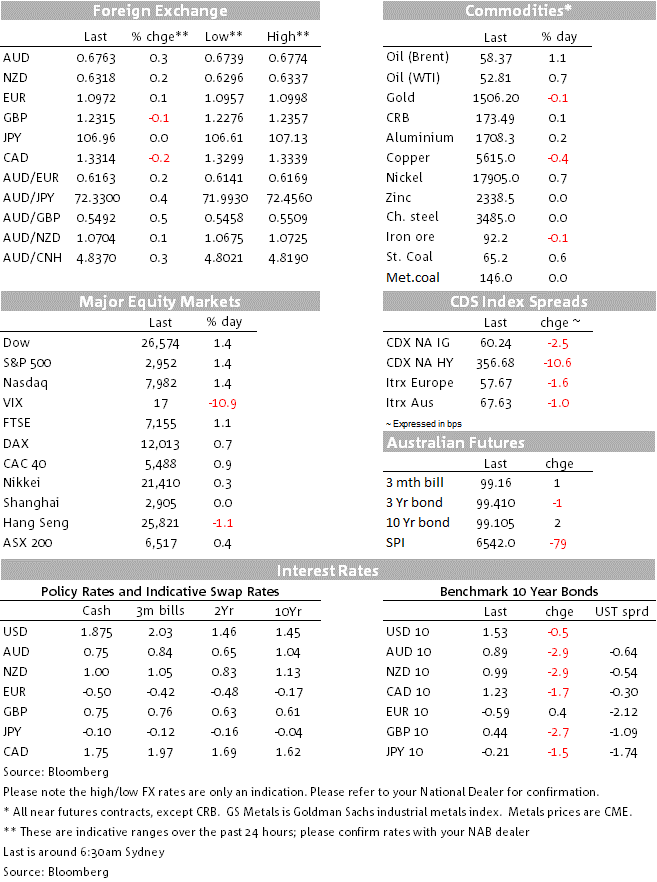

There was something for everyone in Friday night’s US employment report.

After an eventful week, Friday’s focus on the US employment report was an anti-climax, with a mixed report seeing only modest reaction to currencies and US rates. But with fears of another bad economic report allayed, US equities recovered strongly to unwind most of the loss seen earlier in the week.

There was something for everyone in Friday night’s US employment report, with most happy to look on the bright side, following the shockingly weak ISM manufacturing and non-manufacturing reports earlier in the week. The 136k rise in non-farm payrolls for September was slightly softer than the market consensus, although probably stronger than some feared and with positive revisions (+45k) for July/August adding to the positive vibe. Also of note was the fall in the unemployment rate to a 50-year low of 3.5% – so while employment growth is clearly on a weakening trend, it has still been strong enough to see a lower unemployment rate. Surprisingly flat wages saw annual wage inflation fall to 2.9%, the weakest reading since mid-2018, casting more doubt about the inflation outlook.

Rather than jump on the weak wage inflation reading, the market was prepared to accept that compositional effects might have caused the errant figure and seemed to put more weight on the evidently tighter labour market. This saw the market price a slightly reduced chance of a late-October rate cut, although still around 70% depending on how one calculates this. The US 2-year Treasury rate rose by as much as 4bps to a high of 1.43% after the release but closed up just 1bp at 1.40%. The 10-year rate closed down by less than 1bp to 1.53%, a muted response considering the big fall earlier in the week that saw it down by 15bps for the week.

With a stronger employment report than feared, the S&P500 rebounded by 1.4%, recovering most of less seen earlier in the week, taking its weekly loss to just 0.3%.

Fed Chair Powell’s short speech, due to be delivered after the employment report, was widely anticipated but came across as a non-event, with him simply reiterating the “economy is in a good place but faces some risks” story. Fed President’s Rosenberg and Mester also spoke after the employment report but weren’t willing to give guidance on their policy views, both wanting to look at the incoming data before the late-October meeting.

Currency markets didn’t react significantly to the US employment report. Improved risk appetite saw the AUD one of the better performers on the day, finishing +0.4% to 0.6770. There was little market reaction to the modest 0.4% lift in August retail sales, with the market still left wondering what happened to the tax refunds that began flowing in early July. A key takeout from the RBA’s Financial Stability Review was the Bank seeing risks relating to the housing market having “receded somewhat” over the past six months, given the uptick in housing market activity. The RBA called on banks to be “not overly cautious in the implementation of current lending policies”, a nod perhaps to some further easing up on APRA/ASIC’s interpretation of lending standards.

The NZD was up around 0.3% to 0.6320, with the gain coming during local trading hours. CFTC data showed yet another record net short speculative number of contracts (42k), equivalent to a notational USD2.7b, around the time the NZD had made a fresh 4-year low just above 0.62, following the weak ANZ and QSBO business surveys earlier in the week. The more than one cent lift later in the week might have reflected some covering of short positions. Positioning in the AUD showed net speculative shorts increasing to 52k contracts – high, but close to its average level over the past three months.

EUR was flat around 1.0980 and GBP was flat around 1.2330. The fog of Brexit continued to hang over the market. Boris Johnson’s lawyers promised a Scottish court that the PM will obey a law that forces him to postpone Brexit if he can’t reach a deal before 31 October. But Johnson later tweeted “New deal or no deal – but no delay. #GetBrexitDone #LeaveOct31”. Sigh. Enough said.

The calendar in the week ahead is fairly light, with fresh trade talks between the US and China this week likely to be the focus of market attention. US CPI data (Thursday night) will be closely watched for a guide as to whether the recent pick-up in US core inflation is just transitory or important for the outlook for Fed policy. FOMC minutes of the September meeting will look a little dated in light of the fresh downside to ISM manufacturing and non-manufacturing data. A number of Fed speakers through the week, including Chair Powell in the early hours of Wednesday morning, will keep the focus on US monetary policy.

The Fed’s George speaks this morning, while German factory orders will be released tonight to provide a further gauge of the depth of the recession in Germany’s manufacturing sector.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.