Online retail sales growth slowed in May following a fairly strong April

Insight

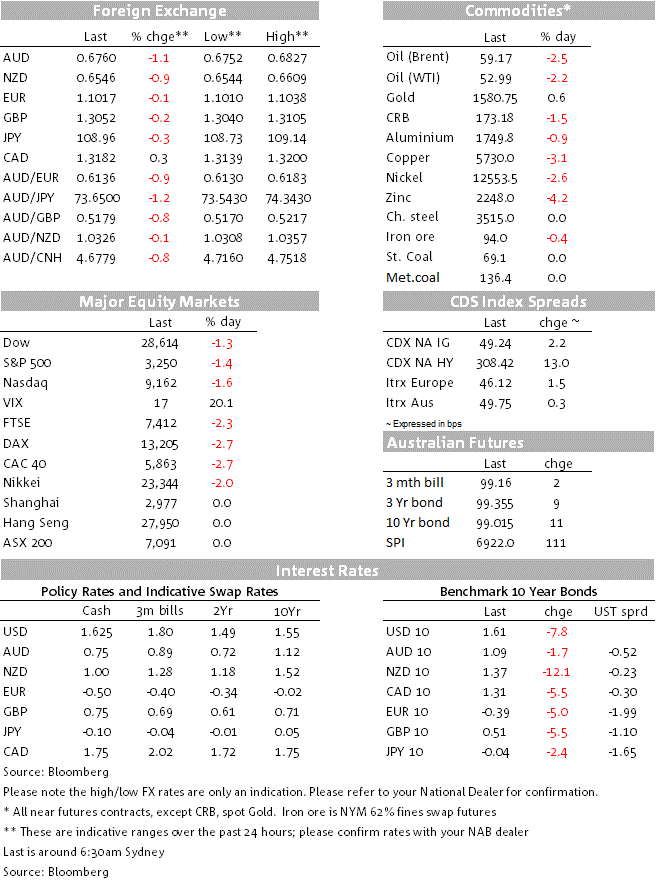

The Australian dollar has fallen more than one percent today as concern continues over the spread of the Corona virus.

https://soundcloud.com/user-291029717/spreading-virus-extends-risks-aussie-hit-hard

Northern Hemisphere markets awoke to the news of a swath of further Novel Coronavirus (nCoV) infections and an acceleration in news reports. It’s been “risk-off” dominating financial markets overnight trading. As of late London time, the number of confirmed infections was 2,886 (2,827 of these in in China, the number of deaths up to 81. Australia has four confirmed cases, the UK none (so far), the US 5 and others spread throughout Asia. The US Centers for Disease Control & Prevention (CDC) said Monday that “the immediate health risk from [coronavirus] in the U.S. is currently considered low”, that it’s a “rapidly evolving situation” and that reported illnesses in infected people had ranged from little to no symptoms to people being severely ill and dying.

It would be difficult to argue that the policy response from within China – where the virus was first detected – has been anything other than prompt and strong, overall. Happening at the time of the Lunar Year, closing down public transport and effectively clamping down on travel from 16 cities is one such example. Many will have seen the reports of the new Huoshenshan Hospital in Wuhan that from the looks of the buildings erected so far, is being constructed in record time. The first unit of the hospital seems to have been constructed in 16 hours (that’s hours not months, weeks, or days) with construction apparently on track to be finished and ready for use by February 2 to take up to 1,000 patients.

The Lunar New Year has already been extended to February 2, while in Shanghai to February 9 to limit the spread of the disease.

What is not known is how much further the nCov will spread, in China and elsewhere. Only time will have the answer to that question. What is becoming a little clearer is that the Chinese economy will take a hit for a time, travel and tourism is being impacted in China, in Asia and elsewhere, including in Australia where the Chinese inbound tourism market is the largest market in exports of personal tourism and education.

Demand for bonds and gold has risen, while oil (less travel) and industrial commodity prices have fallen back, iron ore down smartly at the start of the week in Singapore trading, base metals also lower. Iron ore futures are down to $84.85/t, having been in the $90s last week while LME copper is down 3.09% to $US5,743/t. In the circumstances, gold is up a relatively modest 0.40% to $1584.5/oz.

US stocks were lower again overnight, following the decline in European stocks. The Eurostoxx-50 closed down 2.23%, the FTSE, DAX, and CAC-40 faring no better. Bond yields have opened lower again, German 10y bunds down 5bps to -0.385% and US 10s down so far a net 7.59bps to 1.608%. AU 10y bond futures have rallied to 99.02.

While Asian currencies have been sold lower, it’s been the hit to commodity currencies that have seen larger declines. The Norwegian Krone is down a net 1.07%, USD/NOK at 9.14 on the back of a further hit to oil prices, WTI down 2.12% and Brent down 2.44% as we go to press, a little above their intraday lows.

After the NOK, next on the selling list has been the commodity- and China-sensitive AUD that broke through the 0.68 level in what was a limited APAC session yesterday and into the mid 0.67s during the London session overnight, AUD/USD currently trading at 0.6760. The NZD was also sold lower, but at the margin somewhat less. The VIX index is up 2.57 index points to 17.11. There has been some demand for the Japanese yen and the Swiss Franc today, while USD/CNH is around 6.98.

The EUR has been little changed before and after release of Germany’s Ifo survey for January, markets understandably more fixated on nCoV news for the moment. While Friday’s PMIs for Germany suggested that the German economy might be beginning to improve, the German Ifo Survey was less clear. The Survey’s Expectations index was down 0.9 index points while the Current Assessment index rose 0.3 points.

The survey reflected an improvement from low levels in the Trade and Manufacturing sectors, a slightly lower level for Services but a more discernible decline for Construction as the main drag. Weather, short-term factors could have been at play. The Ifo’s Clemens Feust was speaking in an interview on a more positive outlook for manufacturing that is recovering even though it is not extending to the auto industry at this point.

The UK Bankers’ Association reported today that bank lending for housing surged in December. It was up 19% on year-earlier levels and the highest December since 2013. This further piece of evidence of a turn in the UK housing market adds to the emerging picture of a December of “two halves” another element of a Boris bounce if you like. The UK Government is making two important decisions this week, first on whether to invite Huawei to participate in the building of the 5G network and the second on whether to proceed with the high-speed rail HS2 project, costed in the vicinity of £100bn. Sterling is little changed overall, EUR/GBP having tested lower earlier in the London session.

US New Home Sales were shy of expectations, quite possibly a degree of payback after an exceptional run, bearing in mind the continued strength in demand indicators such as the NAHB Home Builders’ index and that the US HomeBuilders stock index is up 0.2% in a heavy market.

Ahead of the RBA next week, the two most important domestic releases are the NAB Business Survey for January and tomorrow’s December quarter CPI. It will be interesting to see what discernible impact the bushfires have had on confidence as well as the underlying performance of the economy.

Ahead of the FOMC on Wednesday, the US releases Durable goods orders for December, there’s January US Consumer Confidence from the Conference Board as well as the Richmond Fed manufacturing index.

The UK has the January CBI Retail sector survey, not an indicator that gets much attention but might this time.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.