Online retail sales growth slowed in May following a fairly strong April

Insight

Equities have been helped by some strong data from the US and continued hope on a stimulus deal.

https://soundcloud.com/user-291029717/strong-us-data-with-no-room-for-chicken-lickens?in=user-291029717/sets/the-morning-call

“Summer has come and passed; The innocent can never last; Wake me up when September ends”, Green Day 2005

Risk sentiment bounced overnight on optimism that a US fiscal package can be agreed to, and as economic data came in stronger than expected. However, that optimism was pared somewhat towards the end of the day after US Treasury Secretary Mnuchin said “we still don’t have an agreement”, but hopes have been kept alive with Pelosi and Mnuchin set to meet again tomorrow.

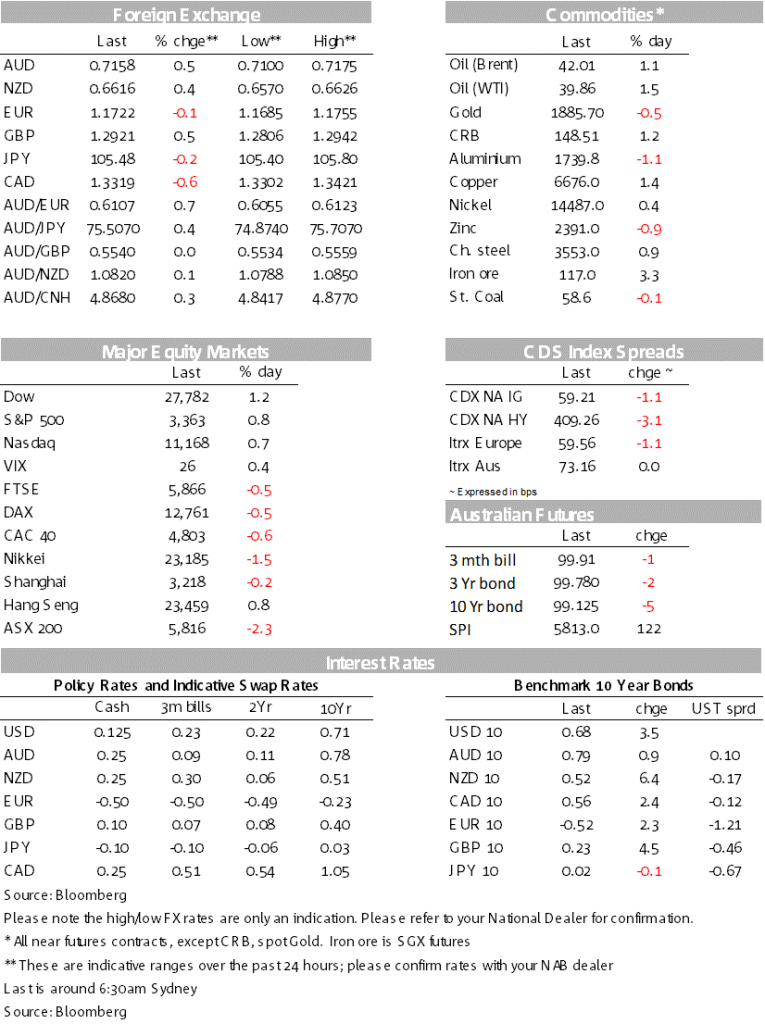

The S&P500 pulled back from session highs on that late headline, though finished still well in the green at +0.8% (range +0.1 to +1.7%) and notably shook off the negative lead from Europe (Eurostoxx 50 -0.6%) and the fallout from the US presidential debate (S&P500 futures in Asia at one point were down -1.3%). Yields also moved higher, with the US 10yr +3.5bps to 0.68%. So ends September with the S&P500 down over the month -3.9%. As for FX, September was the month where the USD rebounded (DXY +1.7%) as Euro fell (EUR -1.8%), while the USD/Yen was little moved. The worst performing currencies over the month were AUD (-2.9%), GBP (-3.5%), SEK (-3.6%) and NOK (-6.8%).

Hopes of a US fiscal stimulus package were buoyed overnight after Treasury Secretary Mnuchin said he was “hopeful that we can get something done. I think there is a reasonable compromise here”, with those comments coming before a meeting with House Leader Pelosi who was also “hopeful” for deal.

No agreement was reached despite more than 90mins of talk, with hopes for a deal pared somewhat but not extinguished. Mnuchin and Pelosi are set to meet again, while Mnuchin continues to be positive “we still don’t have an agreement, but we have more work to do. And we’re going to see where we end up”; “made a lot of progress over the last few days”.

If an agreement between Mnuchn and Pelosi can be reached, Senate Republicans are likely not to step in the way given prior comments. Meanwhile House Democrats meanwhile delayed a vote on their $2.2tn proposal to buy time in talks.

That was notably mixed. Although it was initially “risk off” in the aftermath of the debate (S&P500 futures were down by as much as –1.3% at one stage), the turnaround in stockshas led to a number of high-profile Wall Street commentators stating the stock market doesn’t seem upset with the prospect of a Biden win (e.g. former Goldman’s CEOBlankfein tweeted: “so far the stock market doesn’t seem too upset at the prospect of Biden winning, despite Trump’s more market friendly policies.

Perhaps folks think their stocks and 401(k)s will do better with higher taxes and increased regulation than with nastiness and scorched earth”). It seems what would be more upsetting is a contested election where the result is not known for weeks/month – reinforced in the debate where President Trump’s refused to say he will accept the poll result and continued his criticisms of mail-in-ballots.

That outcome though becomes less likely if Biden wins by a clear majority and in this vein post-debate polls scored in favour of Biden (though remember they did as well for Hillary).

The stock market also is seemingly backing Biden with solar stocks surging overnight on the back of Biden’s energy plan which includes increased use of solar and wind.

And helped boost sentiment. The Chicago PMI was 62.4 v 52.0 expected, and the highest since December 2018. Together with the other regional manufacturing surveys suggests some upside risk to tonight’s ISM Manufacturing where the consensus sits at 56.4.

There was though one worrying anecdote within the survey and that was firms continuing to mention additional layoffs in September, and thus reinforcing notions of the labour market recovery having stalled. ADP Employment for September also beat at 749k v 649k expected and suggestive of Payrolls printing within the ballpark of consensus on Friday.

High-frequency data such as HomeBase are suggestive of stalling occurring in the labour market recovery and we will be watching Jobless Claims tonight closely. Finally, Pending Home Sales were strong (8.8% m/m v 3.1% expected) and reinforcing the strength seen in the housing market.

And with activity broadening out to the non-manufacturing sector. The Manufacturing PMI beat expectations (51.5 v 51.3) as did the Non-manufacturing PMI (55.9 v 54.7 expected). Note for the next week China will be quiet with the week-long Golden Week Holidays from today to October 9. It is also possible production ahead of the holidays helped spur demand.

The AUD rose +0.6% to 0.7164 and has made a remarkable turnaround after hitting a low of 0.7006 on September 26. CAD also lifting by a similar amount with USD/CAD -0.6% to 1.3319, as is NZD +0.5% to 0.6618.

Other FX pairs were more mixed with EUR was choppy -0.1% to 1.1726 amid two notable headwinds. Firstly, there could be a delay to the key EU Recovery Fund, the same fund that initially parked the recent rally in the Euro. The controversy surrounds protecting EU funds from fraud in cases where institutions are weak with details yet to be worked out. Overnight the European Commission in a report singled out a few Eastern European countries with law deficiencies to investigate and prosecute high-level corruption.

That met with strong criticism from Hungary and Poland and spokesman for Germany said that “A delay of the EU budget and the recovery fund is becoming increasingly likely”. Secondly, ECB President Lagarde gave some support to looking at the Fed’s new “average” inflation targeting strategy as part of the ECB’s monetary policy strategic review due mid next year. Such a strategy allows for a period of above-target inflation following a period of sub-target inflation (see Reuters for details).

Bank of England Chief Economist Haldane added to the chorus that negative rates aren’t imminent in the UK, saying work is likely to take months. He outlined three conditions before judging whether negative rates should be applied and none were currently satisfied: operational feasibility; macro necessity for further stimulus; and conviction that the benefits outweighed the costs.

A quiet day domestically with only House Price data likely to garner much interest. Weekly data from CoreLogic suggests prices fell -0.3% m/m across the capital cities, largely due to falls in Melbourne with positive price growth in Adelaide, Brisbane and Perth.

Offshore it is also quiet with only the US with top tier data with the ISM Manufacturing, Personal Consumption/Expenditure, and Jobless Claims. For more details, please see below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.