Online retail sales growth slowed in May following a fairly strong April

Insight

The US finished on a high last week.

https://soundcloud.com/user-291029717/stronger-earnings-surprising-gdp-but-no-grand-deal?in=user-291029717/sets/the-morning-call

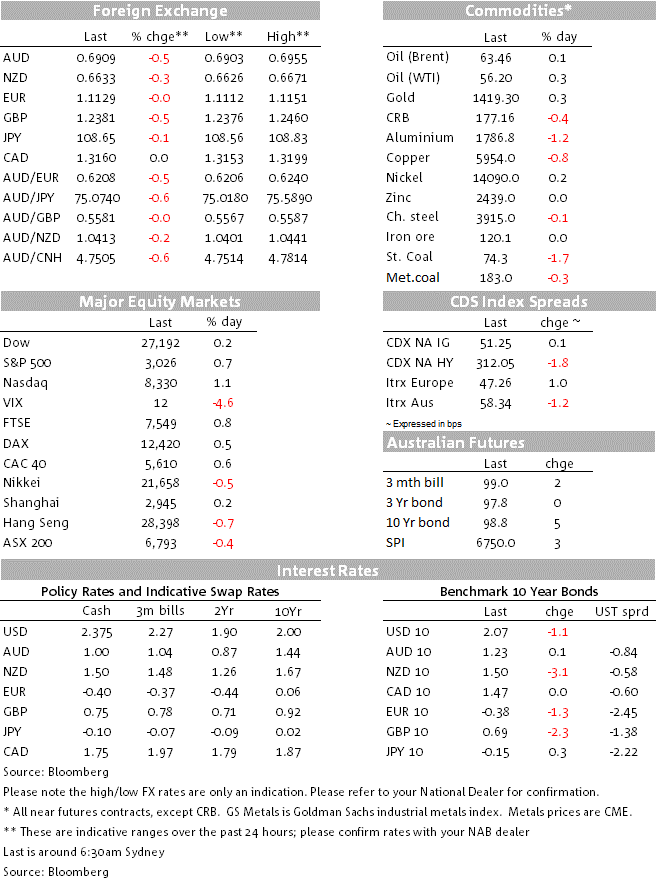

Titanium features highly in my workout beats playlist and its lyrics of “you shoot me down, but I won’t fall, I am titanium” is an apt description of the US economy at the moment. On Friday US Q2 GDP beat expectations at 2.1% annualised against 1.8% expected, while the y/y figure was 2.3%. The case of the US economy remaining the least dirty t-shirt in the laundry basket remains – as reference Q2 Eurozone GDP on Wednesday is expected to be a more meagre 1.0% y/y. The USD was stronger across the board in response with DXY +0.2%, helped along by Kudlow’s comments of the US having “ruled out” FX intervention (Trump though added a layer of ambiguity, stating “I didn’t say I’m not going to do something”). The AUD was one of the weaker G10, down -0.5% close to breaking through 0.69 being at 0.6907. GBP was also weak, down some -0.5% to 1.2381 on growing hard-Brexit fears. Yields though were little moved (US 10yr -1.1bp to 2.07%) , with US Core-PCE inflation softer than expected (1.8% annualised v 2.0 exp; but importantly is 1.5% y/y) and weakness in Business Investment keeping alive prospects of an extended Fed easing cycle.

Delving into the GDP figures in detail reveals Consumption being the main driver with Personal Consumption +4.3% annualised, up from the subdued 1.1% pace in Q1. GDP growth though was dragged down by weakness in business investment (-0.6%), net exports (-0.7%ppts) and from inventories (-0.9ppts). There were also sizeable revisions to the GDP report which serves as a reminder that these figures are far from gospel – 2018 growth was revised down to 2.5% y/y instead of the initially reported 3.0%, while 2018 Q4 growth was revised sharply lower to 1.1% annualised instead of the 2.2% initially reported. Adding to the softer gloss was a below expected Core-PCE deflator which was 1.8% annualised and below the 2.0% expected. In year-ended terms core inflation is running at a meagre 1.5% and below the Fed’s 2% inflation target.

US profit reporting season also continues to show strength. Of the nearly 40% of companies to have reported so far, over 75% have beaten expectations, and Alphabet was out on Friday with its stock up some 10% after beating expectations and announcing a share buyback. The end result is that despite global growth headwinds, the S&P500 and the Dow have hit new record highs – S&P500 +0.7% to 3,026. Note Australia’s profit reporting has kicked off with Rio Tinto due to report on Thursday.

Chinese Profits out on the weekend has kept alive global growth fears with Industrial Profits -3.1% y/y, well down from last month’s +1.1%. The slowdown in profits lines up with the soft producer prices seen earlier in the month and also suggests margins are being impacted by the US-China trade war. The details show Computer & Electronic production profits ‑7.9% y/y, though there was some strength in profits for Machinery and Construction Materials – a sign perhaps that stimulus is gaining traction. In line with some official commentary of reining in iron ore prices, profits for Iron Smelters was -21.8% y/y. Given such an outlook, it wouldn’t be a surprise to see further headlines of China investigating the iron ore price and also perhaps further industry consolidation.

Hard-Brexit fears continue to sink Cable, with GBP -0.5% to 1.2382 and around the lowest levels since March 2017. Prime Minister Johnston has said he intends to deliver Brexit “by any means necessary”, while Gove told the Sunday Times that the government is working on the assumption of a no-deal Brexit. Betting markets currently ascribe a 36% chance of a hard-Brexit, up from 30% on Friday. While we continue to hold the view that Parliament remains opposed to a no-deal, until we see Parliament baring its teeth with a meaningful majority GBP looks like it will trade weaker through the Summer (31 October is the current Brexit date).

The AUD remains on the backfoot, down -0.5% since Friday and is -1.9% over the week to 0.6910. Driving the weakness is a combination of USD strength (DXY +0.8% over the past week), alongside reaction to Governor Lowe’s speech on Wednesday which gave implicit forward guidance that rates were going to be low for an extended period of time and the RBA is willing to cut again, while its commitment to the inflation target at a time of subdued global inflation implies further easing could be on the table.

Finally, the tentative stabilisation in the Australian Housing Market continues with Auction Clearance Rates at 71.2% compared to 55.6% this time last year. The total volume of auctions though remains lower with 1,115 auctions compared to 1,536 this time last year.

It is a quiet day ahead with no major data releases scheduled (Japan has Retail Sales and the US the Dallas Fed Manufacturing Index). US-China trade talks restart today, though expectations are low with White House Economic Advisor Kudlow stating “I wouldn’t expect any grand deal” and President Trump implied he is going to stick to his hard line stating: “I think China will probably say let’s wait. It’s 14, 15 months until the election….I’ll tell you what, when I win [the 2020 election], like almost immediately they’re all going to sign deals. They’re going to be phenomenal deals for the country.”

It is a very busy week ahead with Wednesday shaping up to be a key focal point with a likely US Rate Cut and Aussie Q2 CPI:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.