We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Markets have controlled their excitement after the burst of optimism over a potential COVID-19 vaccine.

https://soundcloud.com/user-291029717/taking-a-deep-breath?in=user-291029717/sets/the-morning-call

Equity markets have failed to build on Monday’s exuberance which was driven in part by the excitement over US drug company Moderna’s early COVID-19 vaccine test results and the associated thoughts that instead of only 90% of the global economy being back in action next year, 100% is possible if a vaccine exists by then.

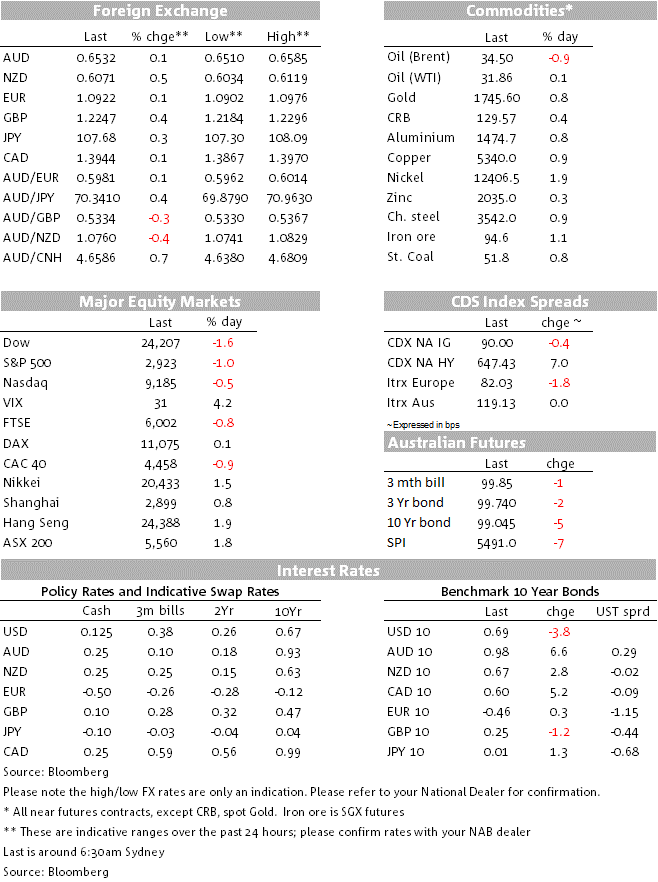

Having been bouncing about around flat, US indices fell away in the last hour of trading (S&P 500 ending -1%) following a ‘STAT’ report (Statnews.com) saying that Moderna withheld some key information about its coronavirus vaccine, citing the lack of a National Institute of Allergy and Infectious Diseases (NIAID) press release and missing information needed to interpret the data. Moderna says it will supply this at later date, according to Bloomberg. Moderna’s stock is back below $72, having jumped from $65 to $85 on Monday and managing to sell $13bn worth of new stock, valuing a company with zero revenue at $29 billion. Ring any bells?

Comments from Fed Chair Powell and Treasury Secretary Mnuchin before the Senate Banking Committee last night failed to make much market impact, Powell saying that more fiscal stimulus may be needed but being more circumspect in his remarks than previously (perhaps because of the new political bun fight emerging in Congress following the House of Reps. passage of a $3tn support package that looks certain to be rejected by the Senate). Mnuchin said that the Treasury intends to fully utilise the agreed $500bn authorised for the Treasury by Congress for direct lending to medium sized firms, and said ‘we are fully prepared to take losses in certain scenarios on that capital’.

Interest rate markets are showing modest decline in US Treasury yields, with 2s -1.4bps to 0.163% and 10s -3.6bps to 0.688%. Earlier, European bonds ended mostly lower, led by Spain and Portugal which both saw their 10-year benchmark -9bps (German Bunds were little changed). A story to note here is an interview in Die Zeit magazine with German FinMin Olaf Sholtz, in which he invokes Alexander Hamilton (the father of US fiscal union) as a role model for the EU, arguing that more integrated fiscal policy could be an important start on the path to (EU) reform. He says pan-Eurozone debt should not be taboo and even quotes Winston Churchill’s famous quip about not letting a good crisis go to waste. Some other EU countries (you know who) are saying they will forward their own proposals (after the Franco-German accord on Monday to seed a EUR500bn Recovery Fund that would be distributed in the firm of grants); so there is a long way to go here, but the omens from the EU’s biggest member are undoubtedly positive.

The other bit of positive news from Germany was the jump in the expectations component of the ZEW survey, to 71 from 28.2 and well above the 30 expected, even though the current conditions reading fell further, to 93.5 from -91.5. In other economic news, UK jobless claims surged by 857k in April to 2 million, taking the claimant count rate to 5.8%, its highest in more than two decades and the UK chancellor warning it could rise to 10%. US housing starts and permits plunged by record amounts, but were in line with expectations. Closer to home, the latest GDT dairy auction price index gained 1%, a slightly better outcome than the small fall in pricing our BNZ colleagues expected.

ECB President Lagarde said that the ECB would continue its QE programme despite the ruling from Germany’s top court questioning the legality of the programme, saying “each national central bank in the euro area is independent and cannot take instructions from governments. This is laid down in the treaty”.

The NZD and AUD extended their local session gains during the European day, AUD/USD breaking up though the 0.6570 recent range highs to 0.6585 before dropping back alongside the late US day equity market fall-back to below 0.6550. AUD took only minor hit late in the APAC day yesterday on the Bloomberg report saying China was considering targeting more Australian exports, including wine, seafood, oatmeal, fruit and dairy. This latter news may have had a hand in NZD outperformance (AUD/NZD back to around 1.0750 from above 1.08) together with the strong push back from RBNZ officials yesterday to any thoughts the central bank might renege on its public commitment to keep the OCR at 25bps at least until March 2021 (and instead resort to lower – including negative – rate before then). Having earlier poked its nose above 0.61, NZD/USD has fallen away into the New York close to near 0.6075.

The Big USD, having fallen away on Monday and most of Tuesday, has recovered in the NY afternoon alongside the deterioration in risk sentiment, to remains very much ‘home on the range’, in narrow DXY terms defined as 99 -101 (99.60 now).

The ABS releases its preliminary April retail sales report at 11;30, where we look for a big (7%) payback after the 8.5% March leap on panic buying of essential items.

China Loan Prime Rates (LPR) will be announced at 13;30, but after Medium Term Lending Facility rates were left unchanged last week, the LPRs are expected to stick at 3.85% (1-year) and 4.65% (5-year)

Tonight, the UK and Canada have April CPI, and early tomorrow morning latest FOMC Minutes are published.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.