Long-term signal vs. Short-term noise

Insight

There’s been big moves on equities and bonds today as talks between the US and China appear to be back on.

https://soundcloud.com/user-291029717/talks-back-on-bonds-sell-off?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s research support please let your company’s representative know

Windmill, windmill for the land Turn forever hand in hand….Windmill, windmill for the land, Is everybody in? – Gorillaz

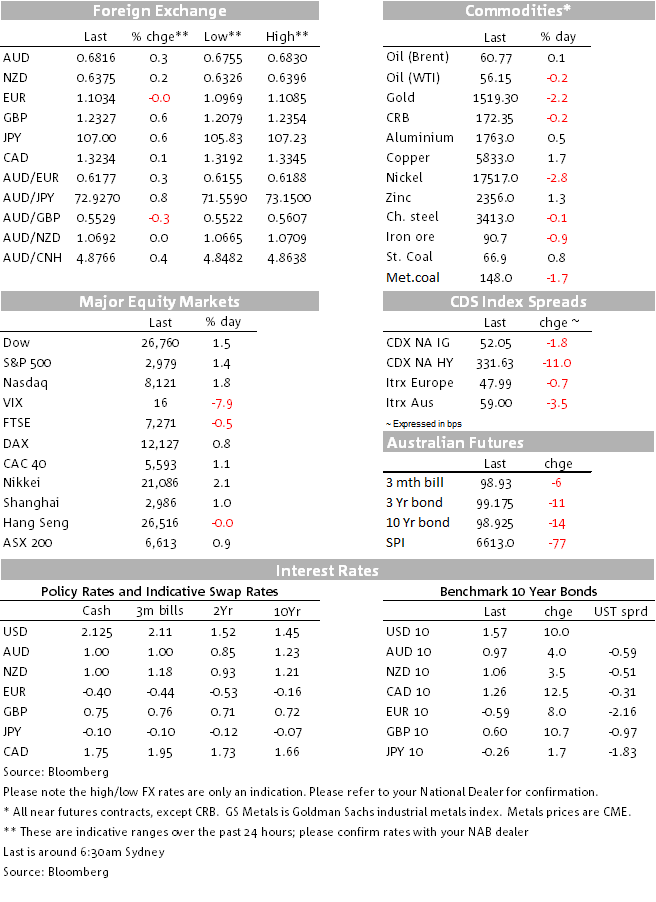

Who said talk is cheap? The feel good vibes have continued in the overnight session boosted by yesterday’s confirmation by China that high level trade talks with the US will resume in October. Strong US data releases added further fuel to the positive vibes, lifting UST yields along the curve while US and European equities enjoyed a second day of solid gains. The USD had a steady night losing ground against pro-growth currencies, including the AUD and NZD while safe haven pairs (JPY and CHF) are the big losers. GBP has continued its recovery on Brexit optimism

Yesterday risk assets were already travelling with a spring in their steps on the back of good news from Hong Kong, Brexit and Italian politiucs. Then, Chinese officials gave a strong signal of imminent economic stimulus followed by China’s confirmation that high level trade talks with the US will resume early in October, while lower-level officials will have discussions over the coming weeks to prepare for the talks. Prospects of new high level trade talks in spite of a new round of trade tariffs, had already been heralded by President Trump, but the lack of confirmation from China had kept the market wary.

Thus a positive lead from the APAC region boosted risk assets as Europe began its trading day with strong US data releases at midnight (Sydney time) adding an additional boost to the feel good vibes. Ahead of the US non-farm payrolls release tonight, the ADP private payrolls number for August printed at 195k comfortably beating the 148 expected by markets and the ISM non-manufacturing (Aug) also beat expectations coming at 56.4 vs the 54 pencilled in by economists.

The August ISM non-manufacturing print was the strongest since April and it allay fears of contagion from a contracting manufacturing sector. Looking across the components, orders were very strong at 60.3 up from 54.1, the Business Activity reading was a punchy 61.5, up from 53.1 and the prices paid sub-index was up to 58.5 from 56.5. All these sub-indices point to activity resilience, bucking the trend however the employment index fell to its weakest level in more than two years and, combined, with the ISM manufacturing employment index, the data signals sub-100k monthly payroll growth towards the end of the year.

Looking ahead and bearing in mind China is celebrating its 70th anniversary of the founding of the Peoples Republic of China with national holidays from 1st to 7th of October, our sense is that US-China trade developments are likely to be put in the back burner until then. This then suggests that a market friendly environment of no new US-China trade news over the coming weeks looks likely with focus over the remainder of September set to be centred around major central banks policy intentions. The ECB meets September 12th followed by the Fed on the 17th-18th and the BoJ on the 18th and 19th. Barring the BoJ, which in our view is likely to sit on its hands, both the ECB and Fed are expected to ease over the coming weeks.

Awful German factory orders (Jul: -2.7 vs. -1.4 exp.) released overnight reinforce the view that the ECB needs to deliver a new round of stimulus on the 12th, but with clear divisions between northern vs other council member, questions still remain on the content and potency of the “new bazooka” or “gun pistol” for that matter. US non-farm payrolls are out tonight and a solid print may put some doubts on the need for another rate Fed funds rate cut in September, Fed Chair Powell speak early tomorrow morning (see more below) and ahead of the FOMC meeting, next week we get new US readings on retail sales and inflation.

US Treasury yields were already trending higher ahead of the overnight US data releases, but post the data prints Treasuries extended their losses, marking their worst day since January. 2 and 10-year rates are now trading just over 10bps higher relative to yesterday’s levels at 1.540% and 1.559% respectively. European rates are also much higher, with German, French and UK rates up between 8-11bps. The sell-off follows the massive rally through August and is a reminder that markets don’t always move in a straight line. The negative tone towards bond markets has been exaggerated by some record-breaking issuance of corporate bonds (49 US deals in 30 hours totalling $54b, Bloomberg reports), as companies look to take advantage of low rates to lock in some reduced borrowing costs.

Looking at currencies, the USD is little changed in index terms with the DXY index at 98.41 (-0.03%) and BBDXY at 1210.5 (-0.04%). A closer look at its components, shows a divergence in fortunes with EM FX and pro-growth currencies such as the AUD and NZD outperforming while JPY and CHF, the traditional safe havens, are the big underperformers. CHF (-0.62%), now trades at 0.9868 while USD/JPY now trades at ¥106.94, after trading to an overnight high of ¥107.21. The latter continues to show a strong correlation to the move in 10y UST yields courtesy of the BoJ Yield Curve Control policy.

The AUD currently trades at 0.6815 and after looking a little bit undervalued early in the week, based on our fair value models, the recovery in the aussie can be attributed to the RBA’s lack of urgency to lower the official cash rate again as well as the broad improvement in risk appetite. On the RBA score we note that similar to the previous day’s AFR article, the WSJ’s James Glynn suggested that the RBA’s base case is for another rate cut in November, but data could push the Bank over the line to an earlier cut in October. The 0.6825/30 region remains a near term resistance for the AUD, but if we are right about our assessment that risk assets are likely to enjoy a friendly environment over the coming weeks, we think the AUD has a good chance of heading towards the 69c mark.

The NZD pushed higher yesterday to 0.6375 after the announcement that US-China trade talks would resume. In overnight trading it pushed up to a high of 0.6396, before the stronger US data saw it fall back down to 0.6375. This will see the 0.64 level marked as an area of resistance in forthcoming trading.

GBP has been the best performer and is up some 0.9% since this time yesterday to 1.2325, as a no-deal Brexit looks increasingly unlikely. Confirmation that legislation designed to stop a no-deal Brexit on Oct. 31 will be completed in the House of Lords by Friday 5pm( local time) and now a new vote on an early election is scheduled just before Parliament is due to be prorogued – or suspended – from next week until 14 October.

The BBC reports that Brexit Party leader Nigel Farage has warned Mr Johnson that he “cannot win an election, whenever it comes, if the Brexit Party stands against him”. However, if they were to make a pact during a general election “with a clear policy, we’d be unstoppable”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.