Total spending grew 0.9% in June.

Ray Attrill explains how the latest small business survey data in the US shows signs that tariffs on Chinese imports might be starting to make their mark.

https://soundcloud.com/user-291029717/tariffs-bite-as-powell-prepares-to-testify?in=user-291029717/sets/the-morning-call

“You told all the callers you were not amused oh I’m looking for clues” – Robert Palmer

Overnight markets have been mostly about positioning into the first of Fed Chair Jay Powell’s two Congressional testimonies starting at midnight AEST tonight. US yields and the US dollar have continued to push higher, the DXY index by 0.13 to 97.5 to now be some 1.75% off its late June lows. 2-year US Treasury yields are another 2.3bps higher at 1.913% and 10s up by 1.9bps to 2.067%. US stocks don’t like the interest rate messaging, more so than acting with any particular trepidation in front of the US earnings season that kicks into gear next week, with the Dow ending -0.1% and the S&P 500 up but by only 0.1%

One fresh piece of Fed commentary in front of Powell’s testimony has been an interview with the Wall Street Journal, Federal Reserve Bank of Philadelphia President Patrick Harker that he doesn’t see a “compelling reason” for the Fed to cut rates. “Though slowing global growth and uncertainty over trade policy have created clear risks to that outlook,” Harker added and further reiterated that the U.S. economy continues to be strong. This tells us that he was one of the eight ‘dots’ indicating no change to Fed policy this year as of the June FOMC meeting, but doesn’t alter our expectation that a 25-point rate cut this month is almost certain (noting too that Harker doesn’t have an FOMC vote this year).

One piece of US economic news to note overnight has been the latest NFIB (small business) survey. There was nothing significant in the headline index which fell to 103.3 from 105.0, virtually in line with expectations, but the Selling Prices sub-series leapt to 17 from 10 (when gasoline price falls were suggesting it should have been down). This looks to reflect the impact of the lift in tariffs on $200bn worth of Chinese imports to 10% from 25%, announced in May but which will have only impacted when Chinese imports started to hit US shores in June.

The Fed has been clear it will look though any tariff-induced pick up in US inflation (and which will after all be a one-off hit to the price level, not the ongoing inflation rate). But it also serves as a reminder that were Trump to go the whole hog and tariff all Chinese imports if latest trade talks break down, the impact on consumer prices (and with that consumer spending) will be much more significant. As it is, some analysts are suggesting that the read-through from the NFIB survey is that core CPI could hit 2.7% in the coming year.

Also released overnight the latest JOLTS (job opening) report showed vacancies slipping to 7.323mn in May from a downward revised 7.372mn in April.

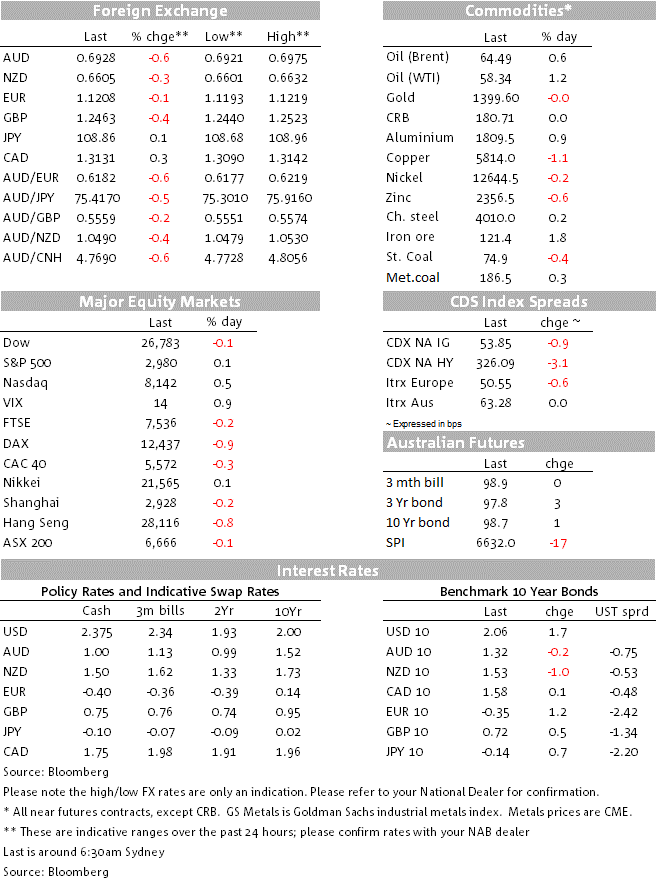

In currencies, the AUD is the weakest G10 currency of the last 24 hours off 0.6% to near 0.6925, followed by GBP, the latter -0.4% to its lowest against the USD since April 2017. With the exception of the CHF which was very marginally stronger, all G10 currencies are weaker against the rising greenback.

The AUD was already on the back foot ahead of yesterday’s NAB Business Survey and where we suspect it’s a case of ‘the bigger they are the harder they fall’ in so far as the AUD (and NZD) have been two of the better performing currencies during the big dollar’s June decline. So a further shake-out of some longs sitting in weak hands would be our guess.

The NAB Business Survey pulled an already slipping AUD lower, albeit by only 10-20 point. The survey revealed that the post-election lift in business confidence was short-lived and that there is little sign of a turnaround in business conditions. Confidence reversed most of its sharp lift in May, to be at 2pts, while conditions were modestly higher at 3pts (from 1pt, below its long term average of 6pts).

Firms reported improved trading and employment conditions, both 3pts stronger to 6 and 5pts, respectively, while profitability remained at -2pts. New orders remained weak at -4pts. Note that the survey was undertaken after the June rate cut, predating the follow-up rate cut in July and the temporary boost to growth from the government’s personal income tax cuts. Capacity utilisation recorded a solid rise and is now back at 82.1% while price pressures were subdued, with final product prices still posting very weak growth even as labour cost growth picked up to 1.5%.

By industry, the small lift in business conditions in the month was driven by finance, business & property services and construction. Notably, retail conditions continue to lag, with retailers reporting conditions last seen in the depths of the global financial crisis.

GBP/USD reached a low of 1.2440, with markets remaining concerned about the slow-down in UK growth and the risk of a no-deal Brexit and possible new elections. There has been a feeble attempt at a rally on news that parliament has approved – albeit by just one vote- a motion to prevent a parliamentary shut down in order to facilitate a no deal Brexit on October 31st, but since then Boris Johnson, who betting markets ascribe a 95% chance of being the next PM, has been out in a TV debate saying he wouldn’t take anything off the table when asked if he would shut parliament to get a no deal Brexit done.

It’s been a very mixed night for commodities, with based metals mostly lower save for aluminium but iron ore and oil both up. Gold is flat. See table below for details.

The main event today is Fed chair Jay Powell testifying before the House Financial Services panel starting at midnight AEST. Powell, and rest of his FOMC colleagues, ‘don’t have a clue’ about Fed policy according to President Trump last weekend, which we can safely assume will not be the impression conveyed by the Mr Powell tonight, albeit his testimony might not prevent POTUS repeating the barb via his Twitter feed.

In the Monetary Policy Report submitted by Fed Chair Powell to Congress last Friday, the key passage, lifted from the June post-FOMC statement, is that “At the June FOMC meeting, however, the Committee noted that uncertainties about the global and domestic economic outlook had increased. In light of these uncertainties and muted inflation pressures, the Committee indicated that it will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective”.

We doubt that last Friday’s employment report will have meaningfully altered the Fed’s assessment of those uncertainties – and certainly not of underlying inflation pressures (or lack thereof) sufficient to put the market’s off the scent of a 25-point reduction in the Fed Funds target range on July 31st, but nor do we expect markets to be put in a position to re-embrace the possibility of a 50-point reduction (something ascribed no more than about a 6% probability at time of this update, in from closer to 50% this time last week).

Before that and indeed before the end of our day, Kansas Fed President Esther Fed’s George (historically hawkish but not a current FOMC voter) speaks in Helsinki at 15:50 AEST.

The FOMC June meeting minutes will be out at 4:00 AEST on Thursday

Locally, Westpac’s July consumer confidence survey is at 10:30 AEST, which recall in June failed to bounce (-0.6%) in the way that the NAB business survey’s confidence reading did, but the latter of course was not maintained in July.

China has June CPI and PPI (former seen unchanged at 2.7%)

In Europe, France Italy and the UK have latest industrial production (and the UK also May monthly GDP and May Construction Output)

The Bank of Canada publishes its latest rates decision at midnight AEST, the same time that Powell’s testimony starts. We don’t expect the BoC to be endorsing current market pricing that currently ascribes about a one-third chance to a 25-point rate cut by October; instead imparting a studious ‘steady as she goes’ outlook even if downside risks to growth from global trade tensions are highlighted.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.