Total spending grew 0.9% in June.

US and European equities rose sharply, with rising confidence seeing a fall in the US dollar and a rise in the Aussie.

https://soundcloud.com/user-291029717/taxing-issues-dont-hold-back-risk-sentiment?in=user-291029717/sets/the-morning-call

Risk rebounded from the get go overnight even though there was little news to drive the move. The S&P500 rose 1.6% following a 2.8% rise in the Eurostoxx 50, while Asia was more mixed especially after the US’ restrictions on SMIC (yesterday the US Commerce Department sent letters to US companies saying they would need export licenses to supply SMIC). Likely helping sentiment initially at least were the weekend reports of Pelosi and Mnuchin meeting, driving hope of a US stimulus deal being agreed to. That played to the broad-based nature of last night’s rally with a clear pivot to cyclicals (S&P500 Financials +2.3%; Energy +2.3%; Industrials +1.8%). However, Pelosi tempered that optimism, noting “he has to come back with much more money to get the job done”. The current Supreme Court nomination and talk of a disputed election are also starving the talks of much needed momentum. Month-end and quarter-end rebalancing was also cited given the sell-off over September (S&P500 is -6.2% since the September 2 high).

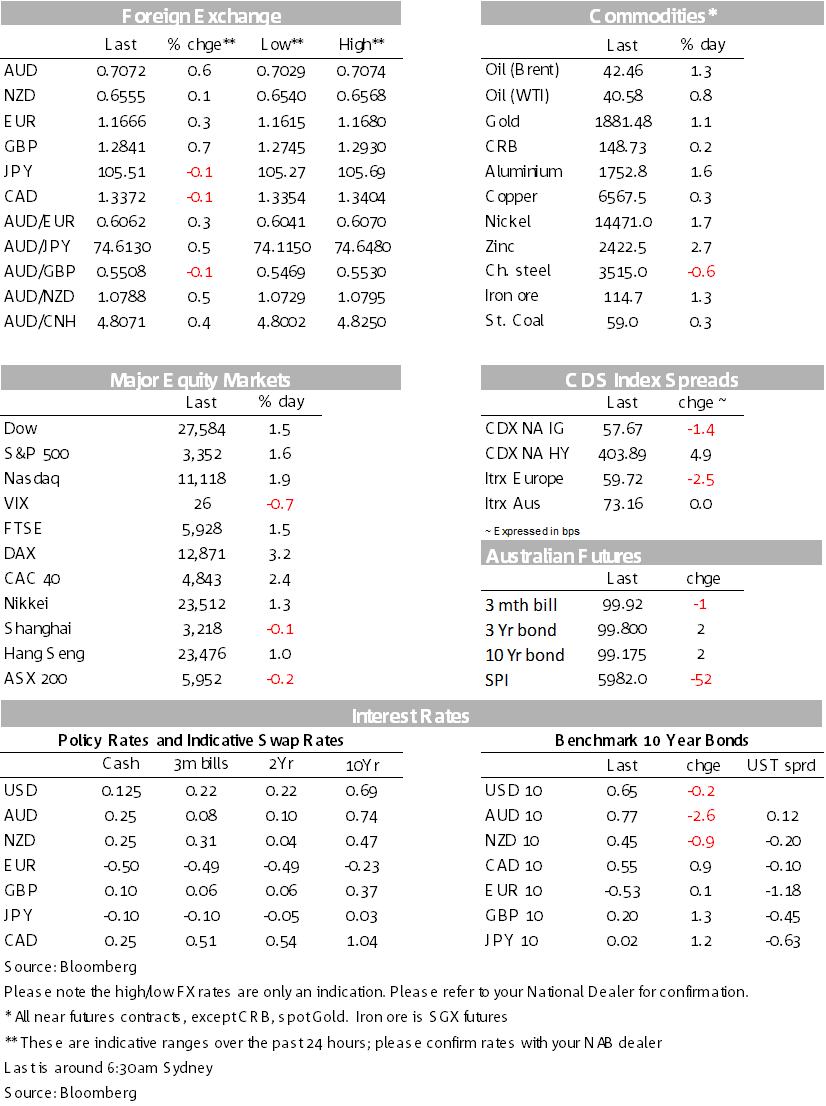

FX reflected the better risk tone, though again month/quarter-end flows are likely starting to be a factor as well. The USD (DXY) fell -0.3% to 94.27 with broad-based losses across the G10 space (EUR +0.3%, USD/Yen -0.1% and GBP +0.7%). There was little reaction in EUR to ECB President Lagarde’s comments to the European Parliament’s Economic and Monetary Affairs Committee, of the pandemic continuing “to weigh on economic activity and poses downside risks to the economic outlook” the ECB “continues to stand ready to adjust all of its instruments, as appropriate”.

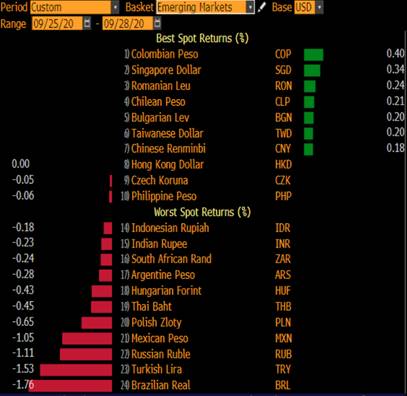

As for the USD, there was a diverging performance amongst emerging markets, suggestive of dollar strength playing out for a little while longer. The Mexican Peso and Turkish Lira both fell sharply against the USD overnight (USD/MXN +1.1% and USD/TRY +1.5%), albeit for very different reasons (see Bloomberg WCRS screen below).

GBP was clearly an outperformer overnight, up 0.7% to 1.2841 on less Brexit pessimism and the some hosing down of negative rate expectations. Weekend reports suggest a UK-EU trade deal could still be secured, while it was also reported the UK Chancellor warned PM Johnson against the adverse consequences of a no deal. Negotiators begin their final round of negotiations ahead of the October 15 EU leaders’ summit.

In BoE news, Deputy Governor Ramsden hosed down the possibility of negative rates in the near term, lining up with Governor Bailey and suggestive of the staff at the BoE being against negative rates. Deputy Governor Ramsden said “I see the effective lower bound still at 0.1 which is where Bank Rate is at present” and on negative rates “we are not about to use them imminently. It will take time to do this work”. The comments follow external MPC member Tenreyo who saw “encouraging” evidence for negative rates, citing on the weekend that “there has been almost full pass-through of negative rates into lending rates in most countries” and that “banks adapted well – their profitability increased with negative rates”.

On GBP though, we are mindful of the prospect of a harder lockdown in Northern England and London to combat the recent surge in the virus. The Times yesterday reported “Ministers are preparing to enforce a total social lockdown across much of northern Britain and potentially London to combat a spiralling second wave of coronavirus. Under the new emergency plan, all pubs, restaurants and bars would be ordered to shut for two weeks initially. Households would also be banned indefinitely from meeting each other in any indoor location where they were not already under the order. Schools would stay open as well as shops, factories and offices at which staff could not work from home.” Should a harder lockdown be announced, it is likely GBP would come under pressure

The AUD also outperformed overnight, +0.6% to 0.7072. There has been some paring back of a rate cut occurring as soon as October, with November now looking more likely. Yesterday Westpac moved their call to November from October, which did see the AUD pop higher. NAB’s view remains a rate cut in either October or November, though November is looking more likely given the backgrounding of journalists who say the RBA wants to see the contents of the October 6 Budget, as well as not wanting to steal the limelight from the Budget.

Not market moving, but also in the background for Australia was Victoria recording just 5 virus cases yesterday. The 14-day moving average for Metro Melbourne is 20.3 and for Regional Victoria is 0.6. Note the third step of re-opening which would see most industries reopen in Melbourne requires the 14-day average to fall to less than 5 a day. A more comprehensive re-opening however does not occur until there are no new cases for 14 days. Pressure continues to mount for Victoria to re-open more quickly given virus counts in the single digits should make track and trace more effective as it is in NSW and QLD.

Newsflow and data was quiet with little in the way of market reaction from either. The Dallas Fed Manufacturing Index rose more than expected (13.6 v 9.5 expected and 8 previously). Trawling through the anecdotes reveals the election uncertainty could weigh on sentiment going forward and that for some in the business sector, a Trump re-election would be favourable (“Election uncertainty, a Congress that is essentially deadlocked from approving another relief package, no infrastructure package and overall weak demand from many of our customers continue to put manufacturers in a state of uncertainty”; another survey participant said “We are bidding new projects that are being held up, we believe, until the outcome of the elections. A Trump win will cause our business to boom.” Either way the rise in the Dallas Fed Measure, suggests the ISM Manufacturing Index should rise on Thursday (consensus is little changed at 56.4 from 56.0).

Yields were also little moved with the US 10yr -0.2bps to 0.65%.

Finally, and ahead of today’s Trump v Biden Presidential Debate, the NY Times reported yesterday that President Trump paid barely any federal income tax over the past 18 years and just $750 in 2016 and in 2017. Regardless of your own personal views of Trump, the risk is that it is another factor that could weigh on swing voters. No doubt it will be feature of tonight’s debate.

A quiet day domestically with only Weekly Consumer Confidence. Offshore the first US Presidential Debate will be a key focal point, while various CPI measures in Japan and Germany are expected to show outright deflation and adding to views that the COVID-19 shock is overwhelmingly disinflationary. For more details, please see below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.