Online retail sales growth slowed in May following a fairly strong April

Insight

Those vaccine hopes continue today, even though there were warnings from Fed officials that the economy still faced ongoing impacts from COVID-19, with structural differences highlighting the need for the fiscal stimulus that now seems unlikely to happen this year.

Today’s podcast

https://soundcloud.com/user-291029717/tech-hit-by-vaccine-and-antitrust-moves-rbnz-today-less-dovish-perhaps?in=user-291029717/sets/the-morning-call

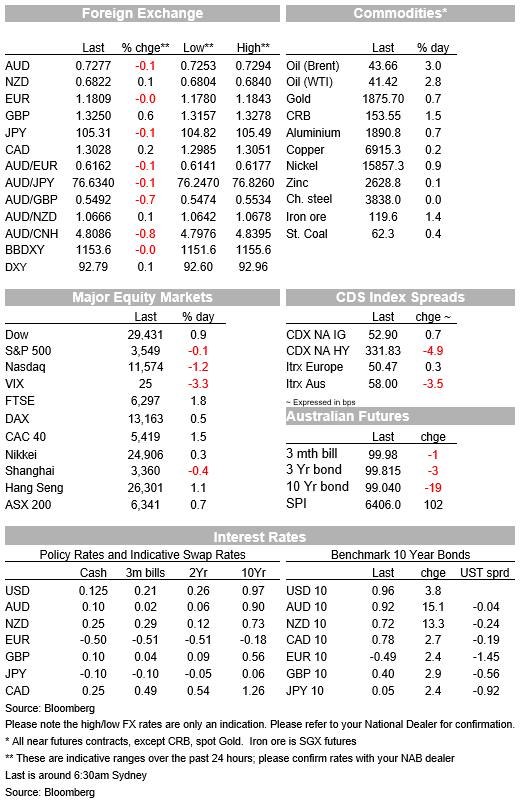

It has been a mixed night for equities although small cap can claim a small victory, outperforming for a second day in a row. Yesterday’s positive vaccine news is one factor still at play while big tech is also under pressure from antitrust rules in Europe. Core global yields have edged up again with 10y UST yields now trading at 0.96%. Quiet night for FX, AUD little changed at 0.7286, NZD back above 68c ahead of RBNZ today and EUR shows little reaction to EU news agreement on long term funding, a positive step for ratification of Recovery fund.

European equity had another good night with major regional indices closing with gain between 0.5% to 1.79%. the STX Euro 600 index closed the day 0.90% higher with energy and financial sectors leading the gains while IT was the underperformer down 2.10%. A look at the main US equity indices depicts a similar picture, the tech heavy NASDAQ is down around 1.25% the S&P is close to flat (-0.15%) while the Dow ( an industrial index) is up 0.84%. That said the big winners in the US are small caps, with the Russel 2000 up 1.89%, adding to yesterday’s 3.7% gain.

A rotation theme remains evident in equity markets. Yesterday’s great vaccines news from Pfizer and BioNtech has triggered a reassessment of the outlook for next year. Big tech which has benefited from our virus driven change in behaviour (working from home a primary example) is now falling out of favour while small cap stocks and those that have been most affected by social distancing restrictions have outperformed. Big tech companies have also come under pressure following overnight news that the EU has accused Amazon of breaching anitrust rules over its use of rival’s sales data on its marketplace that could benefit the company’s own retail arm. The EU Commission will also investigate how Amazon picks products for a prominent “buy box” that drives sales and may push retailers to use its own logistics and delivery services. Meanwhile Alibaba has remained under pressure ( down 9% overnight) following the release of a new draft anti-monopoly rules by the Chinese regulator.

The positive vaccines news from Pfizer and BioNtech appears to be overshadowing the concerning increase in COVID-19 infections. On this score, Fed Kaplan was speaking overnight and while he noted the US economy was likely to have a strong recovery from the pandemic-induced slump in the second half of the 2021, he also warned that because of the resurgence in COVID-19 infections the US economy has “a couple of difficult quarters” to deal with first. Kaplan also repeated the Fed Chari Powell’s message that additional fiscal policy support would be helpful, especially for unemployed workers and small businesses that need support to survive the next few months.

For now, it seems that markets are looking beyond the next couple of quarters with core global yields also looking at the potential for the global economic recovery to become broader and stronger next year. Core global yields have edge up a little bit more overnight as investors price a better growth outlook and less need for further monetary support. . The 10-year Treasury yield is 3bps higher overnight, at 0.96%, which is near its highest level since June. Yield curves are steepening, with central banks still expected to keep cash rates on hold for several years. The 2y10y US yield curve steepened 1.5bps overnight, to 78bps, its steepest level since early-2018.

The USD is little changed in index terms and in G10 GBP has been the outperformer, up 0.64% to 1.3252. Overnight the UK labour data was underwhelming with unemployment rising to 4.8% in September from 4.5% in August so gains in the pound are difficult to justify, there has also been no major developments on the UK and EU trade negotiations. The Euro is little changed at 1.1809, despite positive news from Europe’s long term budget plans. Bloomberg noted that European Union negotiators reached a deal on the bloc’s long-term spending plans, moving a step closer to finalizing its landmark 1.8 trillion-euro ($2 trillion) budget and stimulus accord. This is an important step that paves the way for the EU recovery fund to be ratified next month.

The AUD is little changed relative to yesterday’s levels, currently trading at 0.7278. NZD is a little bit perkier, up 0.14% and trading back above the 68c mark ahead of the RBNZ later today. Our BNZ Colleague, Nick Smyth noted that there were big moves in the NZ rates market yesterday, with the market recalibrating its OCR expectations after the positive vaccine news from Pfizer. OIS pricing for the February meeting shifted up 5bps, to 0.19%, April by 6bps, to 0.05%, while the terminal OCR moved up to -0.11%. For context, the terminal OCR was priced to be almost -0.25% only a week ago. The market clearly sees the positive vaccine news, in combination with the booming NZ housing market and resilient economy to date, as having reduced the chances that the RBNZ will need to resort to a negative OCR next year.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.