Online retail sales growth slowed in May following a fairly strong April

Insight

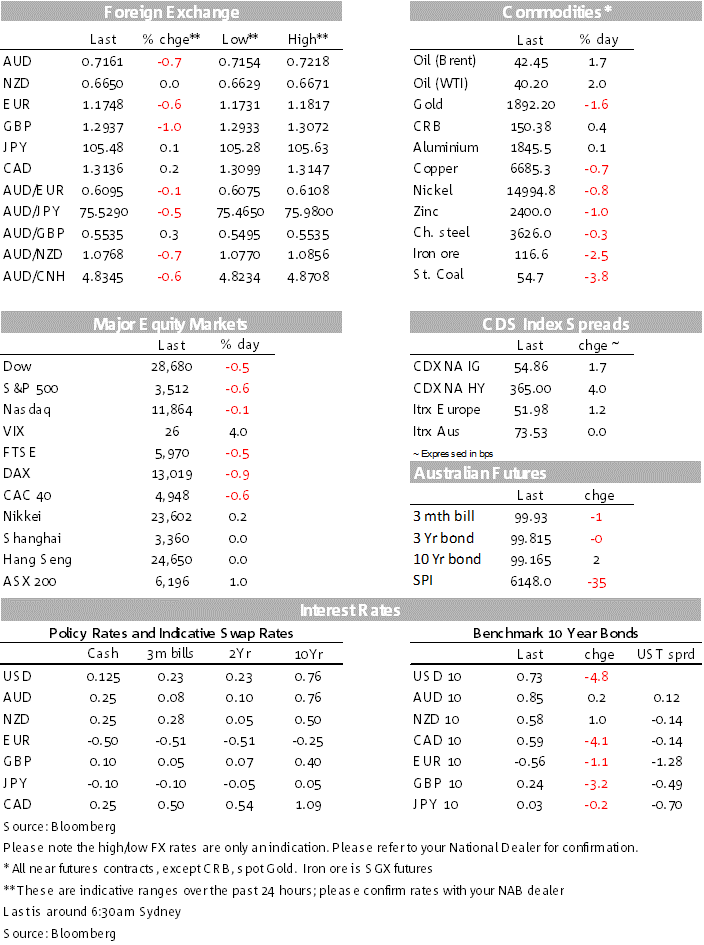

The Aussie dollar has taken a hit twice in the last twenty-four hours.

https://soundcloud.com/user-291029717/the-aussie-coal-ban-and-earnings-caution?in=user-291029717/sets/the-morning-call

Well, I won’t back down. No, I won’t back down

You can stand me up at the gates of hell. But I won’t back down – Tom Petty and The Heartbreakers

A combination of underwhelming company specific news, pausing of COVID-19 trials and no backing down in the US stimulus impasse have contributed to a souring in sentiment over the past 24 hours. The USD and UST yields have benefited from a safe haven bid, AUD is amongst the big underperformers down 0.75% to 0.7159 amid increasing concerns over China’s coal ban while the euro and pound have been affected by a lack of progress in UK-EU trade negotiations.

Talks are still going nowhere dimming the prospect of a new round of support this side of the election. This is a three way negotiation, the White House is negotiating with House Speaker Pelosi and while there had been some hopes of a compromise following the increase in the stimulus proposal by the Trump administration to $1,8trn, vs Democrats $2.2trn plan. Pelosi noted overnight that “Tragically, the Trump proposal falls significantly short of what this pandemic and deep recession demand,”. The House Speaker called for significant changes to remedy the White House proposal. Encouragingly Pelosi and Treasury Secretary Mnuchin plan to continue their discussion.

Meanwhile on the other extreme we have the frugal Senate Republicans led by McConnell stubbornly unmoved on their position for a smaller spending plan. MCConnell was aiming for a proposal to vote next week on just one provision – replenishing funds in the Paycheck Protection Program for small businesses. Unsurprisingly, Pelosi quickly rejected the idea as a non-starter arguing that Democratic priorities would be cut in any deal based on such an agreement. MCConnell’s proposal also triggered a rebuffing tweet by President Trump “Go big or go home!!”.

So for now it is hard to see a deal being agreed before November 3, the market is still travelling with the notion that a new round of stimulus is coming, but at this stage this looks more likely after the election. A Biden win increases the prospect of a big stimulus specially if it comes with a Blue Wave while a Trump win suggesst a stimulus package is likely to be smaller amid the prospect of a still divided Congress.

Better than expected trading revenues and earnings by JPM and Citi kick-started the US earnings reporting season, but the fill good vibes were short lived. Sentiment took a turn for the worst after investors delved into the details of the reports. JPM shares fell ( now -2.43%) after the bank said its surprisingly-good reserve release didn’t reflect a better view of the economy adding that substantial reserve releases may yet come given that there is “a lot of uncertainty around whether this can occur (i.e. it will require further progress against Covid, more fiscal stimulus, etc.),”. Citi shares declined (-4.27%) after the bank reported a jump in costs and warned it now expects a slower economic recovery.

Given the above Financials (-1.67%) have led the decline in the S&P 500 (-0.60%). Apple shares have also struggled (2.56%) following the release of the new Iphone 12, although shares had recent in recent days ahead of the overnight announcement. Worth noting too that lead from yesterday’s APAC trading was also a soft one. After futures fell during Asian trading following a report that Johnson and Johnson had temporarily halted its COVID19 vaccine trial due to an unexplained illness in a trial participant. Early this morning we also learned that Eli Lilly antibody trial is paused because of potential safety concerns. The Eli Lilly trial was designed to test the benefits of the therapy on hundreds of people hospitalized with Covid-19, compared with a placebo. A pause in these trials is not unusual as we saw earlier with AstraZeneca’s trial, which eventually resumed in countries outside the US.

The souring turn in equity sentiment overnight has contributed to an increase in safe haven demand for the USD. In index terms the USD is up 0.47% in DXY (at 93.5) and by a similar amount in BBDXY now trading at 1168.889. Looking at G10, the USD is broadly stronger with NZD the only pair unchanged over the past 24 hours. Idiosyncratic stories have also played a role in some of the G10 underperformers.

Intraday chart reveals two distinctive phases in the currencies decline over the past 24 hours. Yesterday the AUD came under pressure falling from 0.7210 to around 0.7170. After weekend news that coal buyers in China had been verbally told to cease buying Australian coal for the time being (both thermal and metallurgical), the Australian government sought clarification of the ban from Beijing. It was speculated that the ban was politically motivated after the recent escalation in tensions between Australia and China, but an FT article reported analysts comments that the ban most likely reflected quota limits being reached, designed to protect China’s coal sector.

The FT article only provided a small reprieved to the AUD, as market sentiment took a turn for the worst overnight the AUD continued to decline. The AUD is down 0.7% over the past 24 hours, and now trades at 0.7159, 9 pips above its overnight low. Meanwhile the NZD has been supported, perhaps reflecting AUD/NZD cross selling, trading little changed at 0.6649 against a backdrop of broadly-based USD strength. AUD/NZD is down almost one big figure over the past 24 hours and now trades at 1.0768.

Down 0.98% to 1.2937 and euro to a lesser extent down 0.58% to 1.1746. UK EU trade negotiations are making very slow progress with EU negotiator Michel Barnier said the talks haven’t sufficiently advanced for them to enter the so-called tunnel, the intensive final phase, according to officials close to the discussion. Meanwhile UK negotiators noted that they are “ready and willing” to leave without a trade accord. Encouragingly talks are expected to continue today and given the mounting pressure the UK government is under from all sides right now (having successfully pleased no one with the latest COVID measures) it would be a brave PM who decides that’s it for the talks at this stage, when the EU is prepared to carry on negotiating.

The US Treasuries also benefited from a safe haven bid with the curve bull flattening as the 30y Bond declined by 7bps to 1.5070% and the 10y Note declined by 5bps to 0.7250%. The US core CPI rose by 1.7% y/y, meeting expectations, with the index still being affected by the impact of COVID19. Rents, which make up 24% of the index rose 2.5% y/y, their slowest pace in over six years and these will likely act as a drag on inflation for some time yet.

Wrapping up with some economic news, the IMF upgraded its global growth forecasts, seeing GDP now shrink by “only” 4.4% this year compared to the minus 5.2% projected in June. The shallower recession means a slightly weaker rebound, with growth next year projected at 5.2% (previously 5.4%). The Chief Economist described the recovery as a “long, uneven and uncertain ascent”.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.