Total spending grew 0.9% in June.

The Fed has kept rates on hold but have kept the door wide open for future rate cuts.

https://soundcloud.com/user-291029717/the-fed-lowe-boj-and-bojo?in=user-291029717/sets/the-morning-call

I’m not prepared to go on like this, I can’t, I can’t, I can’t stand losing …you- The Police

Early this morning the FOMC delivered a pleasing outcome for markets, shifting it patient policy stance to a clear easing bias. Markets were marking time ahead of the meeting, but reaction to the FOMC has resulted in a broad uplift in US equities, a decent bull steepening in the UST curve and broad USD weakness. The latter however hardly yielded any benefits to the AUD and NZD.

The Fed is losing its patience, but not its data dependency mantra. The FOMC left the funds rates unchanged (unsurprisingly Fed Bullard was a dissenter, the first under Powell’s stewardship), but it also signal for the first time since mid-2007, its willingness to ease potentially as soon as July. The new median dot plot, which projects the future Fed funds rate path based on officials’ forecasts, shows no change in policy this year, but only just given that 8 out of 17 members projected a rate cut before the end of 2019 (seven with -50 bps and one with -25 bps). The median dot for 2020 shows a 25bps decline and the longer run median dot also declined 25bps to 2.50% (reflecting a 25bps hike in 2021). As for the economic forecast, the most notable change was the decline in the 2019 core PCE inflation number which is now seen at 1.8% rather than 2%. The latter plays into the view what was previously thought to be transitory downward pressures on inflation, now appears to be having a longer lasting impact.

As expected the Statement lost the word “patient” and while the base case scenario remains that “The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective”, uncertainties about this outlook have increased. Looking ahead the Committee will closely monitor the incoming data and do what is needed in order to sustain the current economic expansion

At the press conference, Fed Chari Powell emphasised the message that downside risks have increased since the last FOMC meeting, thus the probability that more monetary accommodation may be needed has also risen. Key underlying message is that these new uncertainties are largely trade tensions and slower global growth while on the domestic front the not so new uncertainty of muted inflation is still a concern. Notably too Fed Chair Powell also drew attention to the fact that even those officials that did not project easing in their dots, generally saw the case for more accommodation as having strengthened.

So although the Fed partiality has shifted from a wait and see mode to an easing bias, the fact that trade uncertainty and its impact on global growth has been the main catalyst for its change in stance, means that a new round of Fed easing is largely contingent on the outcomes from upcoming G20 meeting between President Trump and Xi. For now though, the change in the Fed’s bias has encouraged the market to increase its expectations that a new round of easing is just around the corner. A July cut is now more than fully priced and the market now sees 70bps of cuts this year, compared to 59bps priced as of yesterday. This pricing of almost 3 rate cuts before year end looks very aggressive if one considers the fact that yesterday President Trump confirmed he will be having an extended meeting with President Xi at the G20 and that trade representatives from both countries are back at the negotiating table.

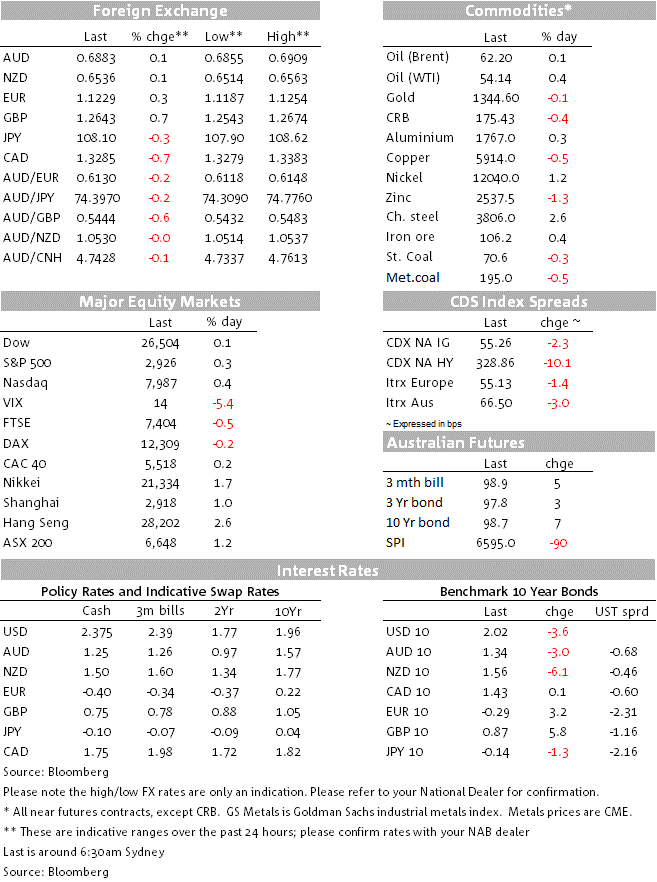

After initially trading in and out of positive territory, US equity markets have closed the day with modest gains between 0.15% and 0.42%, reflecting a small post FOMC uplifts. Moves in UST yields has been more significant with a bull steepening in the curve driven by a 12.2bps decline in the 2y rate to 1.744% while the 10y rate fell 3.1bps to 2.02%, ending session close its intraday low but abovge the 2.0148% low recorded post Draghi’s speech yesterday.

The USD was drifting lower ahead of the FOMC, but the move gathered momentum post. In index terms the US is down about 0.4% against both majors ( DXY -0.39 to 97.254 and BBDXY -0.42% to 1197) and EM ( EMCI +0.45%). Notably against Asian currencies the USD is little changed ( ADXY +0.05%). Both antipodean currencies jumped on the FOMC announcement, but these initial gains faded shortly after. AUD briefly traded to an overnight high of 0.6909, but now is back at 0.6881, essentially at the same place where it was this time yesterday. The Kiwi traded to an overnight high of 0.6563, but now trades at 0.6538, up 0.11% over the past 24hrs.

GBP has been one of the best performer, with gains ahead of the FOMC statement. Boris Johnson extended his lead in his bid to become the next UK PM, winning nearly three times as many votes as the runner-up in the latest round of voting amongst Conservative MPs. The dominant performance by Johnson is now seeing an increasing number of Conservatives calling for an early election, as many now believe that if Johnson becomes PM, the Conservatives can win an outright majority in Parliament if a new election was triggered. On the data front, UK core CPI inflation slipped to 1.7% y/y but was a little stronger than market expectations. GBP is currently up 0.7% to 1.2643 with CAD the other outperformer, up 0.73% (USDCAD now at 1.3285). Headline CPI in Canada was stronger than expected, but the key core-common measure that the BoC focuses on was steady at 1.8% and slightly below market expectations

Moves in commodities have been rather muted, oil prices are a tad stronger, copper eased a little bit and iron are edge up another 0.4% to close the day at 106.2

Our BNZ colleagues expect GDP to show growth of 0.6% q/q/2.4% y/y in Q1, which exceeds the RBNZ’s forecast 0.4%/2.2% given strength in construction and exports. That said, they also expect the data to reveal some underlying weakness, which is something they will be bearing in mind for Q2/Q3 GDP

We see some risk that the Governor Lowe may signals a July rate cut, however we also think it is more likely that the Governor could use the speech to pave the way for rates to eventually head below 1% in order to reduce the unemployment rate towards NAIRU which is now seen at 4.5%. While a close call between July and August, NAB economists still think it is more likely that the Board will deliver the next rate cut in August when it has an updated set of forecasts.

We expect the Bank to stand pat today, but similar to the Draghi’s Sintra speech, we also anticipate the BoJ to acknowledge the increase in downside risks to the economic outlook. In line with a recent speech, early in June, we think Governor Kuroda will yet again emphasise the message that the BoJ still has the ability to ease further, if required, citing four policy options: cutting the -0.1% negative rate further, lowering the 10y JGB yield target, increasing the monetary base or boosting asset purchases.

We expect the BoE to repeat its message that if a soft Brexit is achieved, UK rates will need to rise slightly over the coming years

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.