Kicking the tariff can down the road

Insight

Markets are more preoccupied with the outcome of the US-China trade talks this week.

https://soundcloud.com/user-291029717/the-waiting-games-trade-brexit-and-syria?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s Market Research support please let your company’s representative know.

A quiet start to the week with markets cautious ahead of the upcoming US-China talks scheduled for Thursday and Friday. China has already stated it is only aiming for a partial deal with the Commerce Ministry confirming earlier weekend reports that China wouldn’t include commitments on reforming industrial policies or government subsides. Instead the Commerce Ministry has said it is prepared to set out a timetable for the harder issues to be worked out next year. That of course robs President Trump of his aims for a broad deal that would be 100% for the US and the Administration remains divided on whether to accept a partial deal. In the words of that Barbadian songstress Rihanna, “nothing is promise…ain’t none of this certain” It seems the best we can hope for this week is for a truce to continue and for Trump to extend the deadline for the next lift in tariffs (scheduled for 15 October Tariff increase from 25% to 30% on $250bn of Chinese imports).

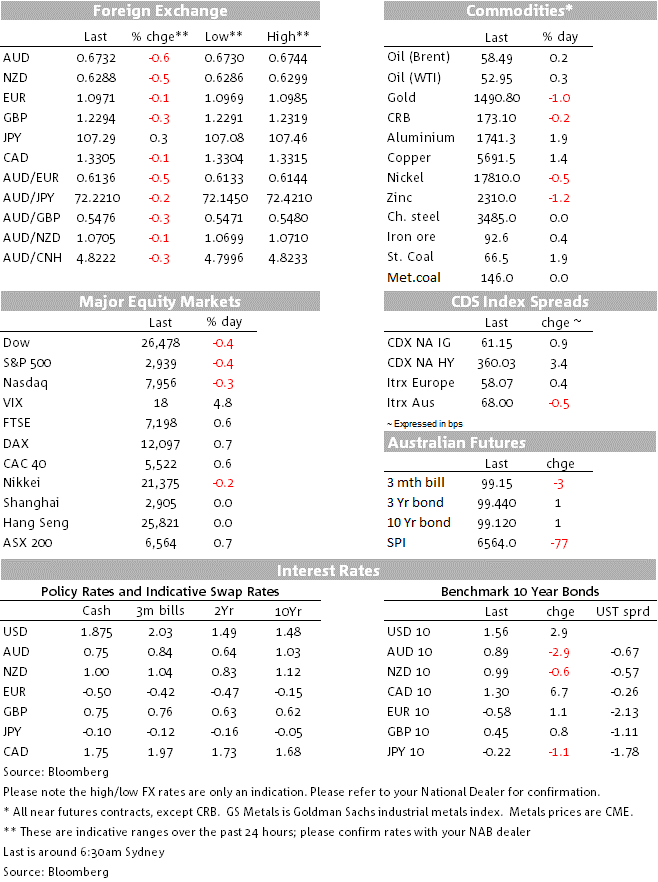

Reduced hopes for a deal saw USD/CNH pop higher, +0.3% to 7.1321, while trade-sensitive currencies fell with AUD -0.6% to 0.6733 and NZD -0.5% to 6289. The biggest G10 mover though was SEK (EUR/SEK +0.7% to 10.88), being buffeted by both dimming trade hopes and a sharp falls in industrial production in Norway. Despite those moves the USD (DXY) is up a more measured +0.2% with EUR broadly steady at 1.0973 and USD/JPY +0.3% to 107.31. In rates, yields are little moved with US 10yr yields +2.7bps to 1.56%, while equities are softer with the S&P500 -0.4% to 2,941. After Payrolls on Friday Fed Funds pricing now points to around a 60% chance of an October rate cut, though a rate cut is more than fully priced by the end of the year (128% priced, and 3 cuts priced by mid-2021).

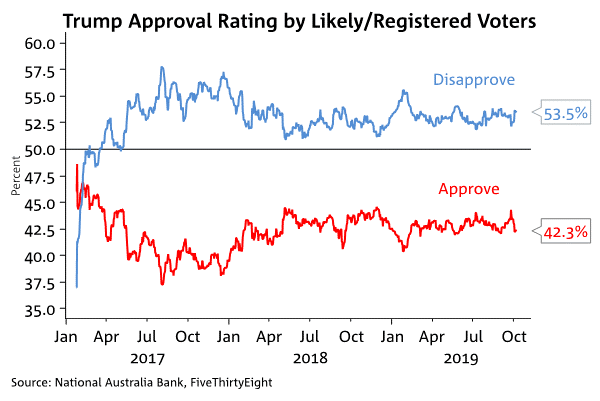

With trade talks the major focal point of the week, Trump’s polling is coming under the spotlight (and combined with the state of the US economy will help dictate the likelihood of a deal, as well as the impact of the impeachment inquiry currently underway). Latest polls suggest Trump’s approval rating has declined, though at 42.3% is still around average levels for his presidency (Chart below). Polls focused on the agricultural heartland of the mid-west though due suggest he is behind Democratic challengers. Payrolls on Friday also suggest the US economy overall remains resilient to trade headwinds, though the ISMs due warn that the uncertainty will likely drag on growth with trend payrolls growth to slow.

Economic data has been sparse, though German Factory Orders fell more than expected in August and pointing to a protracted slowdown. Orders were -0.6% m/m against expectations of -0.3% with orders now at an annualised -6.7% y/y. Interestingly, the details of the report suggests the weakness now is coming from the domestic economy with a -2.6% m/m fall in domestic orders with weakness in consumer goods – and overall suggesting the weakness in the manufacturing sector is being felt in the non-manufacturing sector. Export orders were slightly higher, +0.9% m/m – though it is too early to tell whether this is pointing to a stabilisation in export demand. Separately released Eurozone Sentix Investor Confidence was also weaker than expected at -16.8 against -13.0 expected, suggesting recent ECB policy stimulus has done little to lift confidence in Europe. The weak data initially weighed on EUR, though has been largely unwound with EUR little changed at 1.0972 this morning.

Turkey’s Lira has weakened by more than 2% (USD/TRY +2.6% to 5.84) after a major policy shift by the US government. The White House has said it would stand aside and allow Turkey to engage in Northern Syria, where the formally US backed Kurdish Militias are. However, Trump also cautioned that “…if Turkey does anything that I, in my great and unmatched wisdom, consider to be off limits, I will totally destroy and obliterate the Economy of Turkey (I’ve done before!)”.

In terms of today, it is a relatively quiet day domestically with the NAB Business Survey and ANZ Job Ads the main highlights. Focus then shifts internationally with the China Caixin Services PMI and then to the US for the NFIB Small Business Survey and remarks by Fed Chair Powell:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Kicking the tariff can down the road

Insight

Total spending grew 0.9% in June.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.