Total spending grew 0.9% in June.

The market continues to adjust to the expectation that the US-China trade spat won’t disappear in a hurry.

https://soundcloud.com/user-291029717/trade-battles-on-many-fronts-drives-further-uncertainty?in=user-291029717/sets/the-morning-call

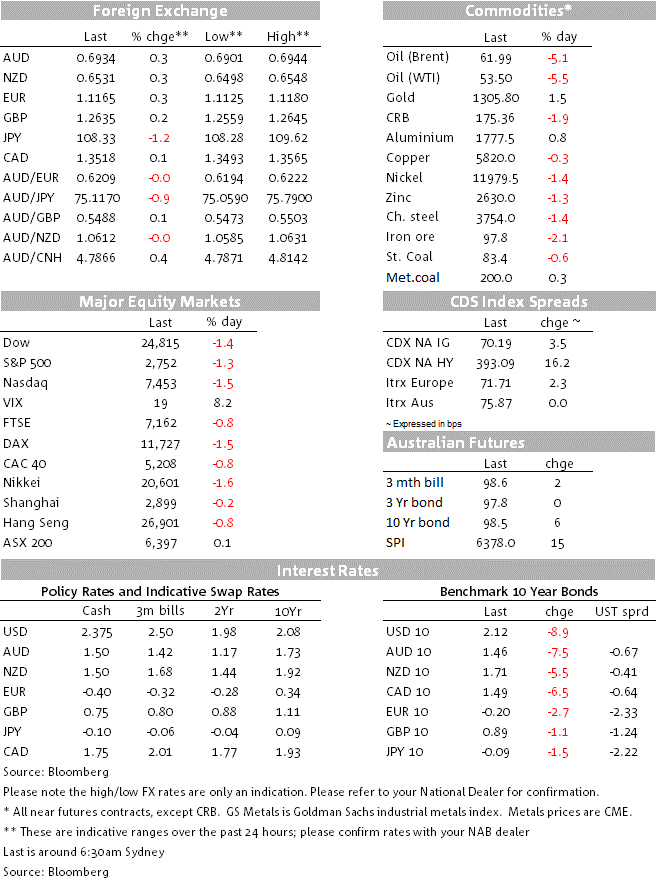

It all started south of the border (down Mexico way), after Friday’s announcement that the US administration intended to impose a 5% tariff on all Mexican imports (effective June 10) climbing to 25% in October if Mexico doesn’t curtail the flow of illegal immigrants. The news provided further fuel to investors’ concerns over the potential of a global growth slowdown amid heightening US led trade tensions. Equity markets took a bath on Friday culminating a torrid month of negative returns, UST yields led the rally in core global yields, safe haven demand on factor while a repricing of Fed rate cut expectations saw the front end of the curve lead the move lower in yields. Lower UST yields hurt the big dollar – JPY followed by CHF the big beneficiaries. Oil prices headed the decline in commodity prices while gold outperformed. Over the weekend, the Trump administration ended special trade treatment for India, China announced intentions to compile a list of “unreliable” foreign companies with FedEx under investigation and back in the US the Justice Department was reported to be preparing an antitrust investigation into Alphabet Inc., Google ‘s parent company.

It’s gettin’ hot in herre (so hot)!! The US move on Mexico has raised a few alarms as the decision shows President Trump willingness to use tariffs as leverage on issues transcending economic tensions. This of course is an additional concern to the impact more tariffs will have on global trade alongside global supply disruptions. Mexico is the US 3rd largest goods trading partner with trade between the two nations estimated to be just over $600bn worth with cars and auto parts representing a significant portion of this figure. India is now also involved in the broadening US led trade war with the US administration announcing its intension to end the country’s special trade treatment. As of June 5th India will no longer be regarded as a developing country, effectively cancelling the tariff exemption for Indian products worth billions of dollars. This comes after the US dissatisfaction with India’s lack of provision for reasonable and equitable access to its markets.

After a volatile month of May for markets, the start of June is unlikely to offer a reprieve as the broadening in US tariff scope over the weekend will have many wondering whether auto exporting countries could be next in the line of fire. Many commentators over the weekend are also suggesting that NATO countries could be next given their failure to increase their military spending. Germany would be concern on both accounts.

Not to be undone by the news, China released a white paper on trade expressing willingness to work with the US to find a solution, but it also noted that a strategy of maximum pressure and escalation will not work with China. Wang Shouwen, China’s Vice Commerce Minister said that China doesn’t want a trade war with the U.S. but it is “not afraid to fight one if necessary”. Also over the weekend, China confirmed its plans to setup a list of “unreliable ” foreign companies that could be hurting “the legitimate rights and interests” of Chinese companies. FedEX is top of the list with China announcing the company is under investigation because it seemingly violated Chinese laws and regulations by misdirecting packages. Hopes for de-escalation in US-China trade tensions look to be diminishing by the day while the increase in nationalistic rethoric is also making it less likely that both President Xi and Trump and can find a way to settle their differences at the G20 meeting late in June.

Given the above major global equity indices had a torrid end to May and the start of June is unlikely get any better. US indices fell more than 1% on Friday and ended more than 6.5% lower for the month. The Stoxx Europe 600 lost 5.7% during the month after falling 0.81% on Friday and in Asia the Hang Seng fell more than 9% in May, while the Shanghai Composite lost 5.8%. News that the US Justice department has opened an antitrust investigation on Alphabet ( Google’s parent company) is unlikely to help sentiment at the start of the week.

Safe haven demand and a repricing of Fed rate cut expectations saw UST yields lead the rally within core global yields. 2y UST yields fell 13.8bps on Friday to 1.92% and the 5y tenor also fell below 2% to 1.912%. The 2y10y curve had a mild steepening bias as the 10y rate fell by “just” 9bps to 2.12%. Meanwhile in Europe, 10y bunds fell 2.7bps to a new record low of -0.21%. On Friday, German retail sales fell 2% in April vs expectations for a small rise of 0.1% and the country’s latest read on inflation also disappointed (+1.3% v 1.4% exp.) printing its lowest number in over a year. Finishing the trifecta, the leader of the SPD resigned on Sunday, raising the risk that the SPD may quit Merkel’s coalition triggering fresh elections.

Moving on to currencies, the move lower in yield weighted on the big dollar with a repricing in Fed expectations now seen the chances of a 25bps rate cut fully priced by September while a cumulative 54.3bps of cuts are now expected by December. After trading to a high of 98.273 on Thursday, the DXY index ended the week at 97.759 (-0.40%). Similarly BBDXY traded to an intraday high of 1212.7 (-0.13%), before ending the day at 1207.39.

JPY was the big beneficiary from the safe haven demand with USD/JPY finally making a decisive break below the ¥109 mark. The break lower in the Nikkei (-1.63%) alongside gains in gold helped the USD/JPY move lower and now many will be looking if the move can extend below ¥108, opening the door for a move towards ¥105.

Somewhat surprisingly given the broad risk of tone in equities and core yields, both the AUD (+0.35%) and NZD (0.31%) managed to outperformed the USD on Friday with the antipodean currencies ending the week at 0.6938 and 0.6531. Both have opened the new week a little bit lower and the prospect of further risk aversion suggest the AUD and NZD are likely face some downward pressures given their risk sensitive nature. Its PMI day today with China Caixin and EU PMIs the highlights ahead of US ISM tonight

Oil prices led the decline in commodities on Friday, reflecting a repricing across the whole sector as the market readjust expectations for global growth. Brent and WTI closed just under 4% lower on the day while meatls werew down around 1%. Gold and Zinc were the exception up just under 1%.

NAB’s headline ISM model points to a 54.3 read, higher than the current market consensus of 53.0 and up from April’s 52.8, but still well down from what it averaged in 2018.Driving the rebound in our model is the mild uptick in the NY Empire, Philly Fed and Chicago PMI, while other regional surveys were mostly flat to lower.

AU RBA meeting, Lowe speech, Q1 GDP and retail sales; NZ GDP partials; US-CH trade talks; ECB meets; UK politics

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.