NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The markets have done a complete u-turn overnight on the back of positive news on the US China trade talks and some wins from the G7 summit, including proposals to reform WTO rules and a potential US Iran meeting.

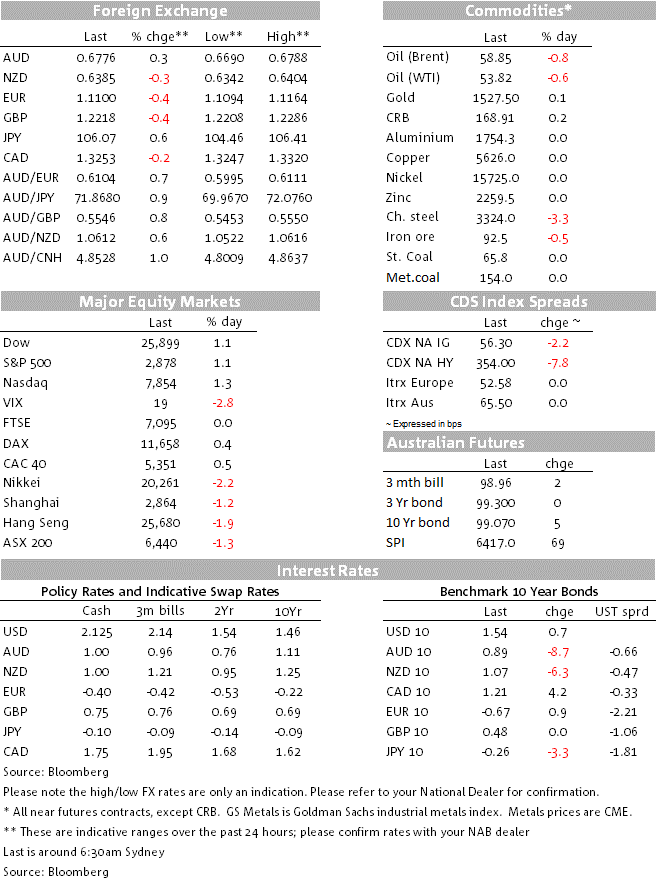

Risk sentiment recovered after a weak Asian open on the back of comments by President Trump and Chinese Vice-Premier Liu that were later bolstered by what seemed to be a productive G-7 meeting. The veracity of Trump’s comments though were later questioned as Chinese officials and press said “top negotiators didn’t hold phone talks in recent talks”, though as veteran market commenter Jim Cramer notes: “really doesn’t matter…in the end we’re doubting a guy that didn’t want the market to crash and that’s a dangerous thing to take on”. The confusion is inspiration for today’s title, “We No Speak Americano” by Yolanda Be Cool and DCUP. US stocks rose sharply shaking off the large falls seen in Asia with the S&P500 +1.1% to 2,878 (note Nikkei was -2.2% and ASX200 -1.3%). With better risk sentiment EUR lost some of its gloss -0.4% (to 1.11), along with USD/Yen +0.6% (to 106.07) with the USD (DXY) up some 0.6%. Yields fully retraced their lows seen in Asia with US 10yrs making a trip from 1.54 to 1.44 and back and currently trades at 1.5351%.

First to the overnight comments that boosted sentiment. President Trump indicated that China called the US trade team “twice” over the weekend and that China wants to “make a deal”. Those comments saw US yields spike 6bps higher in futures trading off their lows. However, those comments were later disputed by the Chinese Foreign Ministry and by the Editor of the Global Times (a known link to Beijing) who said: “Based on what I know, Chinese and US top negotiators didn’t hold phone talks in recent days. The two sides have been keeping contact at technical level, it doesn’t have significance that President Trump suggested. China didn’t change its position. China won’t cave to US pressure”. As we have been highlighting for some time, President Trump’s continued escalation of tensions gives little room for China (or indeed the US) to compromise without losing face, which makes a deal less likely in the near term. While Chinese Vice-Premier Liu also made some conciliatory comments overnight, those comments were no different to what officials have been saying for months and in your scribe’s view shouldn’t be taken as a sign of softening from the Chinese side.

Nevertheless, for markets they have latched onto the headlines as a sign that US-China tensions are unlikely to escalate further, and as evidence that President Trump is sensitive to stocks. Or in the words of veteran market commentator Jim Cramer: “really doesn’t matter…in the end we’re doubting a guy that didn’t want the market to crash and that’s a dangerous thing to take on”. The S&P500 has closed 1.1% higher, a sharp reversal after futures were pointing to a 1.1% decline in Asia. Later in the session, a favourable court ruling on J&J related to lower than expected Opioid penalty (an Oklahoma judge ordered J&J to pay $572m) saw the S&P500 Health Care Index bounce strongly.

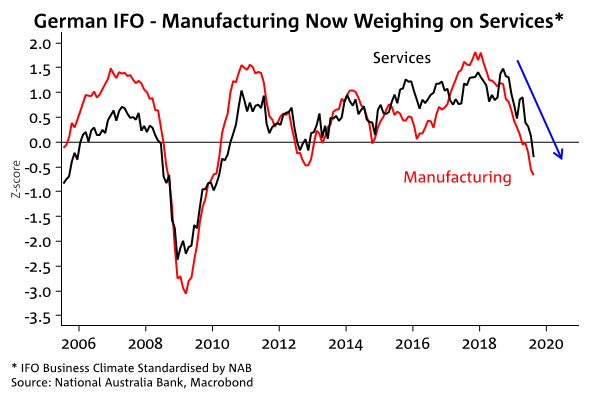

Worryingly for the global economy, the German IFO came in below expectations with the IFO Institute noting that it adds to the many indicators of a recession being likely in Germany. In terms of details the IFO fell to 94.3 from 95.8 and below market expectations of 95.1. The Manufacturing Index is now at its weakest since December 2009, while the downturn in the manufacturing sector is increasingly weighing on the services sector with the Services Index the weakest since June 2010 (see chart below). EUR fell in reaction with EUR -0.4% to 1.1100. Weak German conditions will likely see renewed calls for fiscal stimulus, while a substantial ECB stimulus package in September is all but assured.

FX moves followed usual risk-on sentiment with USD/YEN higher +0.6% to 106.07, while the market’s favourite China proxy (the AUD) rose +0.3% to 0.6776. These moves were in sharp contrast to the Asian open yesterday where USD/JPY had broken below 105 and reachedits lowest level since 2016. The EUR which had also been previously boosted by risk aversion fell -0.4%, dragged lower by the weak IFO print.

US data overnight was not market moving and was mixed overall. Durable Goods beat at the headline due to transport (2.1% m/m against 1.3% expected), but excluding transport orders fell -0.4% m/m and below the 0.0% consensus. Capital Orders were also weaker, with core capital goods -0.7% m/m against 0.1% expected. Also out overnight was the Dallas Fed Manufacturing Index which beat at the headline at +2.7 against -4.0 expected, but with a sharp decline in the Employment Index – a possible herald to the uncertainty starting to weigh on firms hiring and investment decisions.

Last night also saw the G-7 draw to a close with the conference on the whole largely successful. Trump said he was prepared to meet Iran for new nuclear talks – prospects of talks that could see Iranian oil supply return to the wider market saw oil decline overnight with Brent -0.8% to $58.85. France the US have also come to a compromise on the French technology tax with the French tax to stay in place for two years until a global minimum tax is agreed through the OECD. Encouragingly for Europe, President Trump also said he thinks the US and the EU will come to a fair trade agreement that would avoid the imposition of tariffs on cars (We’re very close to maybe making a deal with the EU because they don’t want tariffs… I think we’re going to make a deal with the EU without having to go that route).

Focus this morning will be on the RBA’s Debelle and Chinese Industrial Profits. Otherwise a mostly quiet day datawise with attention on any possible trade headlines:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.