Online retail sales growth slowed in May following a fairly strong April

Insight

Equities were mixed in the US overnight, but the S&P 500 did manage to claw out a new record high, whilst the NASDAQ fell.

https://soundcloud.com/user-291029717/treasury-yields-rise-sharply-as-reflation-rolls-on?in=user-291029717/sets/the-morning-call

All you save, And all that you give, And all that you deal, And all that you buy

…And all that’s to come, And everything under the sun is in tune

But the sun is eclipsed by the moon – Pink Floyd

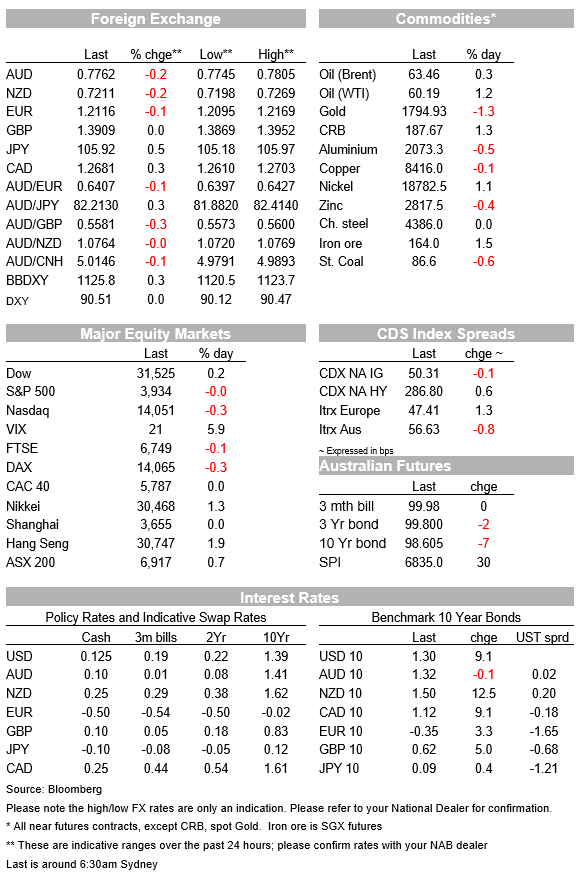

The reflation trade appears to be stepping into (another) high gear with a decent bear steepening in core yield curves,10y UST yields are leading the charge and are still climbing as I type. The S&P 500, Nasdaq and Dow temporarily eclipsed their previous record highs, before easing in the past couple of hours. The USD is broadly stronger with GBP the only outperformer, leaving commodity linked currencies and JPY at the bottom of the pile.

The main price action overnight has come from the bond market with longer dated yields leading a bear curve steepening across core markets. 10y UST yields are ripping higher and are currently attempting to sustainably trade above 1.30% (1.2989% as I type overnight high 1.3006%). The benchmark yield is up 9bps since yesterday’s Tokyo opening level and the 30y bond has climbed 7.5bps to 2.085%.

The move up in yields is also evident in the core yield in Europe with 10y Bund yields closing +3bps to -0.35%, highest since June, 10y UK Gilts +4bps to 0.61%, highest since March, while 10y BTPS rose 4bps to 0.57%, highest since February 4.

The move up in yields has been driven by increasing inflationary concerns amid a rise in energy prices along with the prospect of a big US fiscal stimulus and the global recovery entering a more solid stage as vaccine roll out lead to the reopening of economies. Overnight the Empire State Survey beat expectation by a decent margin, also playing with the reflation vibe in the market. The Empire State manufacturing index rose to 12.1 from 3.5, above the consensus, 6.0, a five-month high. Of note too, the prices paid index jump to its highest level in nearly 10 years. Much of the increase reflects the surge in oil prices, so its not really new news, nevertheless it adds ammunition to the speculation over future inflation risk.

Other factors appear to have contributed to the sell off in the bond market. The move up yields is probably making investors nervous about the 30-year Bund and 15-year Gilt sales due to take place tonight while in the US the recent rise in rates might have been exacerbated recently by mortgage-related “convexity” hedging – the higher rates go, the more hedging that needs to be done, which puts further upward pressure on rates.

US indices opened higher making new record highs in the process, but as the session went by sellers began to dominate, (higher UST yields a concern?). Now as I type the S&P 500 is flat and the NASDAQ is 0.34%. Earlier in the session, European indices closed with small losses with the Stoxx Europe 600 Index down 0.06% at the close.

The FT reported that China is exploring limiting the export of some 17 rare earth minerals that are crucial for the manufacture of American F-35 fighter jets and other sophisticated weaponry. China controls about 80% of global supply. Analysts say that a potential downside of going down this route in addition to the negative political implications, would be encouraging other nations to accelerate their own production capacities, undermining China’s dominance of the industry.

When the news broke out, the AUD and other risk sensitive currencies lost a bit of ground and the news may have played a factor in the weakness in European equity markets. Hard to tell, but this is a story keeping a close eye on.

The USD is firmer across the board with UST yields playing a supporting role. For a change, most of the rise in the 10-year rate reflected a “real” increase, with the inflation-indexed bond up just over 5bps and the break-even inflation component up just over 3bps. Higher real rates have supported the USD, with the BBDXY index up 0.4%.

Commodity linked currencies have underperformed with the AUD, down 0.24% (relative to yesterday’s NY closing levels) to 0.7763 while NZD is down 0.22% to 0.7210. NOK is down 0.57% with JPY joining the underperformers. USD/JPY is up to ¥105.91, with the pair unable to ignore the move up in 10y UST yields.

Bitcoin traded above $50,000 for the first time, continuing its strong run. The crypto currency has been buoyed by increasing acceptance of it being an “asset”, even if some remain sceptical, to which we can add ECB GC member Maklouf, who compared the investment to the 17th century Dutch tulip craze. Some believe Bitcoin to be an inflation hedge, taking the shine off gold prices, which have trended lower and slipping below USD1800 per ounce.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.