Confidence and Conditions Lift

Insight

A tweet from President Trump promising a 10% tariff on the remainder of imports from China has sent the markets into a tailspin.

https://soundcloud.com/user-291029717/trump-goes-all-the-way-on-china-tariffs

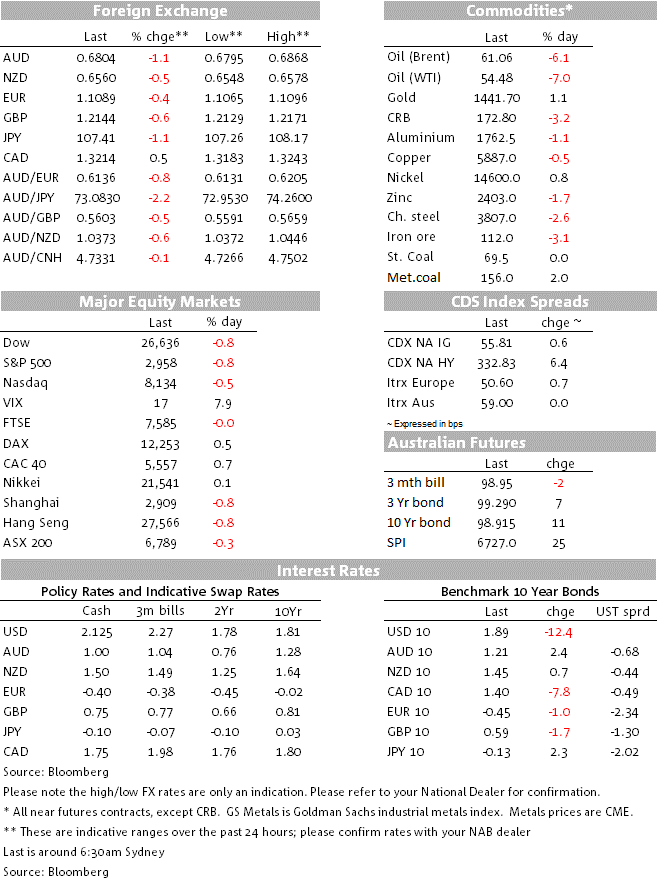

It’s all about tariffs overnight with Trump tweeting “the US will start, on September 1st, putting a small additional Tariff of 10% on the remaining $300bn of goods and products coming from China into our Country”. In a subsequent press conference Trump said the tariffs could go “well beyond” 25% and that “I can always do much more or I could do less”. Yields fell sharply in response with US 10yr yields ‑12.4bps to 1.89% and 2yr yields -14.1bps to 1.73%. Stocks sold off sharply with the S&P500 -2.0% from the peak of the overnight session. FX had typical risk aversion moves with USD/YEN -1.1% to 107.26 with China proxies taking a hit including the AUD which is -1.1% to 0.6804. AUD/JPY continues to the FX weapon of choice, down some -2.2% overnight to 73.08. Given the move in the Yen, the narrow USD DXY actually fell -0.2% to 98.37 with smaller falls in the EUR (-0.4%) and GBP (-0.6% overnight). USD/CNH moved closer the 7 level, up 0.8% to 6.9576.

It is unclear what caused Trump’s latest intensification of the trade war. Worryingly though for the global economy it appears Trump has gone all in and is hoping that China buckles under the pressure and caves to US demands. However, in such a scenario there is no way for China to fold without losing face since it goes against China’s core demands of sincerity and the removal of existing tariffs. It is possible then that China will retaliate with an intensification of non-tariff barriers, as well as further Chinese stimulus to ward off headwinds. Chinese manufacturers will also continue to squeeze their margins to offset the tariff impact which will continue to add to a subdued global inflation picture. For the Fed (and all global central banks), an intensification of the trade war will underpin fears that this could spillover to the domestic economy and puts them on the track for more “insurance cuts” and increases the probability that this could transform into a protracted easing cycle – markets price another 2 cuts by the end of the year.

Reflecting global growth fears, WTI Oil fell a sharp -7.0% to $54.48. Lower oil prices and the possibility of growth headwinds to demand has also seen inflation pricing sharply lower: US 10yr inflation breakevens -6.1bps to 1.69%; US 5Y5Y inflation swap is -7.2bps to 2.03%. The move lower in oil also weighed slightly on oil currencies with USD/CAD +0.5% and EUR/NOK +0.5%.

On US growth fears, the US ISM Manufacturing missed expectations, falling to 51.2 against the 52.0 consensus (51.7 previously; NAB 51.3) and lowest since August 2016. Weakness this month was driven by the Production Index which fell to 50.8 from 54.1 with firms continuing to erode their order backlogs (Backlog Orders Index fell to 43.1 from 47.4 previously), amid little growth in new orders (New Orders Index 50.8 from 50.0). The Employment Index also fell to 51.7 from 54.5 and could be suggestive of trade uncertainty affecting firms’ hiring decisions – though the evidence is mixed in Payrolls to date. Anecdotes in the report highlight very divergent conditions –a number noting “business is strong”, while an equal number note “weakness in end markets accelerating rapidly. Continuing to reduce production based on weakening demand and declining orders”. Construction spending for June also disappointed at -1.3%m/m against the +0.3% consensus and suggests there could be downward revisions to Q2 GDP (note Q2 GDP initially reported at 2.1%, could be shaved by a tenth or two on the back of the data). While on the positive side, Jobless Claims remain at low levels at 215k (214k was the consensus).

There were also a host of other PMIs released overnight with the aggregate JP Morgan Global Manufacturing PMI falling to 49.3 from 49.4 and now is at its lowest level since October 2012. Of 30 nations covered by JP Morgan, 19 had manufacturing PMIs signalling downturns.

In other news, the BoE kept rates unchanged at 0.75%, but downgraded their growth forecasts to 1.3% in 2019 from 1.5%, and the 2020 to 1.3% from 1.6%. The Bank sees a 33% chance that the economy could contract in annual terms in Q1 next year. There was little reaction to GBP with markets far more focused on the risks of a no-deal Brexit.

Also in central bank news, MNI reported the ECB is readying a tiered cut in its deposit rate in September that would open the way for credible forward guidance that the ECB could cut further. MNI quoting one ECB source “if you have some measure to isolate banks from the excessive costs of negative rates then you have more room for further interest rate reductions…guidance on the future direction of rates become more credible”. Markets a fully priced a 10bp deposit cut in September, with a possible further cut in early 2020.

Finally, Australian house prices continue their stabilisation with prices across capital cities up 0.1% in July. Sydney and Melbourne saw slightly stronger increases, both up 0.2% and over the past two months Sydney prices are up +0.3% and Melbourne prices are up +0.4%.

A busy Friday ahead where initial focus will be on Australia’s Retail Sales, and then to the US for Non-farm Payrolls. There is also a smattering of second-tier data including NZ Consumer Confidence, BoJ June Minutes, Eurozone Retail Sales, and the UK Construction PMI.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.