Online retail sales growth slowed in May following a fairly strong April

Insight

New positivity with the Dow breaking 30,000 for the first time, due in part to hopes for; a vaccine and a peaceful transition for the Biden administration.

What are you looking at, Strike a pose, Strike a pose

Vogue, vogue, vogue – Madonna

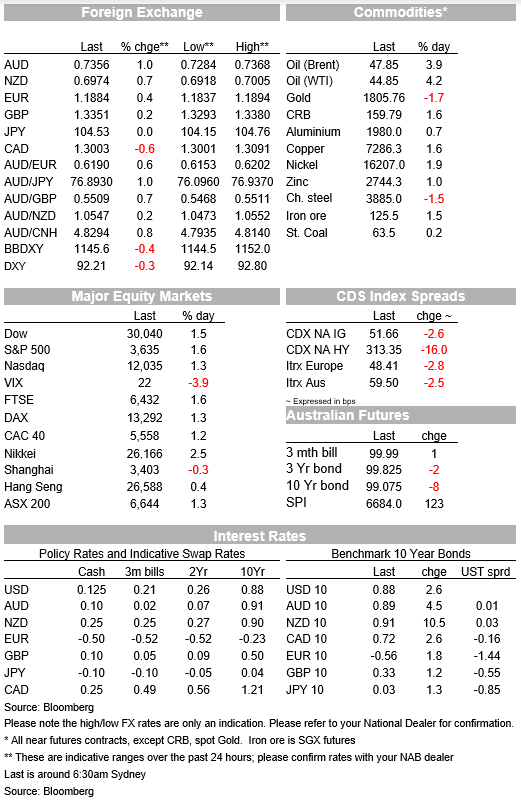

Risk assets had a solid session overnight as investors gain further confidence on the prospect of a broad and strong economic recovery, supported by the possible distribution of vaccines before year end and a peaceful US presidential transition. Cyclicals and small-caps are in vogue leading the gains in equity markets while oil has led the charge within the commodity space, gold the notable underperformer. The USD is broadly weaker with commodity linked currencies at the top of the leader board.

European equities opened sharply higher embracing yesterday’s news that President Trump had finally relented consenting to the start of the transition process to the Biden presidency. While Trump added that his legal fight against the election outcome “STRONGLY continues”, the commencement of the transition process removes an uncertainty that was previously overhanging the market.

News on this front overnight didn’t get better for the president with Nevada Supreme Court certifying Joe Biden’s 33,500-vote victory. Michigan made Biden’s win there official on Monday, Georgia certified its results last week and Pennsylvania followed earlier Tuesday. Arizona is set to certify its results on November 30 and Wisconsin by December 1, after a Trump-requested recount in two counties is completed. President Trump’s ability to overturn the election outcome look all but gone.

European equities closed near the day’s highs with all major regional indices up over 1% while the Stoxx 600 rose by 0.9%. Energy, banks and miners were the biggest winners while on a country level Spanish and Italian equities outperformed.

The sector rotation is also evident in the US equity market with the industrially heavy Dow index stealing some of the headlines after breaking above 30,000. The index is up 1.45% as I type and it currently trades at 30,019. Notably too, the Dow is leading the gains month to date, up 13.3% reflecting a shift in investor preference back towards cyclical stocks. Small-cap and value stocks are also outperforming (Russell 2000: +1.8%) and big tech firms underperforming, but still showing decent gains (NASDAQ: +1.26%).

In addition to President Trump’s consent to the transition process, the pricing of a global broad economic recovery has also been boosted by positive vaccine development . The head of the US government’s Operation Warp Speed program told CNN that vaccinations against Covid-19 in the US will “hopefully” start in less than three weeks. Bloomberg also notes that an advisory panel of the Food and Drug Administration is meeting on December 10 to discuss emergency use authorization for a vaccine candidate. Pfizer Inc. and BioNTech SE have requested that authorization for their product.

Oil has led the gains within the commodity space with Brent crude oil rising over 4% to $47/barrel, its highest level since March, and copper – often seen as a barometer of global growth – closing it on its highest level in six years. Gold on the other hand has been the notable underperformer, down 1.8%.

Moving onto currencies, the USD has lost some of its safe-haven appeal amid the solid and broad improvement in risk appetite. In index terms the USD has reversed almost all of yesterday’s gains, down around 0.3% for both the DXY and BBDX indices. Commodity linked currencies have led the charge within the G10 space with NOK at the top of the leader board, up 1.3% and reflecting its higher degree of sensitivity to movement in oil prices.

The AUD and NZD are not too far behind up 0.9% and 0.75% respectively. The AUD now trades at 0.7353, after making an overnight high of 0.7368 and the NZD is at 0.6973 after briefly touching 70c for the first time since mid-2018.

Yesterday the NZ rate and NZD were lifted by an unexpected NZ government announcement. Finance Minister Robertson wrote to RBNZ Governor Orr yesterday afternoon stating his concern with recent house price appreciation. Robertson suggested that the RBNZ’s Remit be changed, by formally adding house prices as a consideration.

Late in the day, the RBNZ acknowledged the letter, pledging to work together with the government on the issue, but rightly pointing out that there are longer-term, structural issues at play affecting house prices, not just interest rates. The RBNZ added that the monetary policy response, both in NZ and offshore, is intended to lower interest rates, thereby promoting spending and investment in order to meet its inflation and employment objectives. The RBNZ Financial Stability Report today and, RBNZ Governor Orr press conference now take on greater market significance ( see more below).

Longer dated UST yields have led a steepening of the UST curve, again reflecting the improvement in risk appetite and global growth outlook. The 30y bond is up 5bps to 1.60% and the 10y Note is up 3bps to 0.88%. Core yield in Europe climbed around 1bps with the 10y Bund closing the day at -0.56%.

Media outlets have reported that former Fed Chair Janet Yellen will be Biden’s choice as Treasury Secretary, with an official announcement due imminently. Yellen is seen by the market as being in favour of greater stimulus, although she will still need to contend with what is likely to be a Republican-controlled Senate.

In economic data, the German IFO business survey fell in November, mirroring the decline in the German Composite PMI released earlier in the week. US consumer confidence was also weaker than expected, which can be attributed to the resurgence in Covid-19 in the country and disappointment among Republican voters around the election outcome (the mirror image of the post-2016 surge in confidence). There was little market reaction to the data releases.

This morning the RBNZ publishes its bi-annual Financial Stability Report followed by RBNZ Governor Orr news conference. Undoubtedly, the Governor will have to address the NZ government’s proposal to add the stability of house prices to the RBNZ’s Remit. Also, this morning, Australia gets Construction Work Done for Q3. A soft Q3 Construction Work Done headline is expected by our economists at -2% vs 1.9% by consensus. Although Victoria’s lockdown is seen as the main culprit for the negative print, worth noting that NAB recently upgraded its GDP growth outlook on the back of a stronger than expected rebound in consumption where retail sales are 6.7% higher than pre-pandemic levels. NAB now sees Q3 GDP at around 4% q/q and we expect GDP growth to have recovered to its pre-COVID levels by the end of 2021. Looking at the rest of the economic calendar it is a busy day the for the US with data highlights including weekly jobless claims, preliminary wholesale inventories, durable goods orders and non-defence capital goods orders ex air, plus personal income/spending and new home sales (all for October). The second Q3 GDP reading is due for release along with the final November University of Michigan consumer sentiment.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.